Trending

Expressing love through financial support is a powerful gesture, but understanding the tax implications is crucial. Gifting money to family members goes beyond material presents, offering financial assistance and security. In this article, we'll delve into the nuances of charitable planning and the tax considerations that accompany it.

Navigating the Tax Landscape: Key Considerations

1. The Annual Gift Tax Exclusion:

-

Maximizing Your Generosity: In 2023, the gift tax limit is $17,000, increasing to $18,000 in 2024.

-

Spousal Unity: For married couples, this doubles the limit to $34,000 in 2023 and $36,000 in 2024.

2. Reporting to the IRS:

-

Stay Within Limits: If you give away more than the annual exclusion amount in cash or assets (for example, stocks, real estate, a new car) to any one person during the tax year requires filing a gift tax return alongside your federal tax return.

-

Reporting your gift to the IRS does not necessarily mean you will owe additional taxes on the gift. It only means you will need to file IRS Form 709 to disclose the gift. In fact, most taxpayers will not ever pay a gift tax due to the IRS lifetime gift tax exemption of $12.92 million (for 2023).

For example, if you gifted a vacation property with a $217,000 fair market value, to one of your children, you would need to report $200,000 to the IRS ($217,000 – $17,000 annual deduction = $200,000). Your lifetime maximum gift tax exemption would be reduced by $200,000.

3. Lifetime Gift Limit:

-

The lifetime gift tax exemption is scheduled to be reduced in 2026. Current estimates are for the exempted amount to be about $6.8 million in 2026. IRS regulations will allow use of either the lifetime gift tax exclusion that applied when gifts are made or the exclusion amount applicable when the donor dies, whichever is greater.

-

Exemption Insights: Despite reporting, the IRS lifetime gift tax exemption of $12.92 million (2023) means most won't incur additional taxes.

-

Future Adjustments: Be aware that the lifetime gift tax exemption is anticipated to decrease to about $6.8 million in 2026.

Who Bears the Tax Burden?

1. Tax Responsibilities:

-

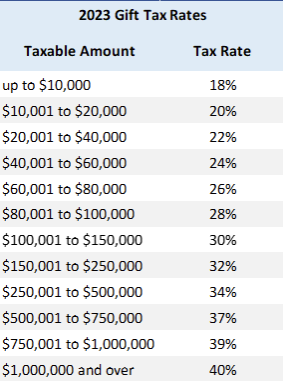

Gift Tax Rates: If limits are surpassed, the giver typically pays taxes, with rates ranging from 18% to 40%, depending on the amount of the gift.

-

Recipient Considerations: Recipients may face capital gains taxes upon selling gifted property in the future.

2023 Gift Tax Rates by gift amount.

The Heart of Generosity: Sharing is Caring

-

Practical and Meaningful: The act of gifting money or other assets is not only a practical means of helping loved ones meet their needs, but also as a demonstration of care, empathy, and commitment to shared well-being. Knowing the potential tax implications of your generosity is important as you consider this important and meaningful gesture.

-

Gifting money or other assets can be an important part of estate planning. If you have questions on this topic or other estate planning topics please reach out to us at Clientfirstcap.com or sign up for our monthly newsletter for additional insights.

Proactive Insights and Future Considerations

1. Gift Tax Facts:

-

If you give more than the annual gift tax limit, you may have to file a gift tax return, but this does not necessarily mean that you'll owe taxes on the gift.

-

The gift tax exclusion limit is $17,000 in 2023 and $18,000 in 2024.

-

The gift giver is the one who generally pays the tax, not the receiver.

-

The 2023 lifetime gift limit is $12.92 million.

-

Gifts to qualified nonprofits are charitable donations, not gifts.

-

The person receiving the gift usually doesn't need to report the gift.

-

Annual Exclusion Clarity: The annual exclusion is per recipient; it isn’t the sum total of all your gifts. That means, for example, that you can give $17,000 to your cousin, another $17,000 to a friend, another $17,000 to a neighbor, and so on in 2023 without having to file a gift tax return in 2024.

-

Spousal Considerations: Unlimited gifts between spouses, with special rules for non-U.S. citizen spouses.

-

Strategic Gift Splitting: Couples can combine annual exclusions through "gift splitting" for a more substantial gift. One way to do this is by each contributing the annual exclusion amount to a 529 to fund your grandchildren’s education. For more on this, see this article.

-

Nonprofit Donations: Gifts to qualified nonprofits are charitable donations, distinct from taxable gifts.

2. Timing Matters:

-

Calendar Watch: Stay informed; Current estimates are for the exempted amount to be about $6.8 million in 2026, although the lifetime exclusion may revert to the previous $5 million in 2026, impacting your estate planning strategy.

Estate Planning and Your Lifetime Exclusion

1. Maximizing Your Legacy:

-

Lifetime Exclusion Management: The gift tax return tracks your lifetime exclusion, influencing your estate's tax implications.

-

Estate Tax Insight: If you don't give any gifts during your life, then you have your whole lifetime exclusion to use against your estate when you die. Learn more about how estate tax works.

Gifting with Purpose

Understanding the intricacies of charitable planning ensures that your generous gestures align with your financial strategy.