Trending

It’s now official that the recession of 2020 was the shortest in history.

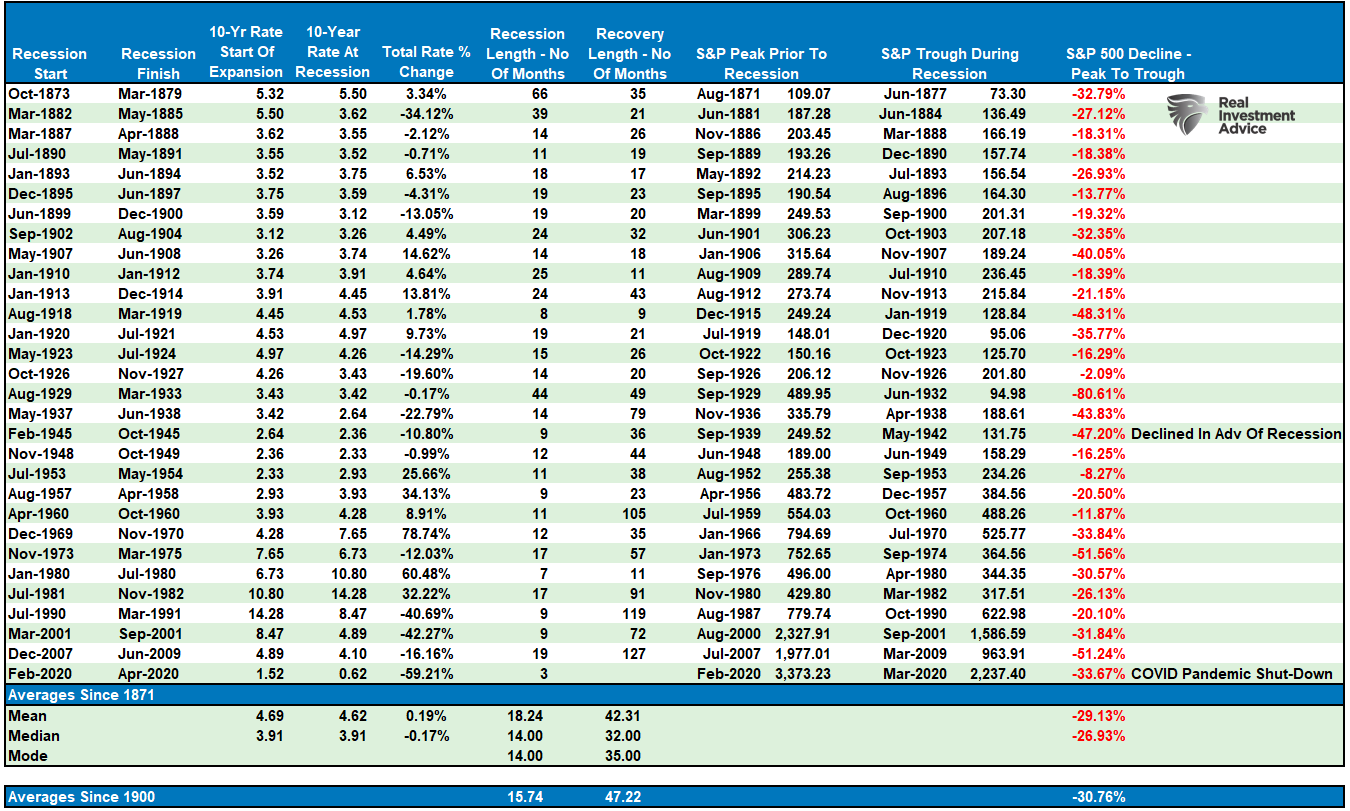

According to the National Bureau of Economic Research, the contraction lasted just two months, from February 2020 to April 2020. However, during those two months, the economy fell by 31.4% (GDP), and the financial markets plunged by 33%. Both of those declines, as shown in the table below, are within historical norms.

