Trending

If you’ve paid any attention to financial news recently, then you know October had the worst monthly stock market decline since 2011. You didn’t have to look far, as stock market noise was at a crescendo. Media headlines were filled with phrases like: epic turmoil, getting crushed and no place to hide. Emotionally charged words that make you feel like you need to do something to prevent losing more of your nest egg. But following our instincts when investing, can lead to dangerous outcomes. In times like this, we need a strategy to give us proper perspective . On this episode, we’ll discuss why market fluctuations are incredibly normal and provide techniques to help you cope with short-term volatility and keep your focus on long-term goals instead. If you’re getting nervous about the direction the market is taking, you’ll want to listen for steps to confront the inevitable next occurrence.

How to Deal with the Emotional Roller Coaster of Investing

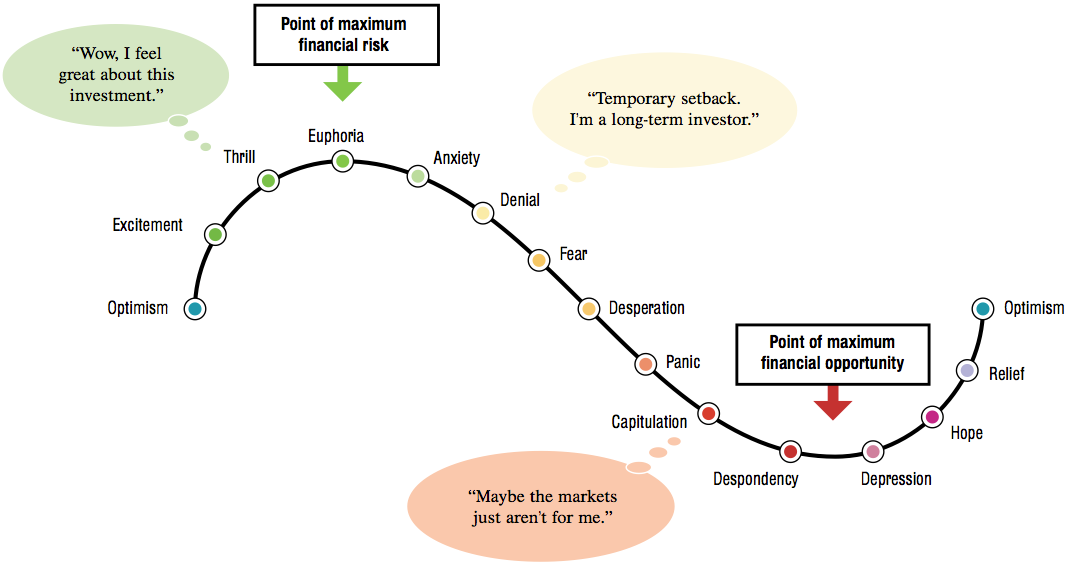

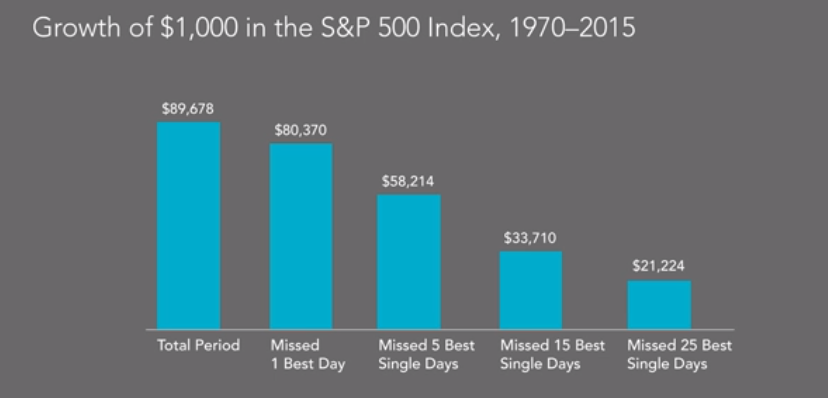

When listening to financial news, it’s important to remember that the media’s ultimate job is to sell advertisements. It’s not their job to help you see the long-term picture or help you reach your financial goals. Easier said than done when markets around the world experienced a 10-15% drop in October. But if we back up, history provides a different perspective. Market volatility is reliably normal, but it can still make you feel nervous. To truly understand the ups and downs, take a look at the chart below from the Capital Group. There have been 12 full-blown bear markets since 1945. A 5% or more decline in the market typically occurs 3 times a year. And a 20% drop usually occurs about every 4 years. The past 10 years have actually been the anomaly. It is important to remember that a bear market isn’t a bad thing. It’s actually a great time to reassess your investment plan and evaluate your risk tolerance. Truly understanding your time horizon, will not only help you digest market drops easier but simultaneously help you take advantage when others are rattled. Because time in the market is miles more important than timing the market. One of the hardest temptations to fight when investing is speculation around when the next market decline will be. So much so, we convince ourselves that we should get out when things are good and get back in after the worst is over. What we miss with that strategy, is many of the best performance days happen near the worst days when volatility is at it’s highest. This is where missing a few of those best days can mean tens of thousand dollar differences demonstrated in this Dimensional Fund Advisors chart.

It is important to remember that a bear market isn’t a bad thing. It’s actually a great time to reassess your investment plan and evaluate your risk tolerance. Truly understanding your time horizon, will not only help you digest market drops easier but simultaneously help you take advantage when others are rattled. Because time in the market is miles more important than timing the market. One of the hardest temptations to fight when investing is speculation around when the next market decline will be. So much so, we convince ourselves that we should get out when things are good and get back in after the worst is over. What we miss with that strategy, is many of the best performance days happen near the worst days when volatility is at it’s highest. This is where missing a few of those best days can mean tens of thousand dollar differences demonstrated in this Dimensional Fund Advisors chart. Related: How to Avoid the Financial Mid-Life Crisis

Related: How to Avoid the Financial Mid-Life CrisisFight Fear with Facts

With breaking news coming at us as quick as we want it with social media, it’s even harder to block out the noise. Whether tweets or 24 hour cable news, today’s financial news is near immediate compared to 30 years ago when you may not hear it until the next day. In Jason Zweig’s book, Your Money and Your Brain, he provides some powerful questions to prevent your feelings from overwhelming the facts. Instead of listening and reacting to the financial news du jour, stop to pause and think about if anything else has changed in your financial picture, other than price of your investment. Consider if your reasons for investing in that investment is still valid? Ask, if I liked this investment enough to buy it at a much higher price, shouldn’t I like it even more now that the price is lower? Investigate, what other evidence do I need to evaluate in order to tell whether this is really bad news? Has this investment ever gone down this much before? If so, would I have done better if I had sold out-or if I had bought more?What Should You Do Next?

To successfully navigate a bear market, you need a long-term strategy in place. Cliche? Sure, but considering where you are in life now is instructive in developing your treatment plan for market short-term sickness. If you’re in your 20’s and 30’s don’t worry, there is still plenty of time. Investment choices still matter at these ages, but not nearly as much as your actual savings amounts. Dollar cost averaging your 401k contributions alone will help you steadily take advantage of the drop in stock prices, a fantastic long-term sale. If in your 50’s and 60’s, it’s much more important to focus on your overall investment strategy. How does your asset allocation match your retirement timeline? For many in this walk of life, investment returns will be larger than your annual savings amounts. You’ll also be facing the sequence of return risk which can eat a big portion of your retirement without a strategy. Professional help at this point, can help you respond accordingly to market events and more importantly, act as an accountability partner. Having a buffer between your emotions and the markets may be the most important financial decision you can make.