The topic of narrow leadership and participation has been around this year in various flavors, most notably in the summer ahead of the minor 5% pullback in September and once again most recently. Dip buyers have continued to show their strength, snapping up any drawdown shown by the mega caps. As we wrapped up trading on Friday with the S&P 500 at a new 52-week high, the average stock was down 10.4% and nearly 17% of the index is off its high by at least 20%.

The market isn’t required to get equal contribution by all its components, but when participation is broad it acts as a bullish sign the market is healthy. This year, just a handful of stocks have all that mattered to get the bulk of the gain obtained by the large cap S&P 500 index. As the year as progressed an increasing number of stocks have been unable to keep up with the index, finishing on Friday with just 46.8% of stocks outperforming the index year-to-date.

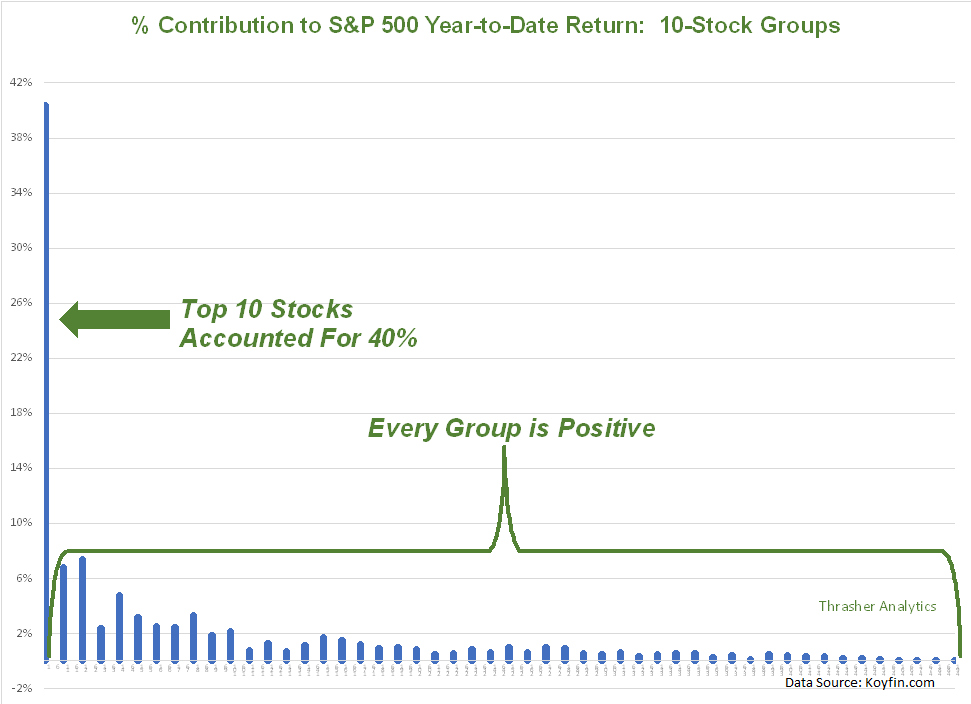

Individual Stock Contribution To S&P 500 Return Year-to-Date

There’s been a lot of discussion by financial writers and bank analysts about the extremely narrow contribution to returns within the Nasdaq 100. The pie chart showing just five of the 100 stocks carrying most of the water is getting passed around. I prefer to focus on the S&P 500, which was the topic of my own study on the percent of stocks contributing to the index performance. Below we have the YTD contribution by each S&P 500 stock, sorted by index weighting and then put in groups of ten.

As you can see on the chart below, the top 10 SPX stocks have accounted for 40% of the year-to-date gain. Truly amazing. But what’s also just as impressive, there’s not a 10-stock group that is negative right now.