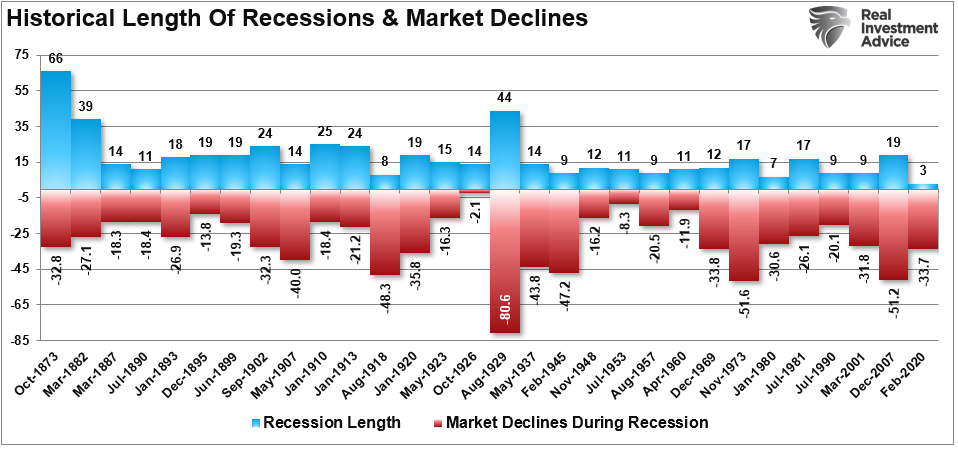

Here it is graphically. The chart shows the historical length of each recession and the corresponding market decline.

However, while the effects of the “recession” were all within historical norms, the recession itself was not.

Let me explain.

A Non-Standard Recession

The statement from the NBER is as follows:

“In determining that a trough occurred in April 2020, the committee DID NOT conclude that the economy has returned to operating at normal capacity. The committee decided that any future downturn of the economy would be a new recession and not a continuation of the recession associated with the February 2020 peak. The basis for this decision was the length and strength of the recovery to date.”

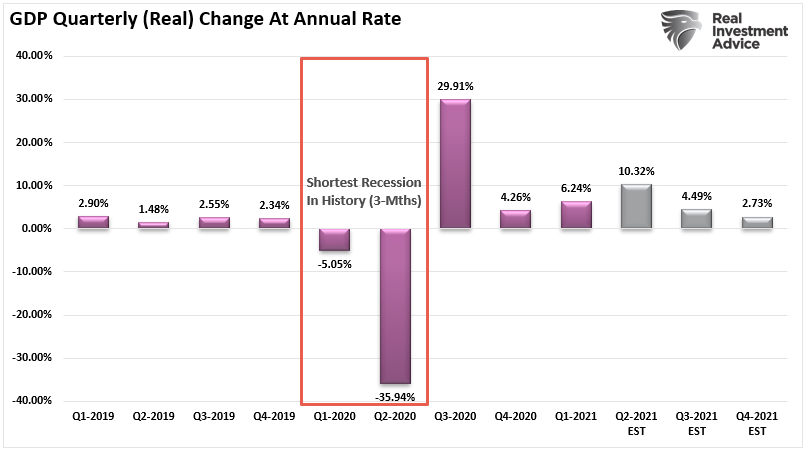

As I said, the recession was non-standard. Conventionally, the NBER defines a recession as two consecutive quarters of negative GDP growth. Notably, while the recession did technically meet the criteria after GDP fell 5% in Q1, recessions tend to last more than three months historically.

The difference was the massive interventions of 20% of GDP beginning in Q2, which created an “artificial growth surge” in the economy by pulling forward consumptive activity. That led to an explosive recovery in GDP in Q3 of nearly 30%.

It is essential to note that the NBER stated that any subsequent downturn would get labeled as a “new” recession. That view accounts for the recovery driven by massive interventions even though that growth is not sustainable.

As such, the “next recession” may not be as far off as many currently expect.

Why Recessions Are Important

Our discussion must begin with a basic concept: “recessions” are not a “bad thing.”

