We’ve previously written that electricity demand is projected to outpace capacity over the next decade. The 20-year power purchase agreement signed between Microsoft and Constellation Energy, announced last Friday, highlights the potential for nuclear energy to meet the surging power demands from AI data centers. Constellation Energy will reopen the Three Mile Island reactor shuttered in 2019 to supply clean energy to Microsoft’s AI data centers by early 2028.

Nuclear power plants and AI data centers are ideal matches since both must run 24/7. Another cloud computing giant recently made a similar move. In March of this year, Amazon agreed to a deal to acquire a data center campus connected to a nuclear power plant on the Susquehanna River. Constellation Energy (CEG) has the potential to be a large beneficiary of the renewed interest in nuclear power, producing over 20% of the nation’s output. Another potential player is NextEra Energy (NEE), which is considering reopening a nuclear power center in Iowa that closed in 2020, per the Wall Street Journal.

What To Watch

Economy

Market Trading Update

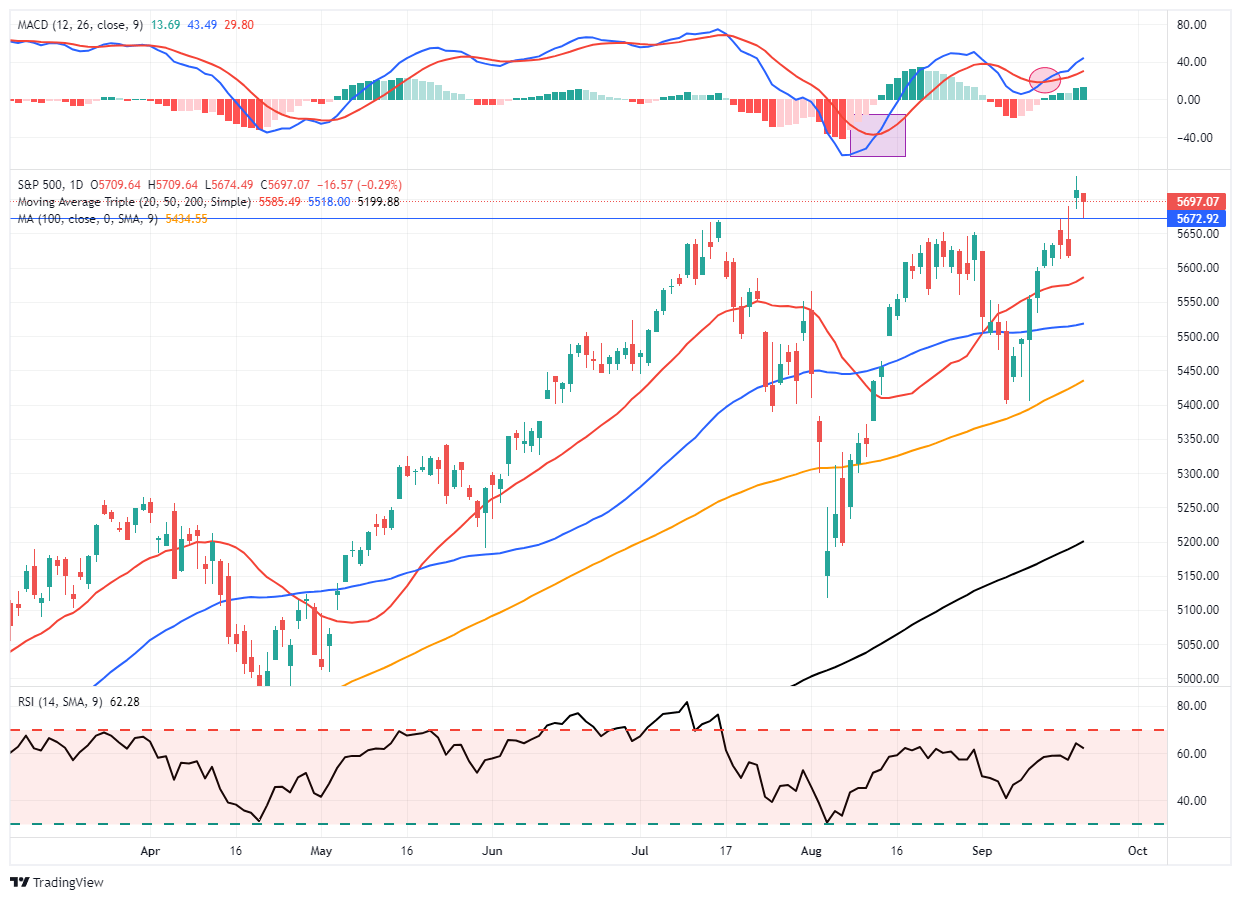

As noted last week, the trend of higher lows and the triggering of the MACD “buy signal” all suggested the recent correction phase was over. That was confirmed this past week, as the market broke out to new all-time highs following the 50 basis point cut in the Federal Reserve overnight lending rate on Wednesday.

The market has continued to front-run the Fed’s rate cuts during the last two years. Each rally turned to disappointment as the Fed postponed while continuing to fight inflation. However, this past week, that battle was won. The question is, what happens next? A recent table from Carson Investment Research shows that near-term performance has been a mixed bag when the Federal Reserve has previously cut rates within 2% of all-time highs. However, returns over the next year are positive 100% of the time.

The difference in returns is whether there was a recession or not. There is little concern about a recession over the next 12 months, which should help support asset prices. However, since there are no guarantees, it is worth continuing to manage risk and maintain some hedges against a sharp pickup in volatility.

From a purely technical perspective, the market remains on a bullish buy signal and is not grossly overbought yet. On Friday, the market retested the breakout of the previous highs and held. Next week, if the market can hold these levels without breaking that support, the breakout will be confirmed, which should provide a bullish bias into the end of the month.