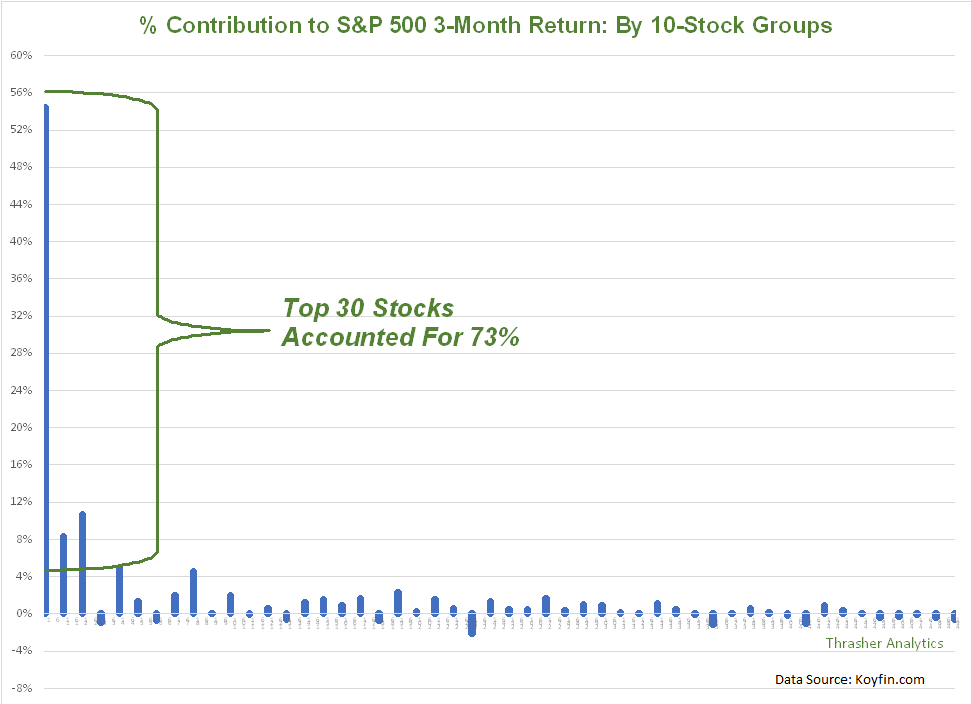

Individual Stock Contribution To S&P 500 Return Over The Last 3 Months

Let’s look at the percent contributed to the last 3-months of the S&P 500 gain. Again, it was just the mega caps, the top 30 stocks, that account for 73% of the gain. Over 50% is accounted for by just the top ten stocks! When does Standard & Poor’s just ditch 450 of the constituents?

