Trending

I received many emails and questions on “why” we are adding the U.S. Treasury bond to our portfolios. The question is understandable, given its dire performance in 2022, where bonds had the biggest drawdown since 1786.

However, there is, as they say, “more to the story than meets the eye.”

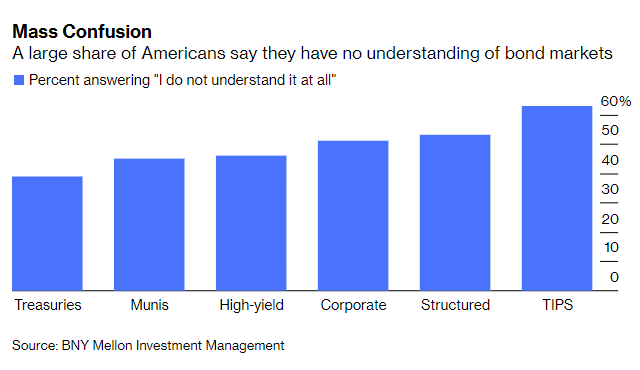

A previous survey from BNY Mellon shows that very few people understand the bond market and how it works.

“A BNY Mellon Investment Management national survey on fixed-income investing was stunning: A measly 8% of Americans were able to accurately define fixed-income investments.“

Such is not surprising since the financial media focuses only on the “sexier” side of the business – equities.

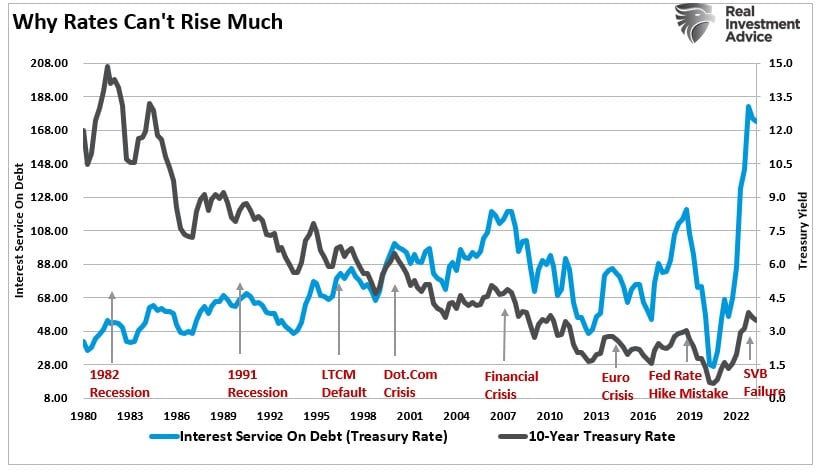

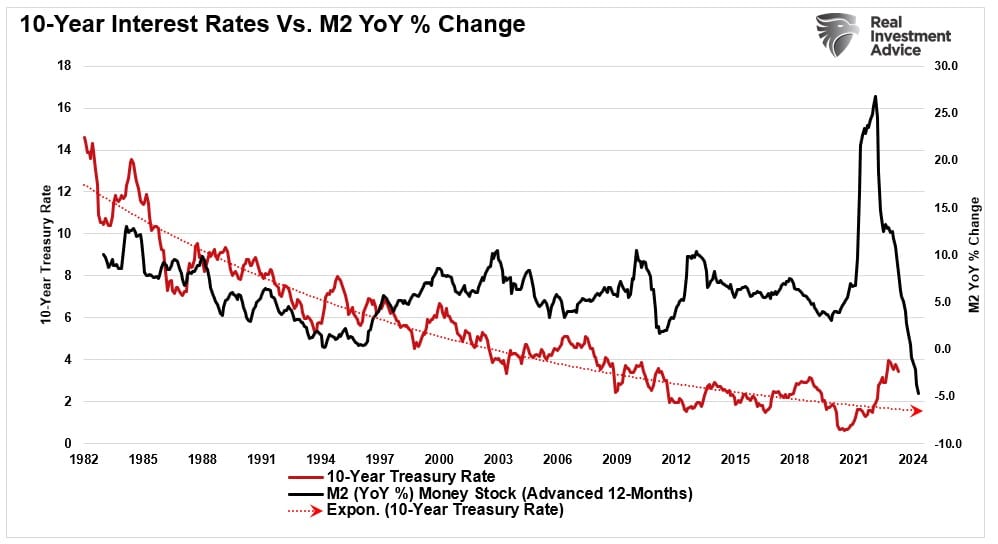

However, bonds are necessary from the investment perspective and the economic view. As we have discussed previously, low-interest rates are a function of an overly indebted economy. If rates rise too much, bad things have historically happened.

