Trending

Written by: Bryce Coward | Knowledge Leaders Capital

This week investors learned of President-elect Joe Biden’s initial bid for the next round of COVID-19 relief. The number came in at $1.9tn. Importantly, included in this figure is mainly covid relief as opposed to a longer-term fiscal package that will be heavily weighted to infrastructure. In other words, it’s covid relief first (plus some goodies to satisfy the democrat base), followed by infrastructure and other structural spending later in 2021. Even if the Congress won’t pass a $1.9tn covid relief bill, the final number is highly likely to be above $1tn. The longer-term package that includes infrastructure is likely to result in net spending of between $1-2tn, much of which is likely to be front loaded. Keep in mind also the $900bn in covid relief that was enacted in December. All in all, the US is likely to see fiscal stimulus up to ~10% of GDP in 2021 and another 5% of GDP 2022. This is on top of stimulus around 20% of GDP in 2020. This string of stimulus spending is simply unprecedented in peace time.

Now, we’ve been talking a lot about the possibility of the fiscal stimulus producing above-trend inflation for a period of time. Many pundits look back at the financial crisis period and point to the fact that, at the time, many investors also thought fiscal stimulus plus the Fed’s asset purchase program would lead to inflation. Asset purchases aside, fiscal stimulus during the financial crisis and years that followed amounted to less than half the stimulus as a percent of GDP than what will occur this time. Nevermind that fact that other catalysts for inflation exist today that have been absent in years past, including:

- Regionalization of supply chains

- Green energy policy that will put pressure on commodity prices from copper to lithium to nickel and cobalt. Indeed, EVs contain 183lbs of copper compared to 43lbs for combustion vehicles; wind turbines contain 800lbs of copper.

- Green energy policy that will seek to raise fossil fuel prices in general (either through taxes, a reduction in subsidies, or other hindrances to new production)

- Weakening USD from persistent budget and trade deficits (i.e. rising import prices)

- Room for the household savings rate (which is currently at 13%) to fall back to the 2-decade average of 6% (i.e. pent up demand)

Given the above, inflation is now a risk investors must consider and hedge for, which is different from anytime over the last 20 years. So, what are the best hedges for inflation?

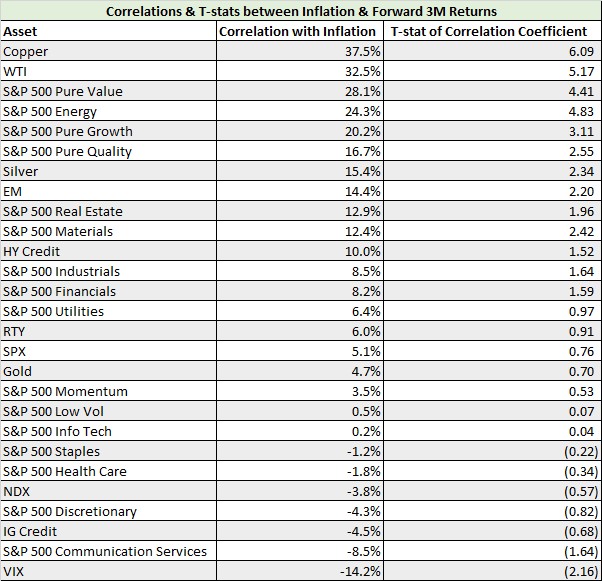

To answer that question we studied the correlations between returns of various asset classes/sectors and inflation, going back to 1971 where the data was available. Specifically, we calculated the correlation between 3-month forward returns and the following binary outcome: 1) inflation was above trend or rising or 2) inflation was below trend or falling. We found copper, crude oil prices, value stocks and energy stocks to be the most sensitive to the binary inflation measure. Furthermore, each of those assets/factors sported t-stats that are highly statistically significant. Interestingly, gold showed no correlation to our binary inflation measure. Silver did show a statistically significant positive correlation, albeit a small one.

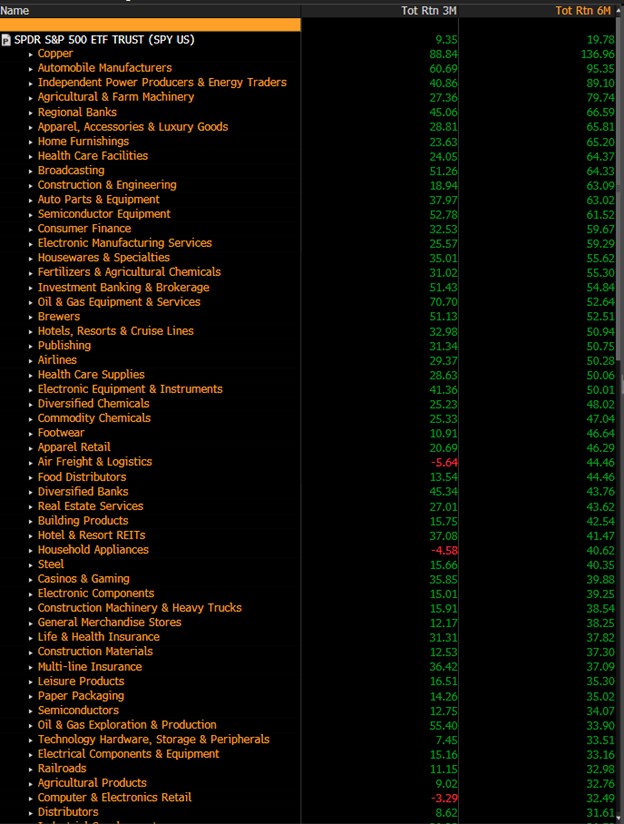

The above study helps us understand why copper has clearly broken out like a rocket ship from a 5-year long period of doing nothing at all. The move in copper explains why copper mining companies are the best performers in the S&P 500 over the last 3 and 6 months.

All in all, the hedging strategy here is fairly straightforward. If one believes above trend inflation is likely, or even rising in probability, one can hedge away some of that risk by owning a combination of copper and oil, or by expressing that view in the equity market by owning some combination of copper miners, energy stocks and value stocks. Now, is this the most opportune time to load up on said hedges? Our view is there may be a better entry point. But, if the above inflation narrative takes hold in the market, we are just in the nascent phases of this bull run in the inflation hedges.

Sign up for reports from Knowledge Leaders Capital.

Related: What Investors Can Expect in the New Political Environment