It is a given you should never mention the “R” word. People immediately assume you mean the end of the world: death, disaster, and destruction. But, unfortunately, the Federal Reserve and the Government also believe recessions “are bad.” As such, they have gone to great lengths to avoid them.

However, what if “recessions are a good thing,” and we just let them happen?

“What about all the poor people that would lose their jobs? The companies that would go out of business? It is terrible to think such a thing could be good.”

Sometimes destruction is a “healthy” thing, and there are many examples we can look to, such as “forest fires.”

Wildfires, like recessions, are a natural part of the environment. They are nature’s way of clearing out the dead litter on forest floors, allowing essential nutrients to return to the soil. As the soil enrichens, it enables a new healthy beginning for plants and animals. Fires also play an essential role in the reproduction of some plants.

Ask yourself this question: “Why California has so many wildfire problems?”

Is it just bad luck and negligence? Or, is it decades of rushing to try and stop fires from their natural cleansing process as noted by MIT:

“Decades of rushing to stamp out flames that naturally clear out small trees and undergrowth have had disastrous unintended consequences. This approach means that when fires do occur, there’s often far more fuel to burn, and it acts as a ladder, allowing the flames to climb into the crowns and takedown otherwise resistant mature trees.

While recessions, like forest fires, have terrible short-term impacts, they also allow the system to reset for healthier growth in the future.

No Tolerance For Recessions

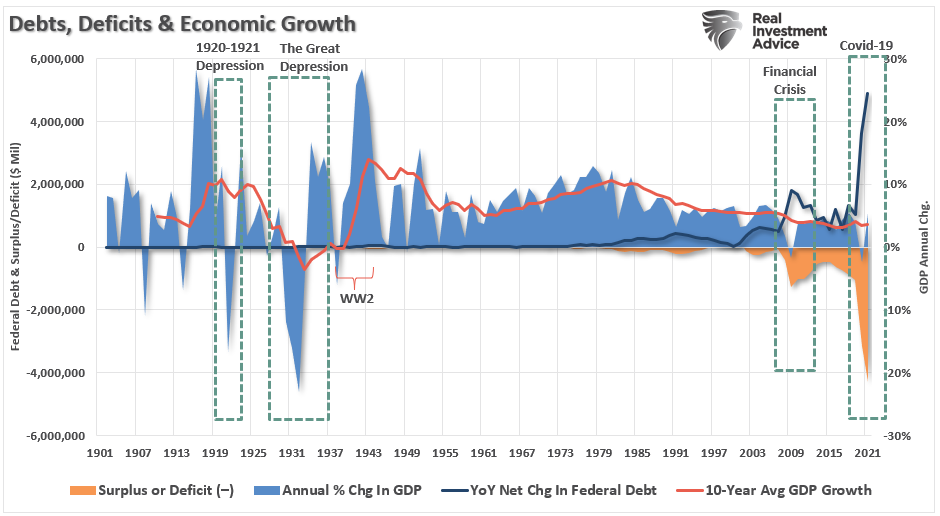

Following the century’s turn, the Fed’s “constant growth mentality” not only exacerbated rising inequality but fostered financial instability. Rather than allowing the economy to perform its Darwinian function of “weeding out the weak,” the Fed chose to “mismanage the forest.” The consequence is that “forest fires” are now more frequent.

Deutsche Bank strategists Jim Reid and Craig Nicol previously wrote a report that echos this analysis.

“Actions are taken by governments and central banks to extend business cycles and prevent recessions lead to more severe recessions in the end.”