“The chart below is the interest service ratio on total consumer debt. (The graph is exceptionally optimistic as it assumes all consumer debt benchmarks to the 10-year treasury rate.) While the media proclaims consumers are in great shape because interest service is low, it only takes small increases in rates to trigger a ‘recession’ or ‘crisis’ event.”

Of course, as noted, interest rates reflect economic growth. As economic growth slows and disinflationary pressures present themselves, rates will ultimately track economic growth lower.

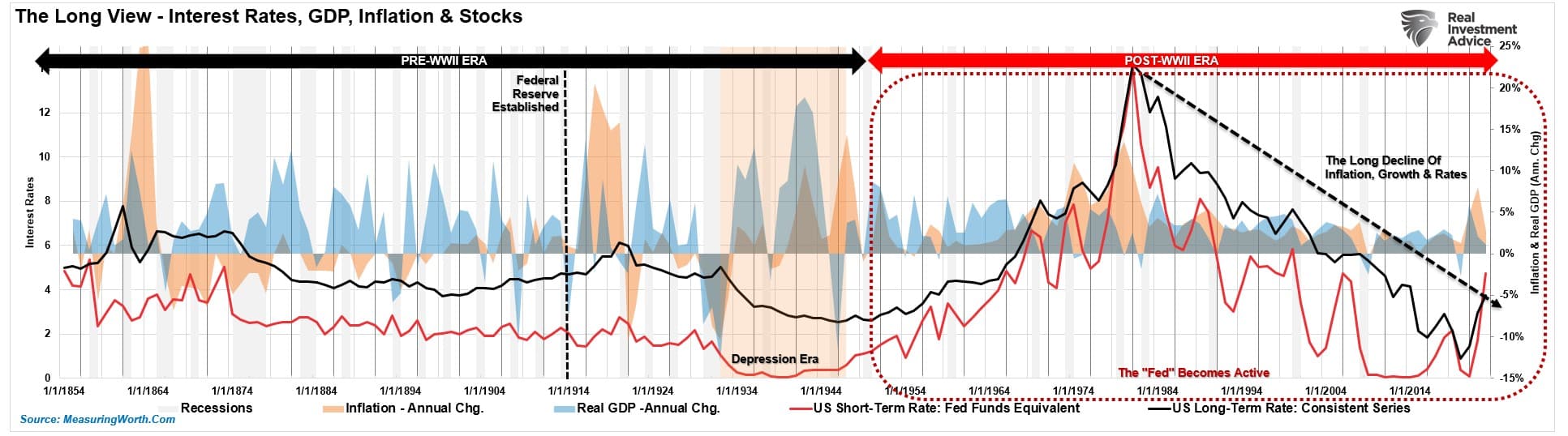

A Long History Of Rates & Economic Growth

The chart below shows a VERY long view of interest rates in the U.S. since 1854.

As noted, interest rates are a function of the general economic growth and inflation trend. More robust growth and inflation rates allow higher borrowing costs to be charged within the economy. Such is why bonds can’t be overvalued. To wit:

“Unlike stocks, bonds have a finite value. At maturity, the principal gets returned to the lender along with the final interest payment. Therefore, bond buyers know the price they pay today for the return they will get tomorrow. As opposed to an equity buyer taking on investment risk, a bond buyer is loaning money to another entity for a specific period. Therefore, the interest rate takes into account several risks:”

- Default risk

- Rate risk

- Inflation risk

- Opportunity risk

- Economic growth risk

“Since the future return of any bond, on the date of purchase, is calculable to the 1/100th of a cent, a bond buyer will not pay a price that yields a negative return in the future. (This assumes a holding period until maturity. One might purchase a negative yield on a trading basis if expectations are benchmark rates will decline further.) “

