Trending

Written by: Jack Manley and Alex Nobile

As younger adults continue to enter the workforce, employers are being forced to innovate the employee experience. Previous research suggests that among young professionals, planning for retirement is one of the more daunting obstacles. There is a plethora of educational resources on simple plan facets, like contribution amounts or differences between traditional and Roth vehicles, but these materials are often very general and can lead to decision paralysis. For this reason, financial planning is one of ripest areas for potential innovation.

J.P. Morgan recently completed a survey of Defined Contribution plan participants. As these data are broken down by age group, we are able to isolate the findings for those Americans under the age of 30; the results are not always obvious, and may be instrumental in creating more effective employer-sponsored retirement plans for the future.

Younger Americans are likely to rely on their employer for financial planning outside of retirement.

Financial health is one of the greatest threats to young adults, and it is persistent. In fact, 80% of those surveyed believe their employer has at least some responsibility in helping them with overall financial wellness. Given the massive amount of student debt, this can include debt counseling and student loan repayment assistance, but also help in building emergency savings. Since these participants prioritize building emergency savings before retirement, a prudent savings strategy could be a “gateway” to increased retirement plan contributions.

Younger Americans are especially likely to rely on their employer for retirement savings.

89% of surveyed young participants say their employer has a responsibility to help their employees save for retirement. This naturally includes a match program for 401(k)s, but also includes a more advisory component: 7 in 10 believe their employer should provide financial advice and coaching for retirement. This includes information like how much should be saved, how it should be invested and how to get back on track if one isn’t doing enough for retirement.

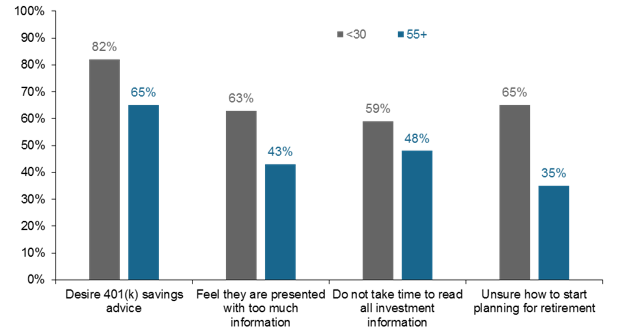

Younger Americans want more advice, and simple, holistic solutions are welcomed.

Surveyed young plan participants are more likely to desire 401(k) savings advice than near-retirees (82% vs. 65%), and they are willing to spend time planning their retirement. However, challenges exist: compared to near-retirees, they are more likely to say they are presented with too much information (63% vs. 43%); they do not take the time to read all investment information (59% vs 48%); and they are unsure how to plan (65% vs. 35%). Clearly, simplification and targeted communication is necessary, both in materials and also products. In fact, 70% of young participants would be willing to completely hand over retirement planning to a financial professional, and nine in 10 find access to a target date fund, which hands over retirement investing to a professional team, appealing.

Put simply, young Americans need more from their employers, and given the ongoing demographic transformation, the challenges that employers face now in talent acquisition and retention will likely persist if not intensify. For that reason, the most successful employers will be the ones to meet these needs most completely.

Participant sentiment by age groups

Source: J.P. Morgan Plan Participant Research 2021.

Related: Does a Continued Inflation Heatwave Mean a More Hawkish Fed?