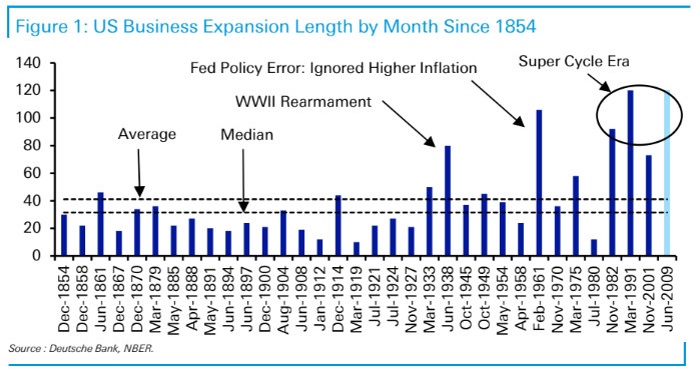

Prolonged expansions had become the norm since the early 1970s, when President Nixon broke the tight link between the dollar and gold. The last four expansions are among the six longest in U.S. history .

Why so? Freed from the constraints of a gold-backed currency, governments and central banks have grown far more aggressive in combating downturns. They’ve boosted spending, slashed interest rates or taken other unorthodox steps to stimulate the economy.” – MarketWatch

But therein also lies the problem.

The Darwinian Process Of Recessions

As we discussed in our series on “Capitalism,” if allowed to operate, is a “Darwinian System.” As with Darwin’s theory of evolution, corporate evolution has the same essential components as biological evolution: competition, adaptation, variation, overproduction, and speciation. In other words, as an economic system, companies either adapt, evolve, and survive or become extinct.

However, in 2008, the Government and Federal Reserve began a process of “bailing” out companies that should have been allowed to go “bankrupt.” The consequence of that process is the failure to enable the system to “clear itself” of the excess debt, which diverts capital away from productive uses.

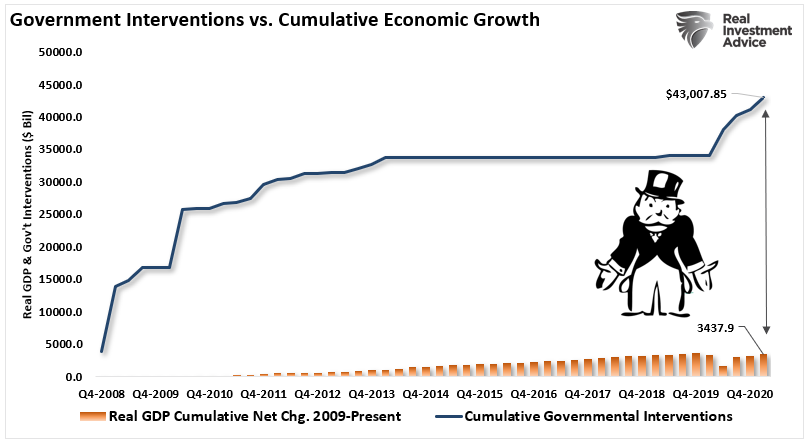

I have illustrated the continual increases in debt used to create minimal economic growth. Specifically, since 2008, the Federal Reserve and the Government have pumped more than $43 Trillion into the economy. But, in exchange, that debt generated just $3.5 trillion in economic growth, or rather, $12 of monetary stimulus for each $1 of growth. Such sounds okay until you realize it came solely from debt issuance.

As Ruchir Sharma previously penned:

“Modern society looks increasingly to government for protection from major crises. Whether recessions, public-health disasters or, as today, a painful combination of both. Such rescues have their place. Few would deny that the Covid-19 pandemic called for dramatic intervention. But there is a downside to this reflex to intervene, which has become more automatic over the past four decades. Our growing intolerance for economic risk and loss is undermining the natural resilience of capitalism and now threatens its very survival.”

Such is an important concept to comprehend.

Just as poor forest management leads to more wildfires, not allowing “creative destruction” to occur in the economy leads to a financial system that is more prone to crises.

