Trending

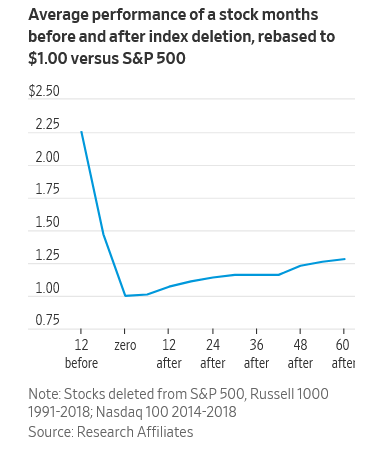

The Wall Street Journal shared an interesting investment strategy that Research Affiliates (RA) championed in its article, Wall Street’s Trash Contains Buried Treasure. Going by the index name NIXT, the strategy is designed to focus on a market inefficiency resulting from the overwhelming popularity of passive investment strategies. The NIXT index is simple: it buys stocks that have been kicked out of the indexes. RA claims investors would have earned 74x on their money since 1991 following the strategy. Per the article:

The basic idea isn’t revolutionary: Plenty of hedge funds make money, or try to, by buying stocks that are about to enter a widely held index such as the S&P 500 and selling short those about to leave. They know that there will be forced buyers and sellers who don’t care about the price. Instead of a speculative one-night stand with those stocks, though, NIXT includes them after they have been dumped. And, while not being wedded to those losers forever, it dates them for five years—an eternity for fast-money types. The surprising thing is how long the good performance lasts.

When stocks are added to an index, passive investors of the said index, by default, have to buy those stocks. Conversely, when a stock is removed, they must sell the stock. Not surprisingly, stocks taken out of indexes tend to be smaller and cheaper than most other stocks in the index. The article notes that between 1991 and 2022, stocks removed from indexes traded at a 26% P/E discount to the S&P 500 P/E. There is a catch with the NIXT model. The strategy can only afford a limited number of investments before the benefit of buying seemingly cheap stocks fades. The graph below, courtesy of RA and the WSJ, shows the average performance of NIXT index holdings in the year before being removed from its index and the five years following.

What To Watch

Earnings

Economy

Market Trading Update

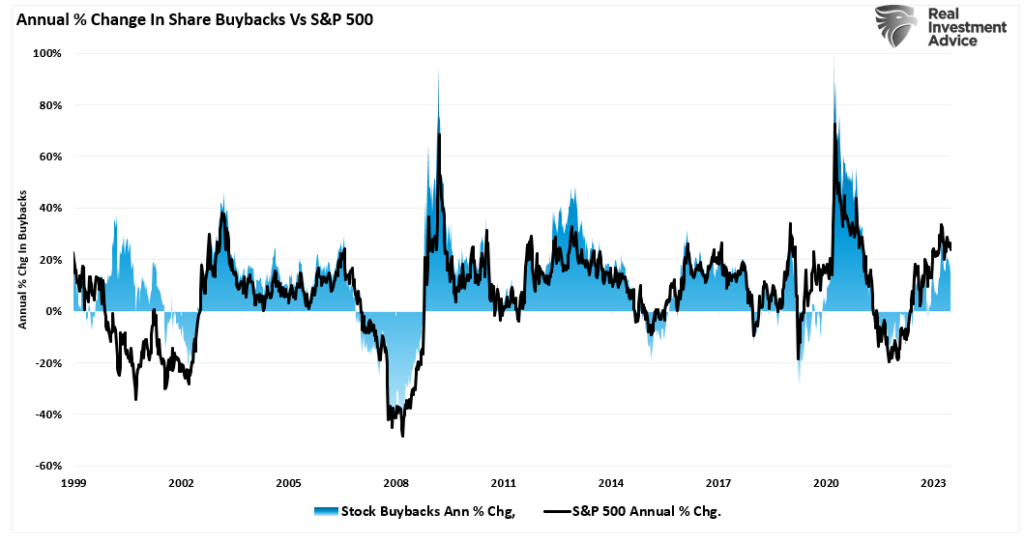

As noted yesterday, the market rally continues, and we are approaching a short-term MACD “buy signal.” While we are likely not done with the current correction process, one aspect that will provide support to the market in the near term is share buybacks.

With the Q2 earnings season behind us, the “blackout” window for buybacks is now mostly reopened.

Those buybacks are important because they continue to provide a bulk of the net purchases of equities in the open market. It was also a very active week for new repurchase authorizations, with 38 new programs authorized for $15.1 Billion.

Importantly, as I noted in yesterday’s blog post, there is a high correlation between the annual change in buybacks and the market.

