Trending

Written by: Phyllis Scruggs | Waddell and Associates

The older we get, hopefully, the wiser we become. And, unless we discover the fountain of youth, the less time we have left to make up for large investment losses. Readers of my quarterly client letters have heard these “words of wisdom” from me before. But as my mom used to tell me, there is no time like the present.

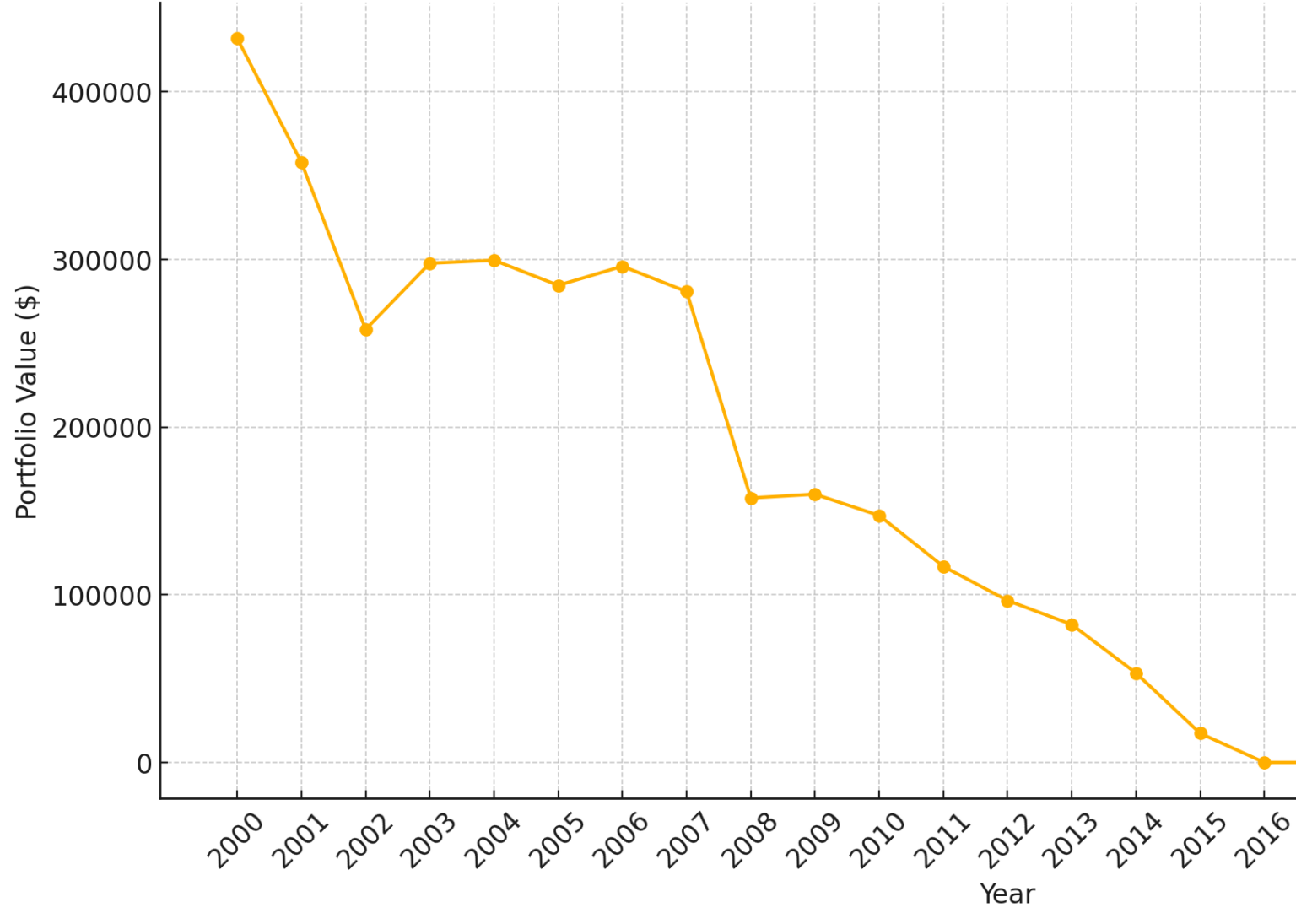

Here is a chart generated by ChatGPT to illustrate the annual values of a theoretical $500,000 portfolio invested in the S&P 500 starting on December 31, 1999, and assuming annual inflation-adjusted 5% withdrawals of $25,000. Bottom line: A 60-year-old would have run out of money at age 77.

As you can see from the above chart, it becomes increasingly important that we, as wealth strategists and clients, be proactive in taking steps to preserve our wealth, especially as we age and begin taking withdrawals. For most of you reading this, we’ve had this discussion recently and proactively made the appropriate adjustments. However, if worries persist, please let your wealth strategist know.

As we get older, allocating more to the shock absorbers of fixed income and cash, and less exposure to the short-term volatility of the stock market, becomes more important than taking a chance on how long it will take to recover the next time the stock market experiences turbulence. Put on your seatbelt and oxygen mask before turbulence occurs.

Related: Three Trends To Watch From Future Proof Citywide 2025