Structural Fagility

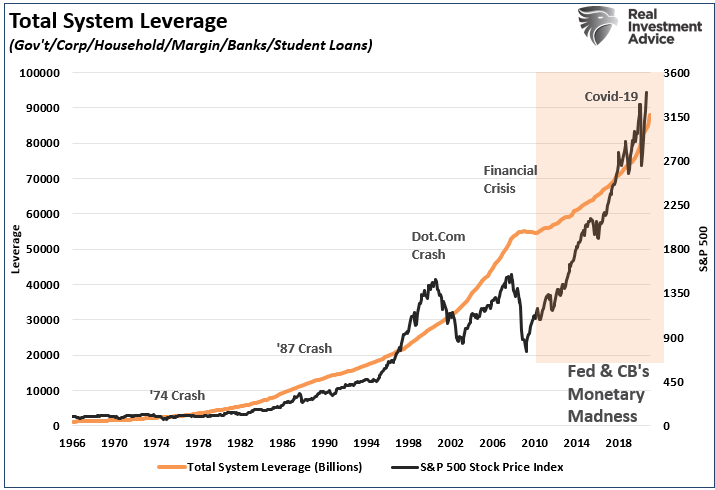

Given the structural fragility of the global economic and financial system, policymakers remain trapped in the process of trying to prevent recessions from occurring due to the extreme debt levels. Unfortunately, such one-sided thinking ultimately leads to skewed preferences and policymaking.

As such, the “boom and bust” cycles will continue to occur more frequently at the cost of increasing debt, more money printing, and increasing financial market instability.

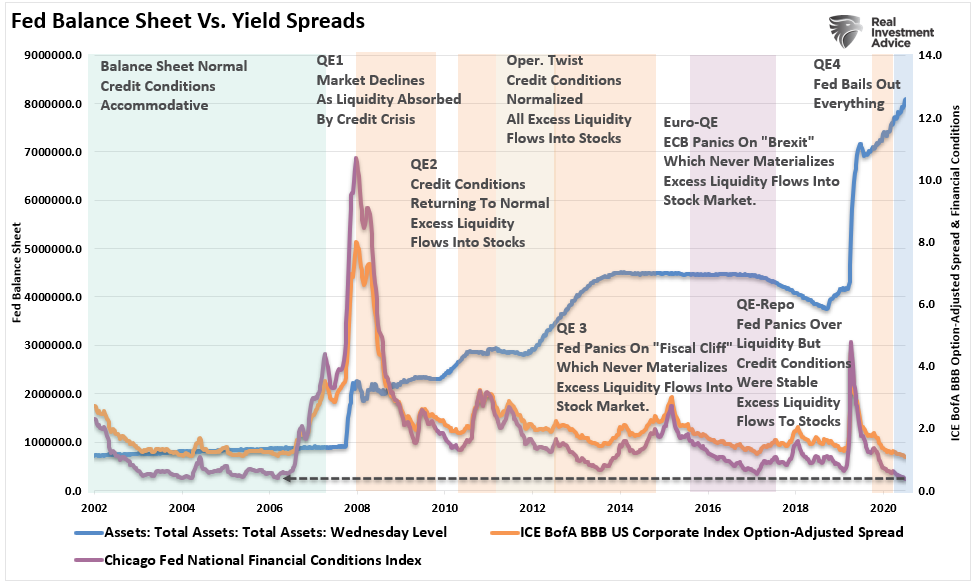

It is clear the Fed’s foray into “policy flexibility” did extend the business cycle. However, those extensions led to higher structural budget deficits. The cancerous byproduct of increased private and public debt, artificially low-interest rates, negative real yields, and inflated financial asset valuations is problematic.

However, these policies have all but failed to this point. From “cash for clunkers” to “Quantitative Easing,” economic prosperity worsened. Pulling forward future consumption, or inflating asset markets, exacerbated an artificial wealth effect. Such led to decreased savings rather than productive investments.