The coming surge of buybacks will be an essential support for stocks in the near term. Such is particularly the case given the low liquidity of the overall market. As noted by Goldman Sachs:

“S&P 500 top book liquidity is currently at $5M. This is down from $26M in July. This is a decline in the worlds equity liquidity instrument of-80% in the last 3 weeks. Top book liquidity hit $3M on Monday, the lowest level since March 2023 (15 months). ETFs represented 43% of the overall market volume on Monday compared to 29% YTD.”

While there are certainly some concerns over the recent market decline, buybacks will substantially support the market in the near term heading into the October blackout period. Such sets October as a likely “flash point” for volatility heading into the Presidential election.

NFIB Improves – Trump Bump?

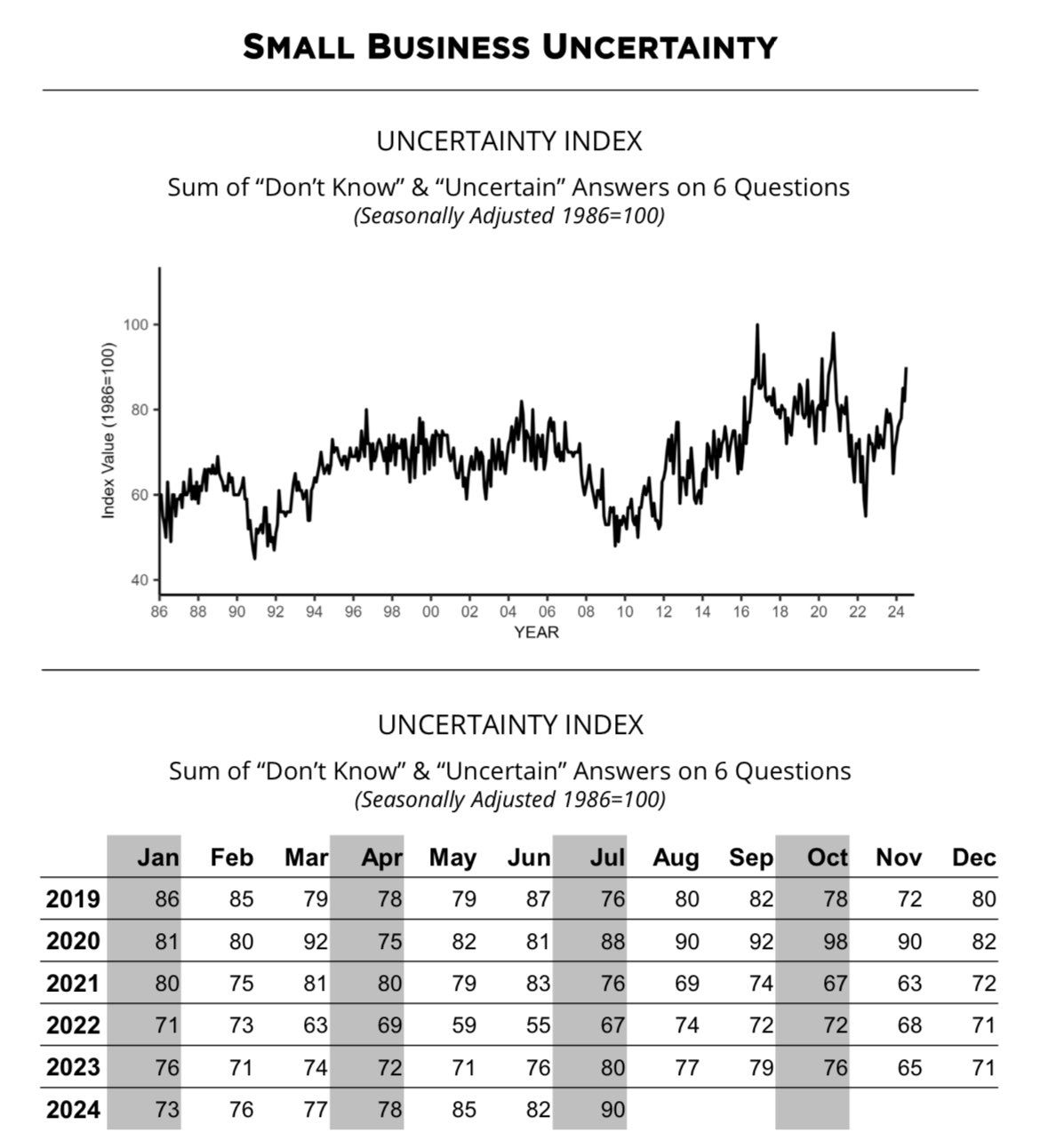

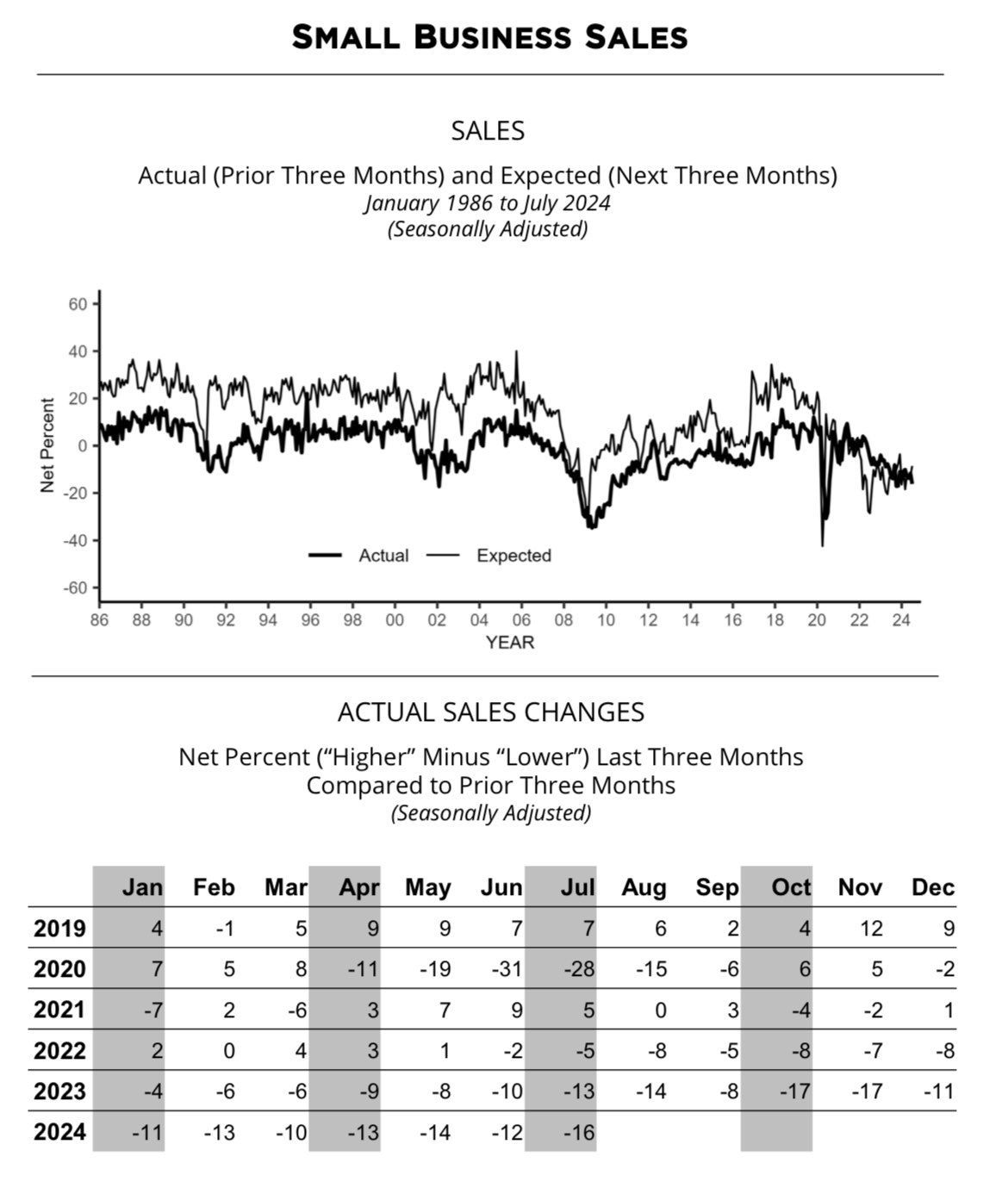

The NFIB small business survey was much better than expected, jumping to 93.8 versus 91.5 a month ago. As shown in the first graph below, the improvement is positive, but the level is still well below normal. However, the readings within the survey results are not as optimistic as the headline. For example, economic uncertainty has risen to levels last seen in 2020. Moreover, a net 16% of those surveyed saw a decline in sales over the past three months. That is about four points worse than last month.

Two factors may explain the strong headline result and weak underlying data.