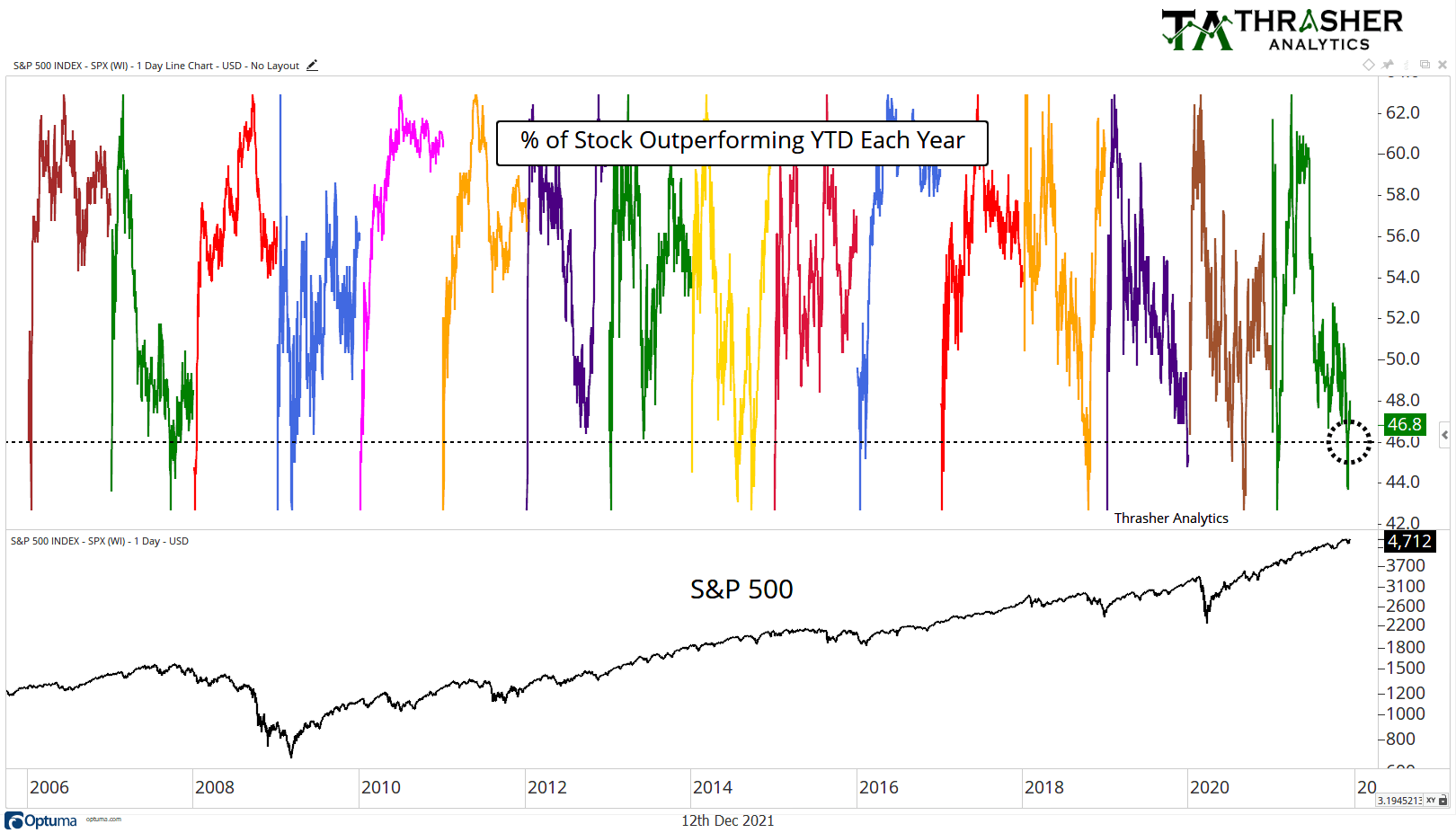

Annual Stock Outperformance: 2006-2021

Is it normal to see this low of a level in stocks showing strength? Below is a study showing each year’s percent of stocks that were outperforming the index, going back to 2006.

Typically, we see 55% to 60% of stocks outperform the index, with several years seeing a drift lower into year-end but rarely do we get below 50% or to current levels near 46%.

A few periods stand out…. At the ’07 peak we got to 46%, also at the ’09 low when many stocks were assumed left for dead, we went below 45%. We saw a low level of outperformance near the 2015 high as the index stagnated and few stocks were able to show strength. Finally, ore recently in Q4 ’18 and at the end of the year in 2019 we saw a move under 46% as breadth narrowed.