The Fed’s “Moral Hazard”

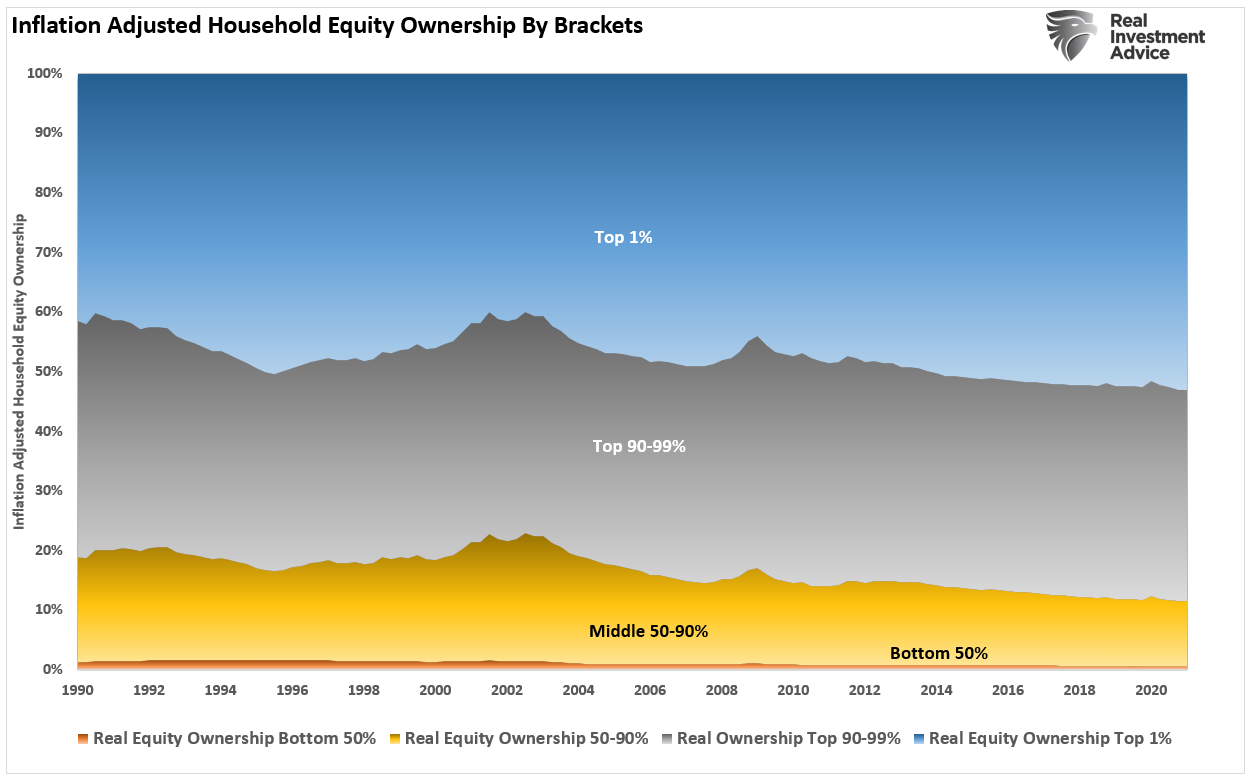

A growing body of research shows that constant government stimulus is a significant contributor to many of modern capitalism’s most glaring ills. Wealth inequality is the most obvious.