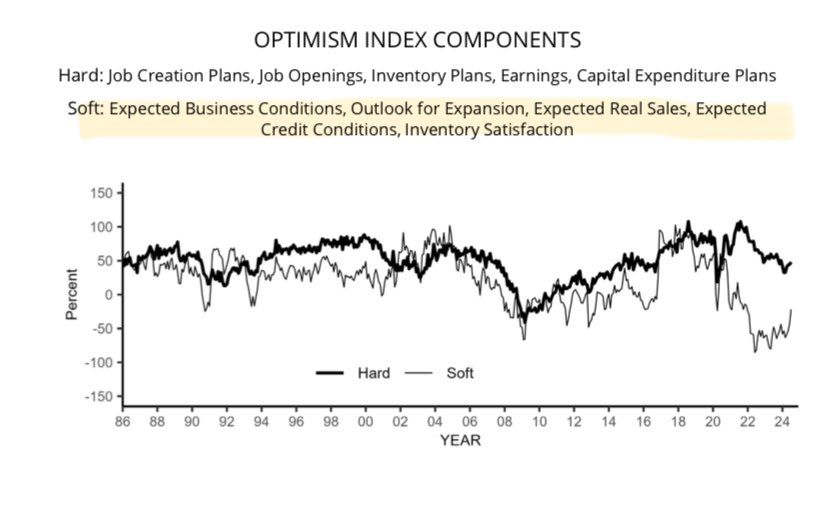

First, the bump in confidence aligns with a surge in Donald Trump’s polling numbers following the assassination attempt. Small business owners tend to favor the Republican party. Thus, confidence that Trump appeared to be a lock for president was running high. Furthermore, consider the bump primarily occurred in the “soft” indicators, as shown in the fourth graph. These include expectations. Based on current earnings, hiring plans, and capital expenditures, the hard results did not jump nearly as much. With the presidential race seemingly back to even, next month’s results will help us appreciate if the positive result was a “Trump Bump.”

The second factor boosting optimism is interest rates. Many small businesses are heavily indebted and often find it harder to get credit. Thus, expectations for lower interest rates and easier credit conditions should also create optimism for some small business owners.

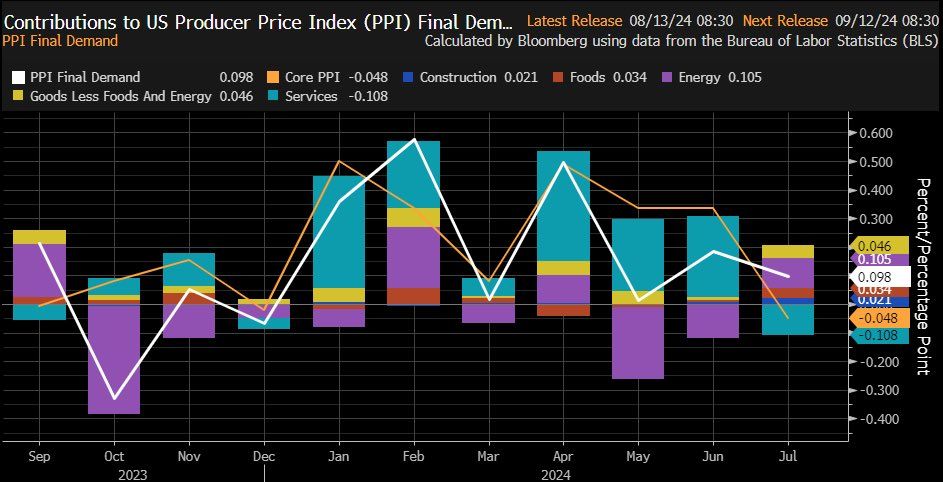

PPI Cools

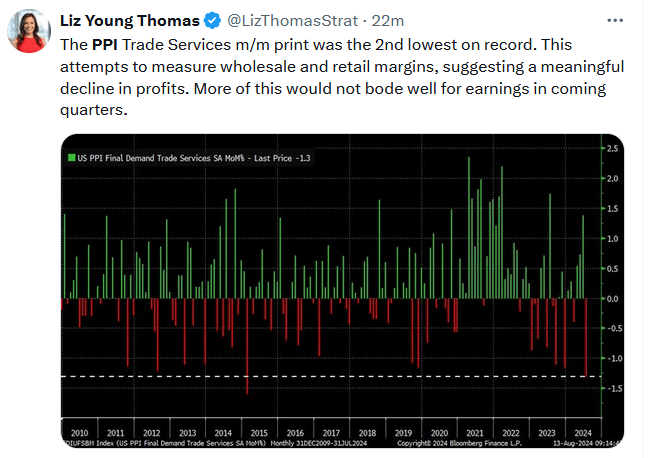

PPI came in lower than expected across the board. The headline monthly figure rose 0.1%, a tenth below expectations. Core PPI was 0.0%, which brought down the year-over-year core PPI from 3% to 2.4%. Assuming today’s CPI print is tame, the case for a September rate cut strengthens. The graph below shows that the PPI would likely have been slightly negative without energy prices. The Tweet of the day shows corporations are having a much more difficult time passing on inflation to their customers. Ergo, profit margins, and, ultimately, earnings are at risk for some companies.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”