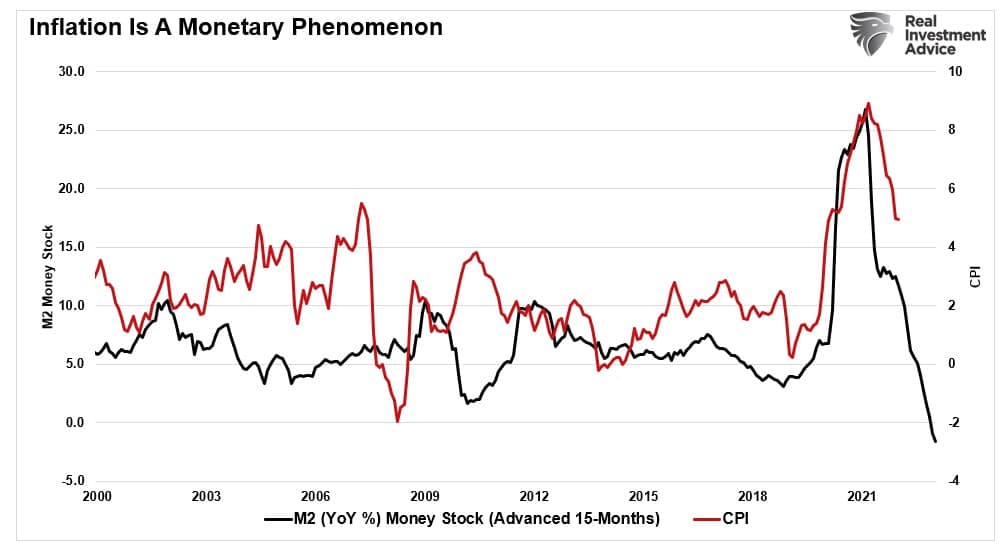

Therefore, it was unsurprising that the recent inflation surge preceded higher interest rates. However, that inflation push was artificial from massive monetary interventions. As monetary inputs fade, disinflation will push yields lower.

Disinflation from the contraction of liquidity will coincide with slower economic growth and, as noted above, lower interest rates.

Buy Bonds For Capital Appreciation & Protection

Understanding the dynamics between inflation, economic, and interest rates is a critical backdrop to understanding why now is likely the opportunity to increase bond exposure in portfolios for both income and capital appreciation. Most people view bonds as an income-only investment. With yields low, why own bonds? However, there is another aspect to bonds; capital appreciation.

There is an inverse relationship between bond prices and interest rates. When interest rates are low and rising, bond prices fall. However, when they are high and falling, bond prices rise.

In our portfolio management process, we buy bonds for three reasons:

- Capital appreciation – the same reason we buy equities

- Total return – interest income plus capital appreciation

- Risk reduction – lower volatility assets to offset higher volatility assets (equities.)

If you consider bonds as an “asset class,” the analysis changes from an income strategy to a capital appreciation opportunity.