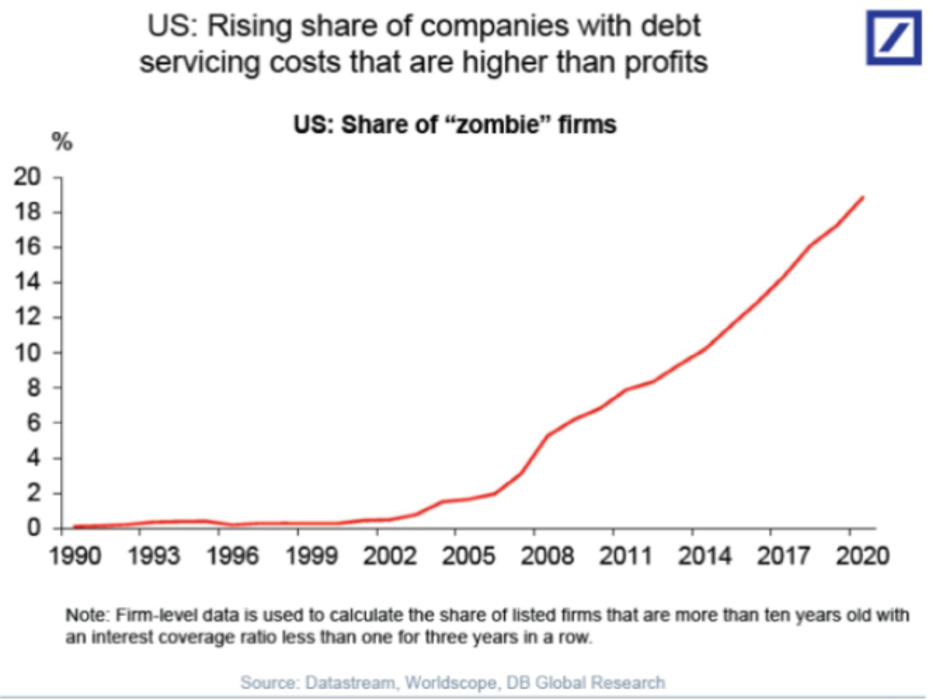

However, another more important but not noticeable side effect is that it keeps alive heavily indebted “zombie” firms.

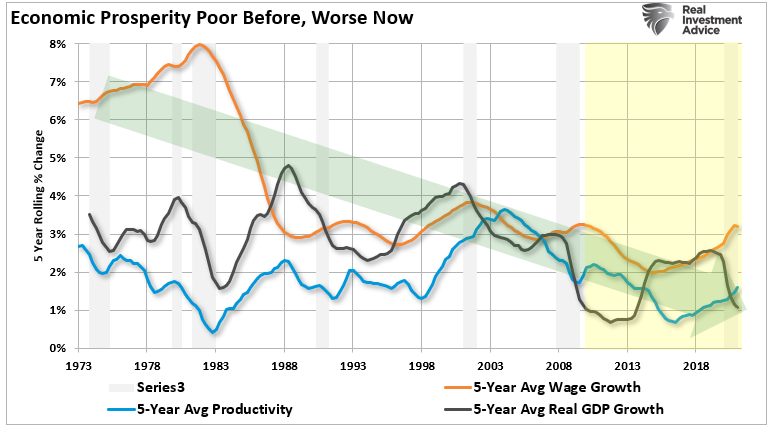

When a company is “kept alive,” it comes at the expense of startups, which typically drive innovation. All of this leads to lower productivity which is the prime contributor to the slowdown in economic growth and a shrinking pie for everyone. (See chart above.)

By not allowing “recessions” to perform their natural “Darwinian” function of “weeding out the weak,” it creates a macroeconomic problem. As previously noted by Axios:\

“Zombie firms are less productive, and their existence lowers investment in, and employment at, more productive firms. In short, a side effect of central banks keeping rates low for a long time is it keeps unproductive firms alive. Ultimately, that lowers the long-run growth rate of the economy.”

If “recessions” are allowed to function, the weak players will fail. Stronger market players would acquire failed company assets. Bond-holders would receive some compensation for their debt holdings. Shareholders, the ones who accepted the most risk, would get wiped out.

Furthermore, assuming capitalism was allowed to function, investors would require appropriate compensation for the risk when loaning money to companies. As such, credit-related investors would get compensated for their risk rather than the current state of abnormally low yields for junk-rated debt.

The consequence, of course, is that since the “Darwinistic process” of a recession did not occur, and the macroeconomic system is even more fragile than previously, the next downturn could happen sooner than later.

The Next Recession

While the interventions certainly salvaged the economy from a more prolonged recessionary event, they also made the economy more fragile. Furthermore, by dragging forward future consumption, the interventions only gave the appearance of economic activity. As excess stimulus fades and assuming interventions don’t repeat, the economy will return its pre-covid growth trend of 2% or less.

