Trending

Written by: Bryce Coward | Knowledge Leaders Capital

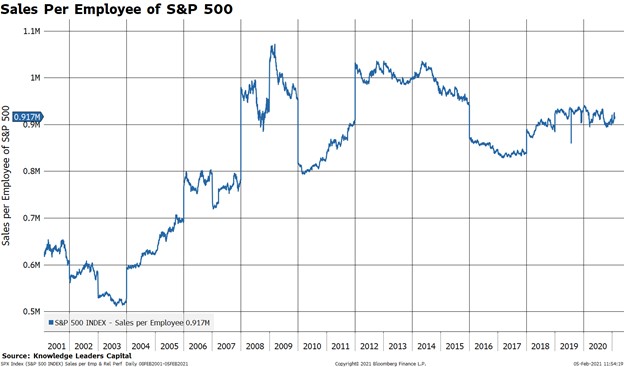

There are a few ways to measure productivity. One simple way to measure productivity at the company level is to calculate sales per employee. Higher sales for the same number of employees obviously means each employee is pulling more weight. Profits are a byproduct.

The interesting thing about US stocks recently is that productivity has declined for about a decade.

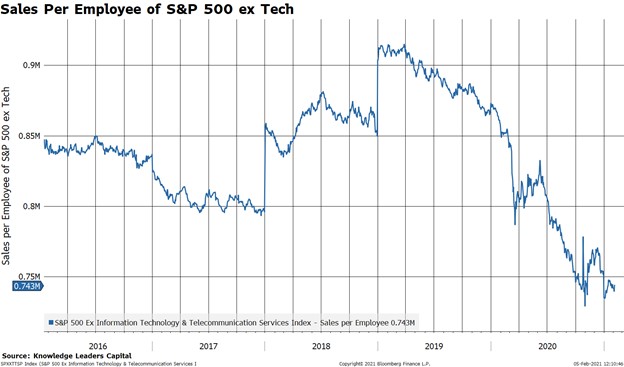

Excluding tech, productivity for S&P 500 companies is even worse.

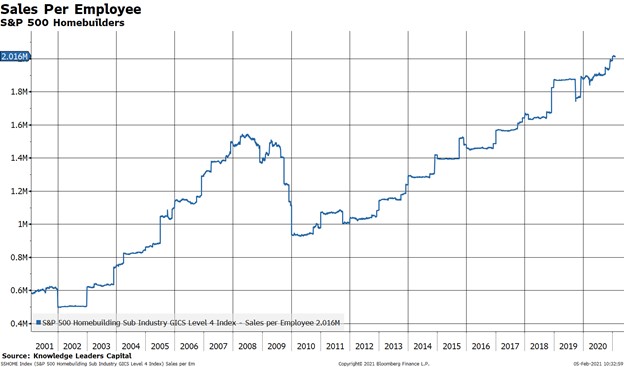

So, when we find that an industry has rising productivity it piques our interest. This is true of homebuilders. Our interest gets further piqued if 1) the market doesn’t seem to be “getting it” and 2) there are unrelated fundamental tailwinds.

Let’s check out that first point. Is the market “getting” that homebuilders are becoming more productive every year? No, it is not.

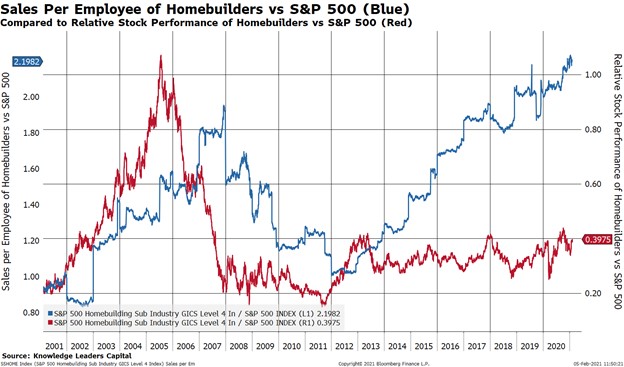

In the next chart I plot the sales per employee of homebuilders vs that of the S&P 500 as a whole (blue line). I then overlay the relative stock price performance of homebuilders vs the S&P 500 (red line). Following the housing crisis/crash in the 2000s, the homebuilders have been in the penalty box, so to speak. They are doing more with less, especially relative to most S&P 500 companies, and yet the stock prices of homebuilders have shown basically no outperformance. This implies catch up potential for the group.

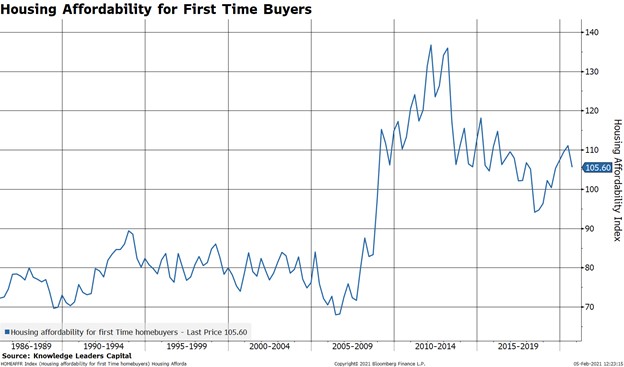

Now, on to point number 2 regarding unrelated fundamentals. Mortgage rates are at historic lows, which is an obvious tailwind for homebuilders. To the extent lower mortgage rates make buying a new home more affordable, more homes will be sold. This is without considering prices, obviously. On prices, house price affordability for first time buyers is off the best levels, but WELL better than where it has trended historically.

Moreover, the homeownership rate for people under 35 is still below average even though it has ticked up in recent years.

Affordable housing + a homeownership rate that has room to rise = higher sales and profits for homebuilders. This is to say nothing of closing those productivity “jaws” that have opened up since the housing crisis.