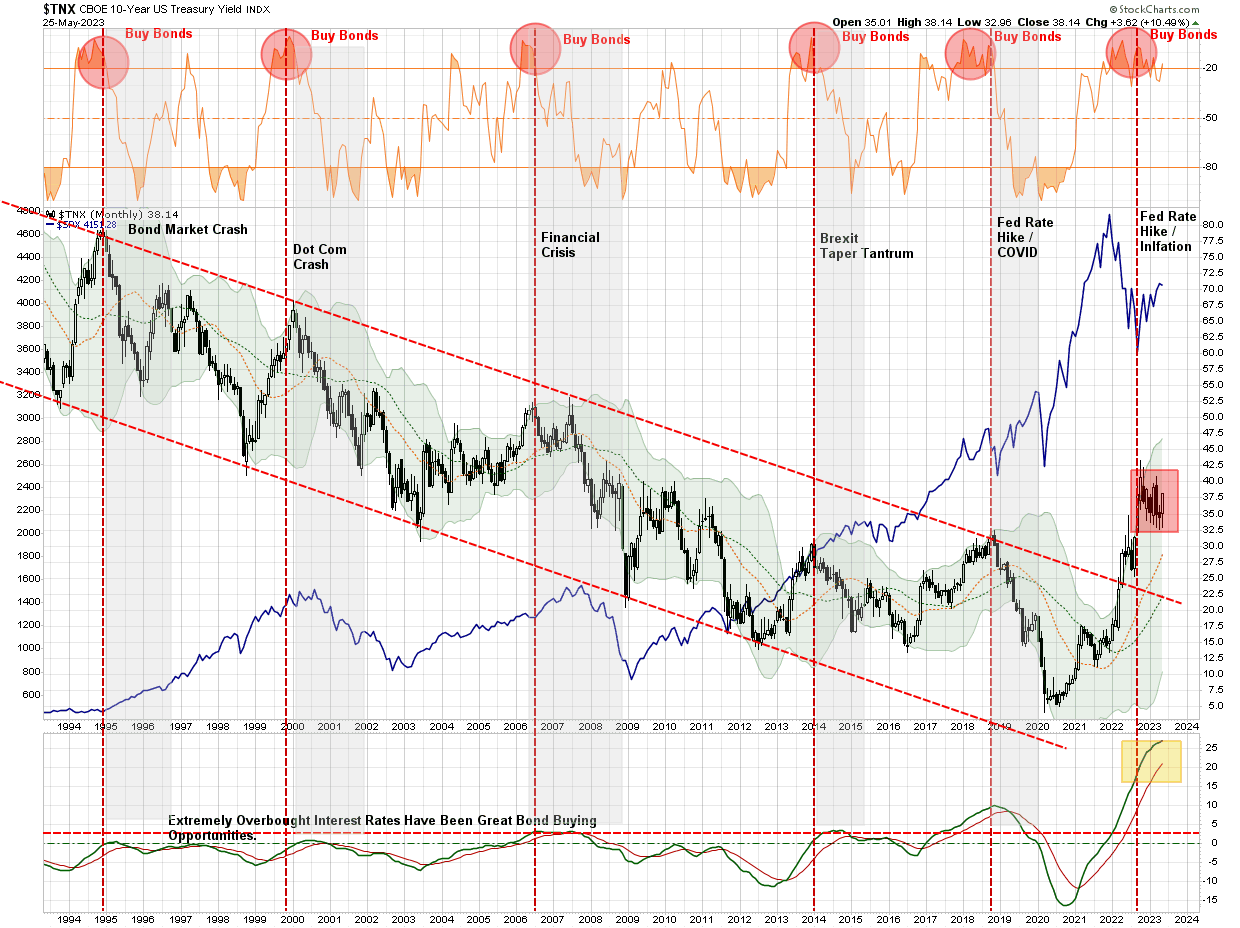

Using a monthly chart, treasury bonds are at a critical oversold juncture. Historically, when bonds were this oversold such coincided with a financial event or recession. Such is not surprising given, as noted above, the impact of higher rates on a highly leveraged economy.

Since interest rates are the inverse of bond prices, we can look at this long-term chart of rates to determine when Treasury bonds are overbought or oversold.

- In 2018, rates slid lower as the realization that Fed rate hikes would negatively impact economic growth and financial stability.

- As 2019 progressed, the yield curve inverted, pushing rates lower as investors sought safety.

- In March 2020, as the pandemic raged, the demand for safety caused rates to plunge to record lows.

- In 2021, rates surged as stimulus-induced inflation surged.

Historically, bonds are the beneficiary of a “risk-off” rotation during market downturns. Such not only provides a return but reduces overall portfolio volatility.

Conclusion

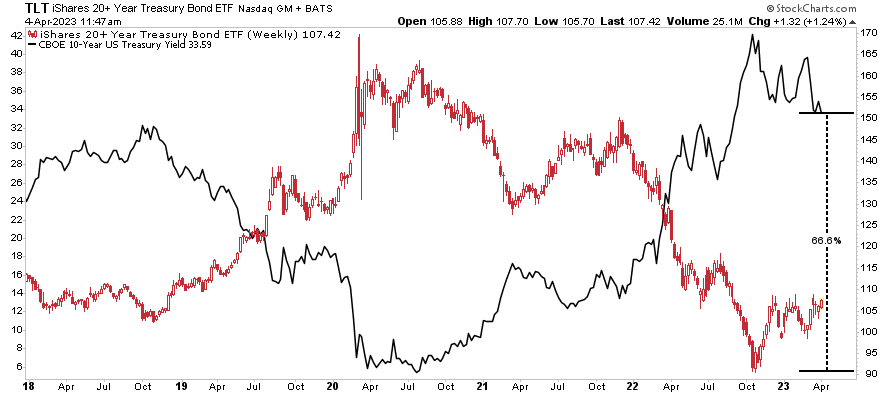

The hope is that the Fed will again start dropping interest rates. However, as we have noted previously, the only reason for the Fed to cut rates would be to offset the risk of an economic recession or a financially related event. Should such occur, the “risk off” rotation would cause a drop in rates toward the pandemic-era lows. Such a decline would imply an increase in bond prices of approximately 50%.

In other words, the most hated asset class of 2022 may outperform stocks by a large margin if a recession occurs.

So, yes, we are opportunistically buying bonds for our portfolio.