Trending

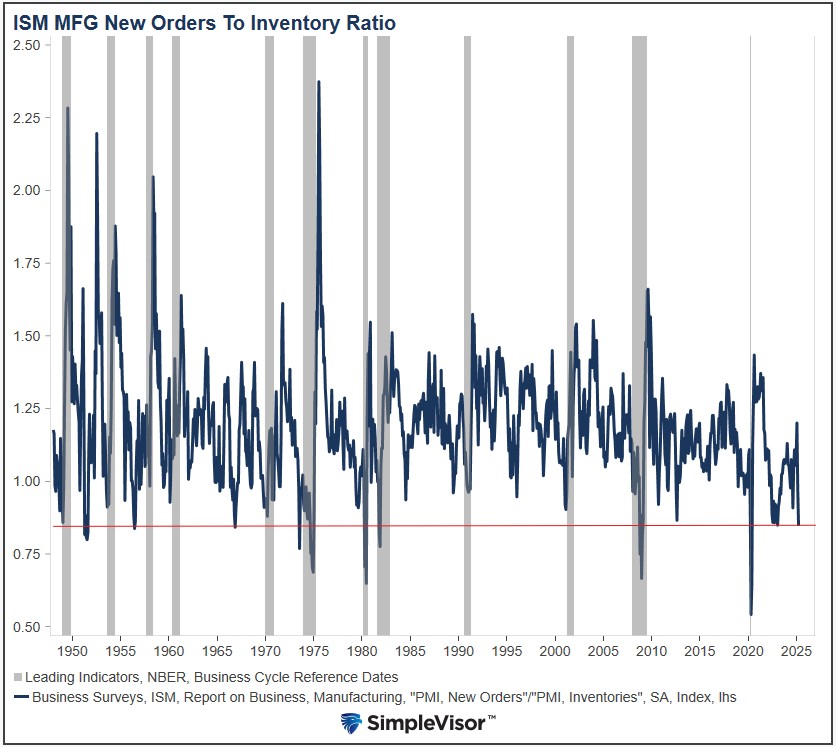

Over the past few weeks, we have discussed the sharp jump in the trade deficit due to a surge of imports trying to front-run potential tariffs. Thus far, the impact of front-running tariffs on economic data has only been significant in consumer and corporate surveys and the aforementioned trade deficit. That was until Tuesday. The ISM manufacturing data showed that new orders fell to their lowest level in over two years. At the same time, inventories rose to three-year highs. Simply, manufacturers stockpiled more goods than customer orders would typically dictate. The graph below clearly shows how manufacturers are gearing up for the impact of the tariffs. The ratio of ISM Manufacturing new orders to inventories is near its lowest level in the last 75 years and at levels frequently associated with a recession.

Now what? This is incredibly difficult to answer until the tariffs are announced and negotiated. This could be a multi-month process. In the meantime, manufacturers have excessive stocks of some inventory. At the same time, new orders are likely to be less than usual as end users are dealing with the impact of the tariffs. We suspect inventories will remain high and new orders low. Thus, due to bloated inventories, manufacturers will likely import less than normal over the coming months. While some manufacturers will be in limbo, the result should be a boost to GDP, likely offsetting the current weaknesses due to tariffs’ impact on the trade imbalance.

What To Watch

Earnings

Economy

Market Trading Update

Yesterday, we discussed the potential buy imbalance of institutional CTAs but the limits of any rally due to the current overhead resistance levels. After the close, the White House revealed its final tariff plans for the world, which the markets will deal with this morning. The result of that announcement doesn’t change much technically, as the upside still likely remains limited, and many investors trapped in the recent selloff are looking for an exit. With some certainty now present over tariffs, the markets’ next move will depend on the estimated impacts of those tariffs on earnings. We suspect that while there is downside risk to the market ahead, given the current oversold market conditions and highly negative sentiment, a rally is likely. That rally could be substantial, pushing markets back to their weekly moving averages, which would reverse investor sentiment. Given the weakening economic data, there is a risk that any rally will be met with more selling during the summer months as the markets fish for a more sustainable bottom based on reduced earnings estimates.

While the break of that running trend line support and the convergence of the moving averages are more bearish in the near term, this does not mean an aggressive bear market is forthcoming. We have seen these negative crossovers previously. The difference between whether those crossovers evolved into a larger bear market cycle or just remained a correction was whether there was a recession or credit-related event simultaneously occurring.

We do not have evidence supporting the evolution into a bear market. Therefore, we should use rallies to rebalance risk and portfolio exposures but not become overly bearish on outlooks or positioning. After today, we will see how the markets interpret the tariff announcement, and we can then technically assess our next moves for the market.

The Problem With $50 Oil

The Dallas Fed publishes a quarterly survey of energy producers. Appropriately, the first quarter of the 2025 edition included a special question on break-even oil prices. The first question asked what price crude oil (WTI) must be above to cover the expenses of running existing wells. Accordingly, the graph and the quote below summarize the answers.

The average price across the entire sample is approximately $41 per barrel, up from $39 last year. Across regions, the average price necessary to cover operating expenses ranges from $26 to $45 per barrel. Almost all respondents can cover operating expenses for existing wells at current prices.

The second question asked the oil price required to drill a new well. The average answer was $65, one dollar higher than last year. Further, the graph below shows the average range, which spans from $61 to $70 a barrel.

So, what might the impact be if Donald Trump can get oil prices to $50 a barrel as he has warned? Below are a few survey responses:

- There cannot be “U.S. energy dominance” and $50 per barrel oil; those two statements are contradictory.

- At $50-per-barrel oil, we will see U.S. oil production start to decline immediately and likely significantly (1 million barrels per day plus within a couple quarters).

- The administration’s chaos is a disaster for the commodity markets.

- “Drill, baby, drill” is nothing short of a myth and populist rallying cry.

- I have never felt more uncertainty about our business in my entire 40-plus-year career.

- Global geopolitical unrest and the uncertain economic outcomes of the administration’s tariff policies suggest the need to hit the pause button on spending.

Trump’s Puzzle

We are big fans of Sunday crossword puzzles, which tend to be bigger and more challenging than the weekday format. Adding to their allure, most Sunday puzzles have a clever theme, typically three or four clues whose answers stretch across the puzzle. Solving the theme often makes a complex puzzle a little easier. Like a crossword puzzle, President Donald Trump has been bombarding the media with clues about his economic policy, particularly his plans to fight inflation and reduce interest rates.

Given the importance of inflation and interest rates to the economy and the financial markets, it’s worth assessing his clues and formulating some answers about what Donald Trump may be up to.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: How Personal Savings Reveal Economic Sentiment Beyond Political Bias