Trending

Like the U.S., the global macroeconomic outlook looks bleak. Persistent price pressures are weighing on consumers, global supply chains remain under pressure and recent manufacturing data suggests economic activity is softening globally. Moreover, in response to above-trend inflation further exacerbated by the war in Ukraine, policymakers are tightening monetary policy aggressively, many at the expense of growth in their respective regions. Given this, investors are concerned about recession risks globally.

Global growth has slowed from 6.0% year over year (y/y) in 2021 to a projected -1.0% quarter over quarter (q/q) seasonally-adjusted pace in 2Q221. Moreover, in July, the International Monetary Fund (IMF) cut its global growth forecasts from its April projections for 2022 and 2023 by 0.4% and 0.7% to 3.2% and 2.9%, respectively. Meanwhile, global inflation continues to surprise to the upside with developing market (DM) inflation running at 8.0% y/y and emerging market (EM) inflation at 6.7% y/y in June.

Recent manufacturing purchasing managers indices (PMIs), a good proxy for economic activity, signaled further slowing heading into the third quarter. Regionally, Europe is losing momentum with the July Eurozone manufacturing PMI falling below 50 to 49.8. PMI data in China suggest a smaller than expected lift from reopening thus far. Moreover, the divergence between manufacturing strength and weakness in services given service-oriented businesses were hardest hit through the pandemic, has narrowed completely, with both global services and manufacturing PMI’s logging 51.1 last month. DM economies continue to face significant downside risks in the form of aggressive central bank tightening and, in the case of Europe, threats to energy supply. EM economies face the dual headwind of both high inflation and a strong dollar which suggests a need for higher policy rates to keep their currencies stable.

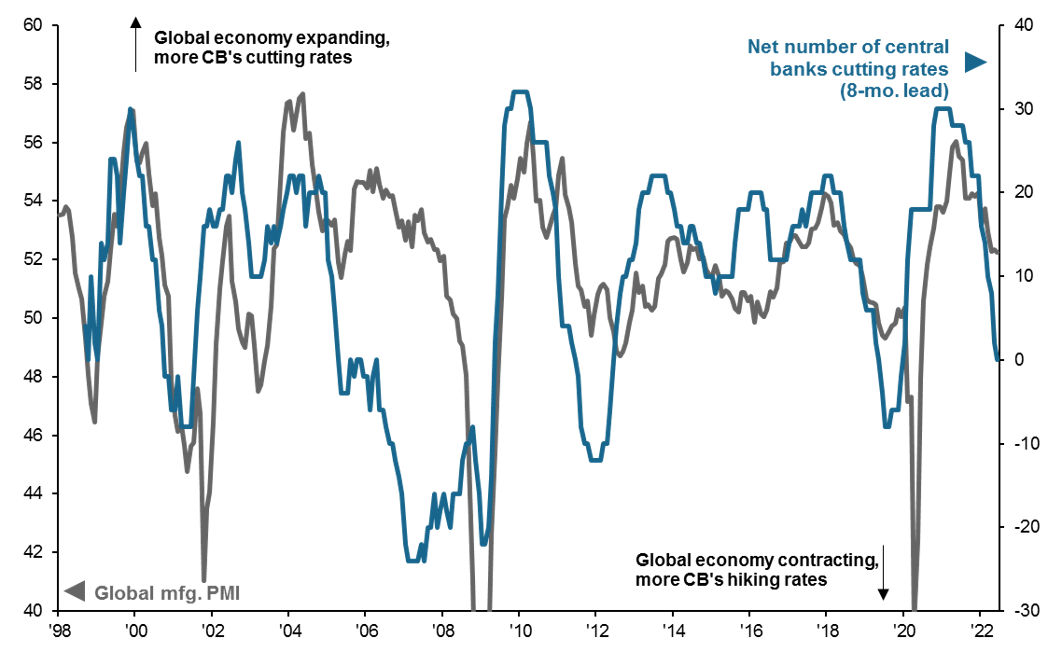

The broad takeaway is that economic conditions are softening globally, and aggressive central bank tightening is contributing to it. The global economy could avoid a recession if a stronger recovery emanates from China in the second half of 2022, and a soft landing is achieved in regions like the U.S. and Europe, however, that outcome looks increasingly challenging. As highlighted, our analysis across 32 central banks shows the relationship between global manufacturing activity and net easing/tightening by policymakers. Given central banks are expected to continue to hike rates through the end of the year, this presents a headwind to economic growth later this year and next, with manufacturing activity likely dipping below 50 (signaling contraction) for a period.

That said, there are still opportunities in international markets: elevated uncertainty and central bank action over the medium term suggests an active approach to sectors and economies that can more readily weather a global growth slowdown. For long-term investors, attractive valuations, higher dividend yields, and a falling dollar over the next several years suggest international equities remain attractive relative to the U.S.

Aggressive tightening from global central banks will likely contribute to slowing economic activity later this year and into next

JPMorgan Global manufacturing. PMI (left), net number of 32 developed and emerging market central banks cutting rates (right)

Related: How Should I Think About Investing in Alternatives?

Source: Bloomberg, Markit, J.P. Morgan Global Economic Research, J.P. Morgan Asset Management. Global mfg. PMI above 50 = expansion, below 50 = contraction. Analysis incorporates 32 central banks for the following countries: United States, Canada, Brazil, Chile, Colombia, Mexico, Peru, UK, Norway, Sweden, Switzerland, Czech Republic, Hungary, Israel, Poland, Romania, Russia, Turkey, South Africa, Australia, New Zealand, Japan, China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Taiwan, Thailand, and Euro Area. Data are as of July 31, 2022.

1Forecast is based on J.P. Morgan Global Economic Research.