Trending

Written by: Bryce Coward | Knowledge Leaders Capital

It’s no secret that money has poured into passive equity vehicles as investors seek low fees above all else. To date, that has worked out just fine since equity indexes have compounded their returns at acceptable, if not above average, rates of returns. But, the world is different now than it was 10 years ago, and the low-cost advantage of passive investing may now be outweighed by its risks.

In this quick post we’ll address three risks to passive investing that together suggest the riskiness of this strategy may well be the highest it has ever been.

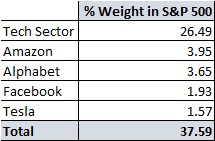

Taking the S&P 500 as an example, the weighting toward tech-like stocks introduces significant concentration risk. Indeed, the weighting of the technology sector + Alphabet, Amazon, Facebook, & Tesla is a whopping 38% of the total S&P 500. In other words, 38% of passive investors’ exposure is to one risk factor. That’s a lot of chips to put on one bet.

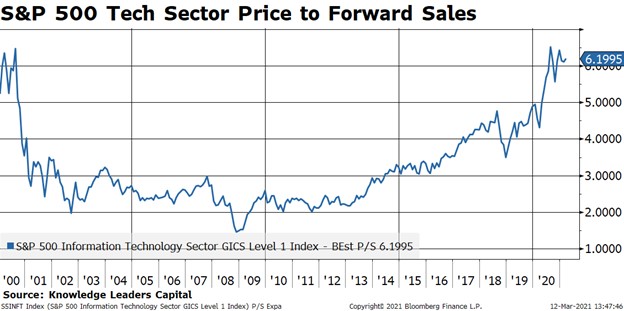

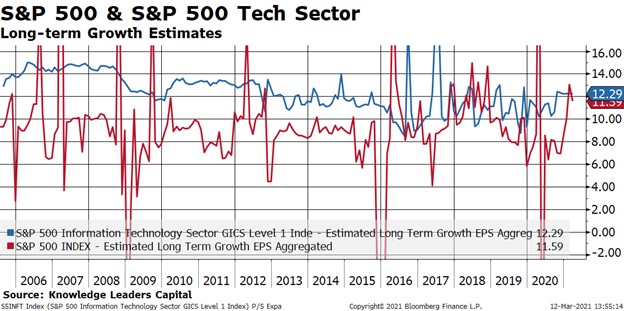

The valuation for the tech-like stocks is out of control. Taking just the tech sector as an example, it’s trading at 6.2x next year’s sales. This valuation extreme was only eclipsed (barely) in the late stages of the tech bubble. Since valuations inform prospective returns, passive investors in the S&P 500 are basically locking in a below average rate of return since 38% of their portfolio is invested in highly valued stocks. But…the growth. Yes, valuations always need to be calibrated against prospective growth rates. However, tech sector growth rates have been trending down since 2006. For the first time in a very long while, S&P 500 long-term growth is expected to be on par with tech sector growth.

Tech valuations are highly related the level of long-term interest rates. Much of the “value” in tech stocks is the stream of cash flows that is expected many years from now, which is similar to the payoff profile of a long-term bond. When interest rates rise, the present value of those future cash flows (for bonds and high growth stocks) goes down. Since we’re in an environment in which very long-term interest rates are more likely to rise than fall, this will generally put pressure on tech valuations.

This is kind of hat trick for passive investors. Passive portfolios are highly concentrated in stocks with overlapping risk exposures, the valuation of those stocks is in the 99th percentile, and there is a catalyst for those valuations to compress. Combined, these things add up to a below average rate of return for passive portfolios, even if the average stock does just fine. But the fees are low…

As of 12/31/2021, Alphabet, Amazon and Facebook were held in a Knowledge Leaders Strategy. Tesla was not.

Related: The Case for Investing in Homebuilders

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.