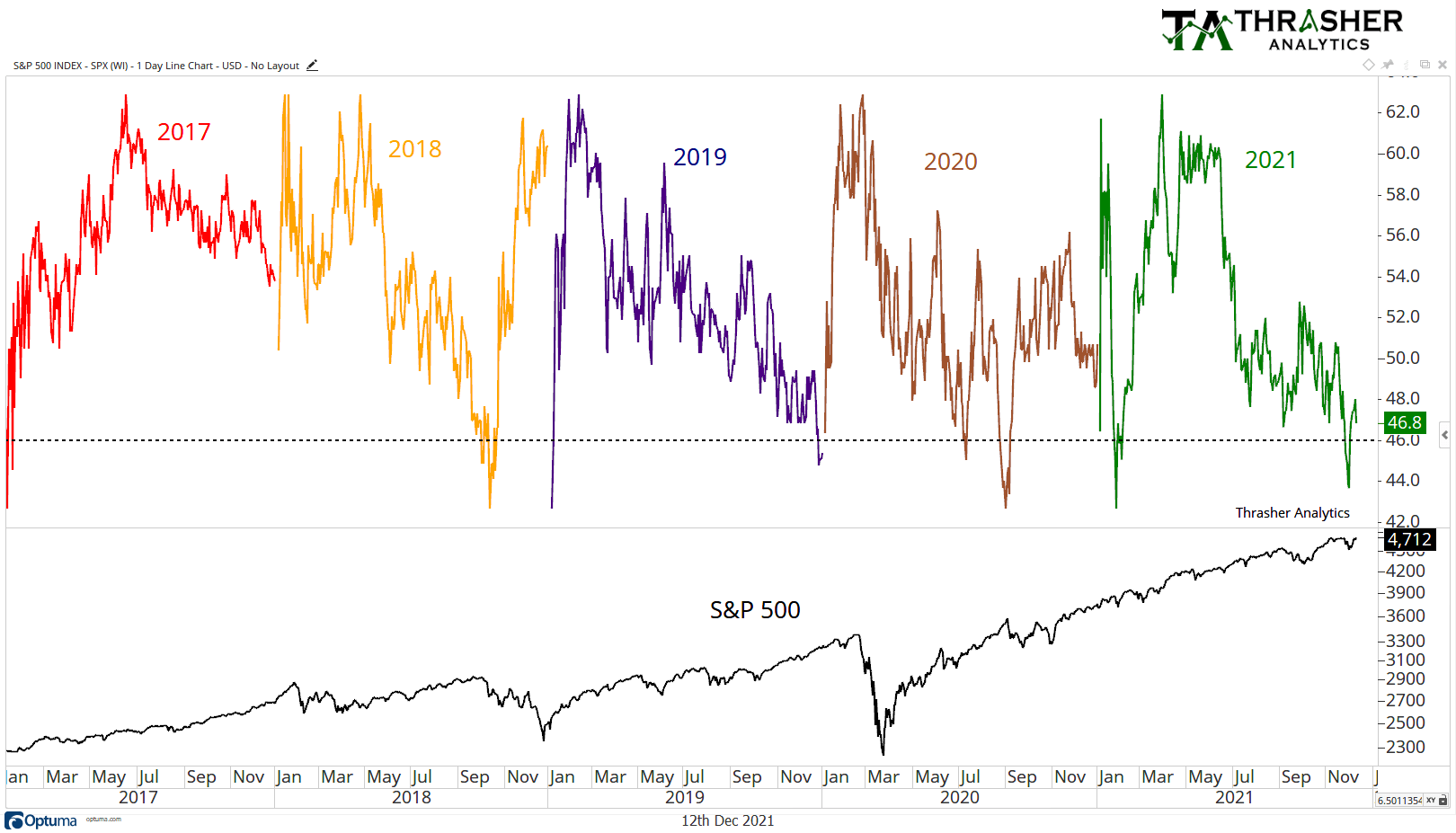

Annual Stock Outperformance: 2017-2021

Here’s a look at the same chart for 2017 to today. 2017 was a strong year for the index which received good support by individual stocks. 2018 saw a steady drift lower from 60% to 44% by the time the index broke lower, a similar move as we’ve experienced this year – a slow bleed lower. Then the Q4 drop in the index played “catch down” to how the individual stocks were performing, declining 20%. During that time, we saw a strong improvement in stock relative performance, finishing the year with north of 60% outperforming. Coming out of the Covid Crash, the index saw an extremely strong v-shaped recovery, outpacing most stocks until later in the year.

This year we had strong outperformance by individual stocks in the first part of the year and then things began breaking down in the summer, moving under 45% over the last couple of weeks.

While the same size is small, when we’ve seen this small number of stocks able to outperform the index, the SPX was more susceptible to a bearish move than when the majority of stocks showed strength.

So what’s it mean?

In the simplest terms, it means that the stock market is heavily reliant on just a handful of stocks to fuel the latest leg higher. This on its own isn’t problematic if those stocks don’t disappoint. However, it does make the market more vulnerable to bearish headwinds should those handful of stocks not deliver and the market begins to “chase down” the other large cap components that have struggled to keep up. 2021 has been a posterchild example of a market that can bend due to narrow breadth but not break as a result of it. Will this last in perpetuity? History would suggest not but it doesn’t set an expiration date either.