While the backdrop to the market is bullish, there is still some risk over the next month as we head into the beginning of earnings season and the November election. Speaking of earnings, analysts have been very busy downgrading estimates ahead of October.

Let me conclude: The bullish bias remains strong as the momentum chase continues. However, economic data, slowing earnings, and the upcoming election raise concerns. Risk management remains key, and we must be flexible in our positioning. Michael Lebowitz sent me a quote last week that I think sums up our views well:

“We don’t really care which way growth and inflation go. Not because it doesn’t impact our positioning, we’re just prepared to adjust.”

The Week Ahead

Federal Reserve speakers will be out in force following last week’s 50bps rate cut, the most notable of which will be Chair Powell’s speech on Thursday morning. The focus this week will be the August PCE price index on Friday. Both the headline and core PCE price indices are expected to rise 0.2% MoM, which is in line with July’s data. The Fed stated last week that it is growing more confident in the downward path of inflation. Thus, the August data has a low potential for a material upside surprise. However, the magnitude of last week’s rate cut may hint that a weak figure is in store.

This week’s economic data starts today with the September S&P Global PMI Flash. The Manufacturing PMI has weakened in recent months, while the Services PMI has continued showing strength. Thus, the composite remains well in expansionary territory. Eyes will be on the employment component for potential deterioration after both sectors reported a contraction in August. Especially with the Fed stating that it now considers inflation and employment risks balanced. August Durable Goods orders are released on Thursday. The consensus expects a decline of 2.8% MoM following the 9.9% surge in July.

Market Declines And The Problem Of Time

The average American faces a sobering reality: human mortality. Most investors don’t begin seriously saving for retirement until their mid-40s, as the cost of living during earlier years—college, getting married, having kids—consumes much of their income. Generally, incomes don’t exceed the cost of living until the mid-to late-40s, allowing for a serious push toward retirement savings. Most individuals have just 20 to 25 productive working years to achieve their investment goals.

Investment studies should align time frames with human mortality rather than focusing on “long-term” average returns. There are periods in history where real, inflation-adjusted total returns over 20 years have been close to zero or negative. Interestingly, these periods of near-zero to negative returns were typically preceded by high market valuations—as we see today.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”