Trending

Written by: Ashley Perlmutter

As we are halfway through financial literacy month, we want to continue to discuss simple ways to better your financial life. At Sherman Wealth, we focus on helping young couples and families get their finances on the right track, which is why we want to talk about common financial mistakes young couples and families often make in their 20’s and 30’s that come back to haunt them in the future.

One of the first commonly made mistakes we see with our clients is purchasing the wrong insurance products. We see tons of people in their 20’s purchasing whole life and non-level term policies from large insurance companies that are truly not right for them and that they truly do not understand. Oftentimes, it is not until these individuals are starting their families and progressing their careers that they realize they have been losing money with the wrong policy for them. It is very important to discuss with a professional or research what policies are best for you and your family before blindly purchasing the wrong insurance.

Another commonly made mistake we see among this demographic is not signing up for your company 401(k) and taking advantage of the match. We have seen tons of cases where individuals are not signing up for their company’s retirement plan and matches until five to ten years later, which is giving away a large chunk of your salary benefits and essentially, “free money”. It is always the right move to sign up for your company 401(k) and contribute the full match if your situation allows you too in order to build a strong retirement account.

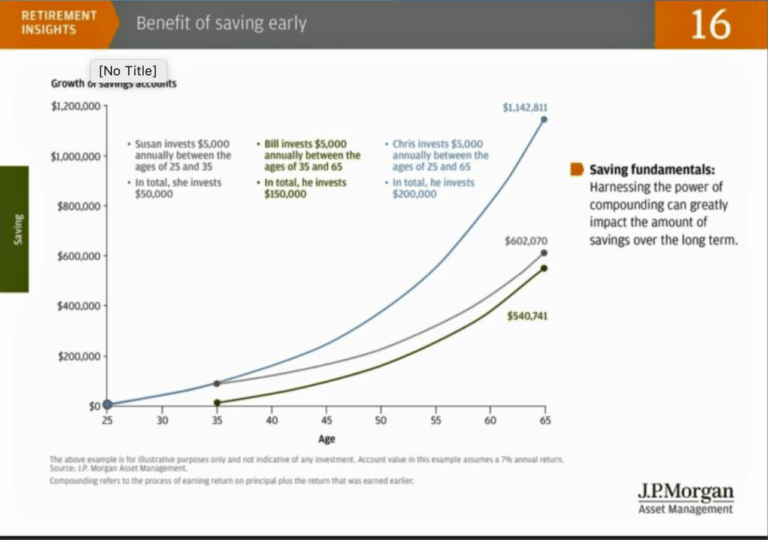

Budgeting and saving is always a priority when it comes to building your financial portfolio and especially starting a family. In previous blogs, we have talked about the importance of starting and saving from an early age and the power that compounding interest and “time” in the market has on your money. Whether you are starting your first job or graduating college, it is never too early to start saving, even if it’s only a few dollars per month.

As we are halfway through financial literacy month, we want to continue to discuss simple ways to better your financial life. At Sherman Wealth, we focus on helping young couples and families get their finances on the right track, which is why we want to talk about common financial mistakes young couples and families often make in their 20’s and 30’s that come back to haunt them in the future.

One of the first commonly made mistakes we see with our clients is purchasing the wrong insurance products. We see tons of people in their 20’s purchasing whole life and non-level term policies from large insurance companies that are truly not right for them and that they truly do not understand. Oftentimes, it is not until these individuals are starting their families and progressing their careers that they realize they have been losing money with the wrong policy for them. It is very important to discuss with a professional or research what policies are best for you and your family before blindly purchasing the wrong insurance.

Another commonly made mistake we see among this demographic is not signing up for your company 401(k) and taking advantage of the match. We have seen tons of cases where individuals are not signing up for their company’s retirement plan and matches until five to ten years later, which is giving away a large chunk of your salary benefits and essentially, “free money”. It is always the right move to sign up for your company 401(k) and contribute the full match if your situation allows you too in order to build a strong retirement account.

Budgeting and saving is always a priority when it comes to building your financial portfolio and especially starting a family. In previous blogs, we have talked about the importance of starting and saving from an early age and the power that compounding interest and “time” in the market has on your money. Whether you are starting your first job or graduating college, it is never too early to start saving, even if it’s only a few dollars per month.

Lastly, another mistake we see individuals making is not contributing to their health savings accounts (HSAs). A health savings account (HSA) can help you lower your taxes as they are triple tax free. Our advice is to always take advantage of these types of accounts if you are eligible, that can help you make the most of your current situation and future.

By avoiding these four commonly made financial mistakes in your early years, you and your family will be in a much better situation as you embark on the next chapter in your life. As always, speak with your financial professional to ensure you are making the right decision for your particular situation.