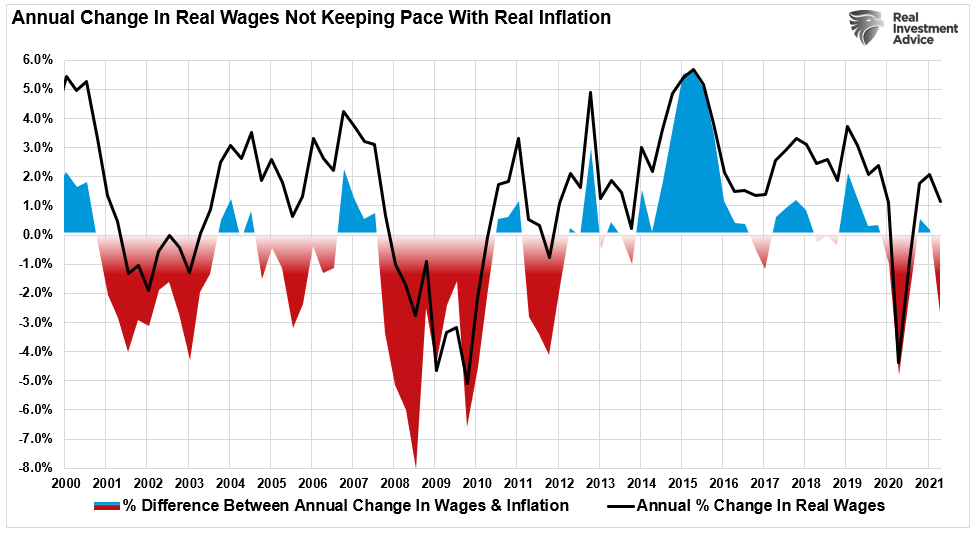

Such should not be a surprise given that economic growth is roughly 70% consumption. With wage growth well below inflationary pressures, consumption will get impacted by higher prices.

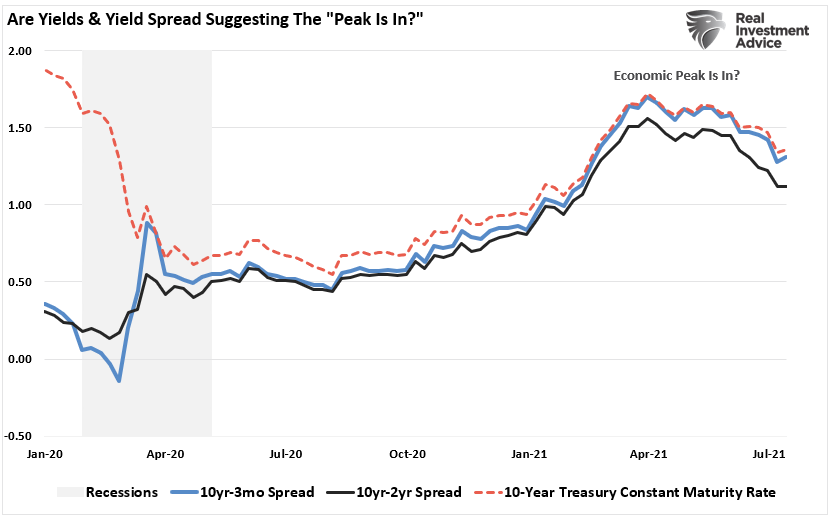

With Treasury yields dropping and the yield curve reversing, these are early warning signs that economic growth is indeed slowing.

While the NBER declared the 2020 recession the shortest in history, such does not preclude another recession from occurring sooner than later.

All the excesses that existed before the last recession have only worsened since then.

- Excess Debt

- High Stock Market Valuations

- Investor Complacency

- Financial System Fragility

- Weak Economic Underpinnings

- Declining Monetary Velocity

- Low Interest Rates Detering Productive Activity

- Financial Liquidity Required To Keep Asset Prices Elevated

Given the dynamics for an economic recession remain, it will only require an unexpected, exogenous event to push the economy back into contraction.

Such is why the NBER is clear in saying they will classify the next downturn as a separate recession.

If you are quick to dismiss the idea, remember no one expected a recession in 2020 either.

But we did warn you about it in 2019.

Related: