Trending

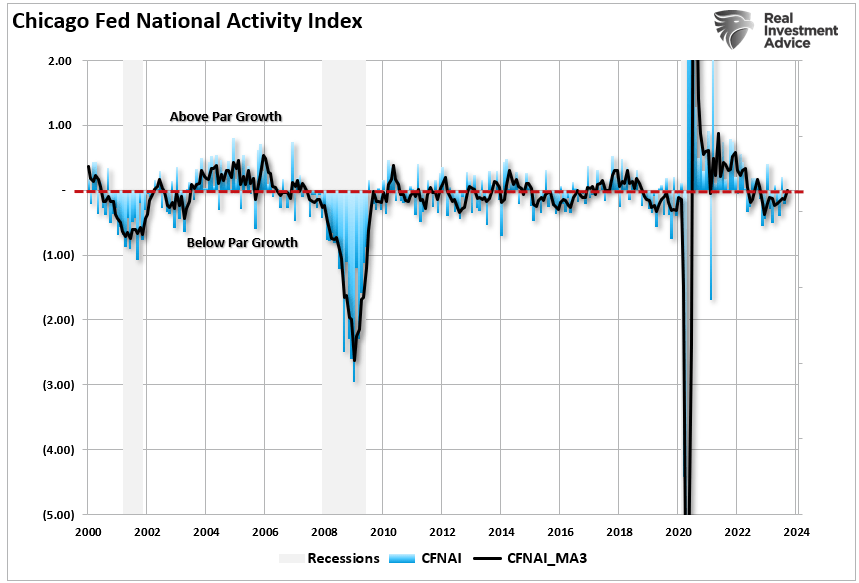

The Chicago Fed National Activity Index (CFNAI) is arguably one of the most important and overlooked economic indicators. Each month, economists, the media, and investors pour over various mainstream economic indicators, from GDP to employment and inflation, to determine what markets will likely do next.

While economic numbers like GDP or the monthly non-farm payroll report typically garner the headlines, the most crucial statistic, in my opinion, is the CFNAI. Investors and the press mostly ignore it, but the CFNAI is a composite index of 85 sub-components, giving a broad overview of overall economic activity in the U.S.

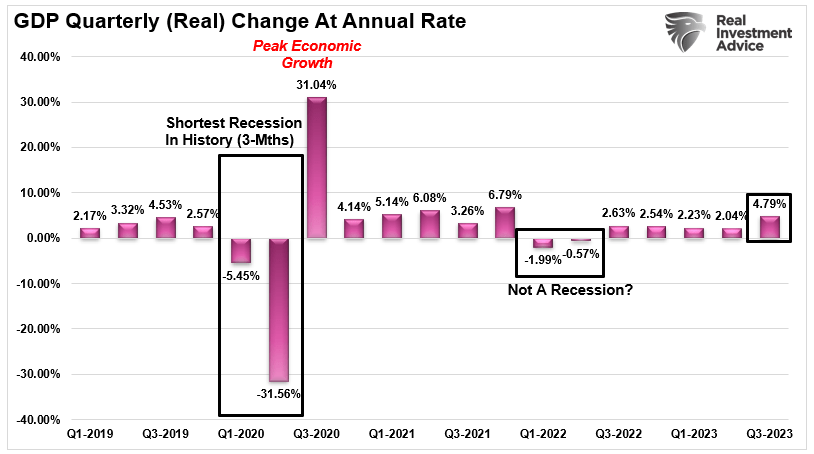

Since the beginning of this year, the markets ran up sharply over into July as the Federal Reserve again intervened in the markets to bail out regional banks. Then, even as the market pulled back this summer, economic growth accelerated in the 3rd quarter, according to the headlines, which should translate into a resurgence of corporate earnings. However, if recent CFNAI readings are any indication, investors may want to alter their growth assumptions heading into next year.

While most economic data points are backward-looking statistics, like GDP, the CFNAI is a forward-looking metric that indicates how the economy will likely look in the coming months.

Notably, that data does not support the recent economic report from the Bureau Of Economic Analysis (BEA), which showed the economy expanded by 4.9% in Q3.

So, what is the CFNAI telling us that is different than the BEA economic report?

Breaking Down The “Most Important Number”

Understanding the message the index is designed to deliver is critical. From the Chicago Fed website:

“The Chicago Fed National Activity Index (CFNAI) is a monthly index designed to gauge overall economic activity and related inflationary pressure. A zero value for the index indicates that the national economy is expanding at its historical trend rate of growth; negative values indicate below-average growth; and positive values indicate above-average growth.“

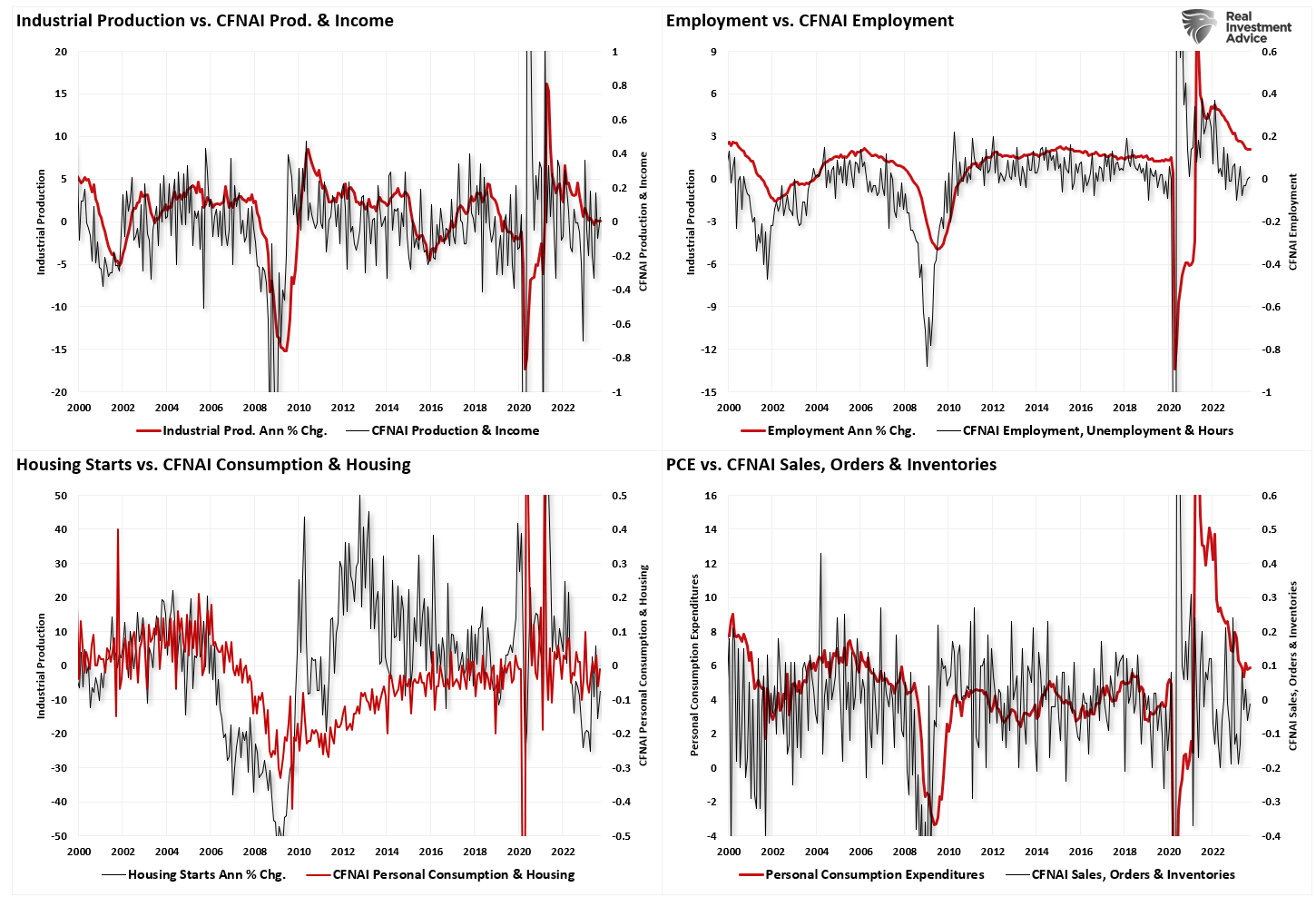

The overall index is broken down into four major sub-categories, which cover:

- Production & Income

- Employment, Unemployment & Hours

- Personal Consumption & Housing

- Sales, Orders & Inventories

To better grasp these four critical sub-components and their predictive capability, I have constructed a 4-panel chart. I have compared the CFNAI sub-components to the four most common economic reports of Industrial Production, Employment, Housing Starts, and Personal Consumption Expenditures. To provide a more comparative base to the construction of the CFNAI, I used an annual percentage change for these four components.

The correlation between the CFNAI sub-components and the underlying major economic reports is high. This is why, even though this indicator gets very little attention, it represents the broader economy. The CFNAI is not confirming the mainstream view of an “economic resurgence” that will drive earnings growth into next year.

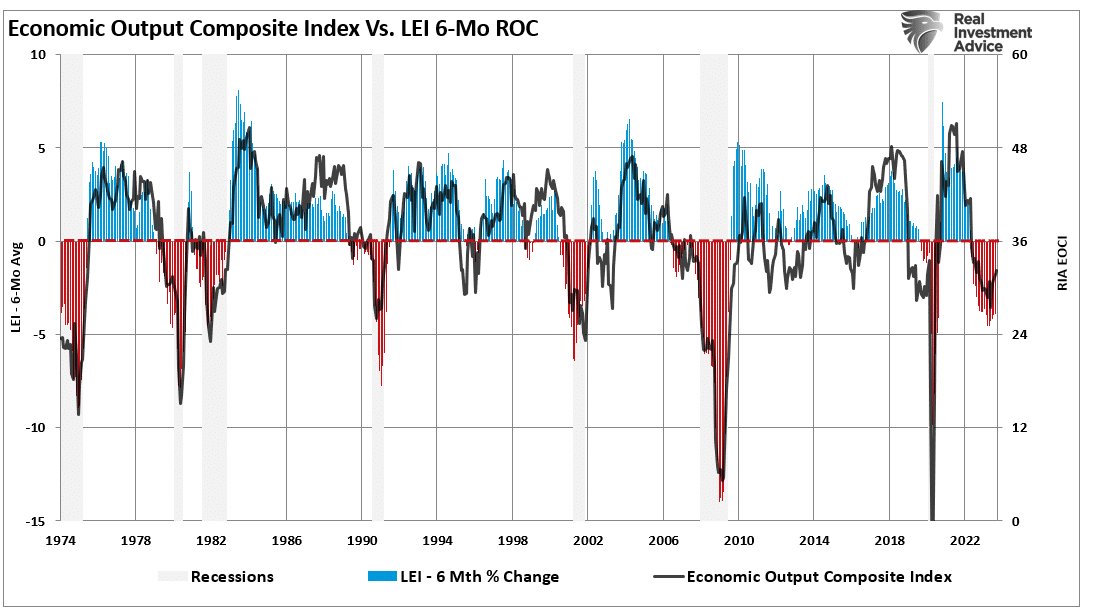

The CFNAI is also essential to our RIA Economic Output Composite Index (EOCI). The EOCI is an even broader composition of data points, including Federal Reserve regional activity indices, the Chicago PMI, ISM, the National Federation of Independent Business Surveys, and the Leading Economic Index. The EOCI further confirms that “hopes” of an immediate rebound in economic activity are unlikely. To wit:

“As discussed in “Signs, Signs, Everywhere Signs,” numerous measures suggest a recession is forthcoming. However, that recession has yet to reveal itself. Such has led to a fierce debate between the bulls and the bears. The bears contend that a recession is still coming, while the bulls are betting more heavily on a “no landing” scenario or, instead, avoiding a recession. Even the Federal Reserve is no longer expecting a recession.

But how is a “no recession” outcome possible amid the most aggressive rate hiking campaign in history, deeply inverted yield curves, and other measures warning of its inevitability?“

There are a couple of essential points to note in this very long-term chart.

- Economic contractions tend to reverse fairly frequently from high peaks, and those contractions tend to revert towards the 30-reading on the chart. Recessions are always present with sustained readings below the 30 level.

- The financial market is generally correct in price as weaker economic data weighs on market outlooks.

Currently, the EOCI index suggests more contraction will come in the coming months, which will likely weigh on asset prices as earnings estimates and outlooks are ratcheted down heading into 2024.

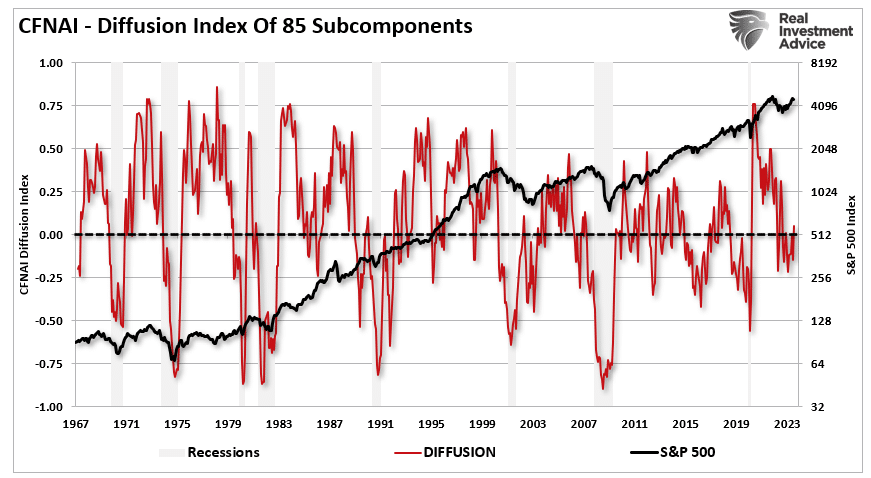

It’s In The Diffusion

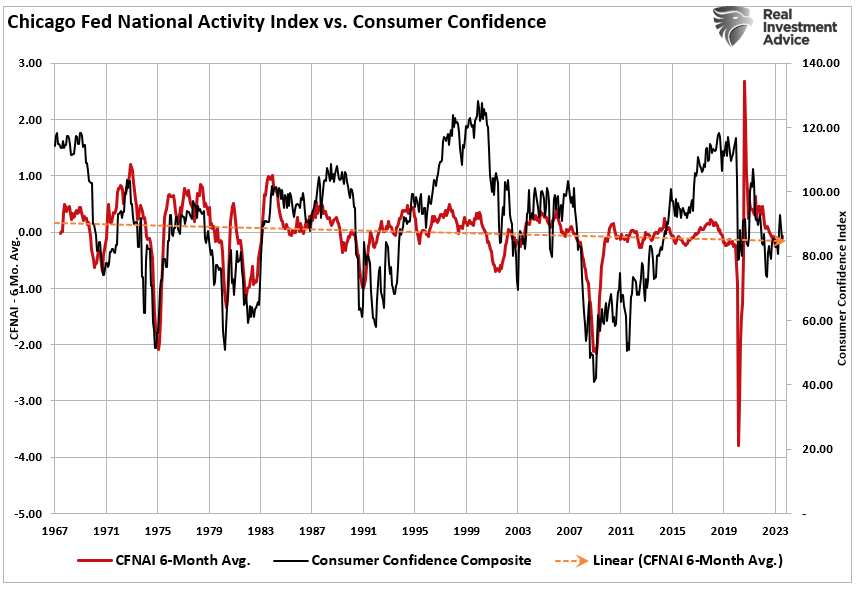

The Chicago Fed also provides a breakdown of the change in the underlying 85 components in a “diffusion” index. As opposed to just the index itself, the “diffusion” of the components gives us a better understanding of the broader changes inside the index itself.

There are two points of consideration:

- When the diffusion index dips below zero, it coincides with weak economic growth and outright recessions.

- The S&P 500 has a history of corrections and outright bear markets, corresponding with negative readings in the diffusion index.

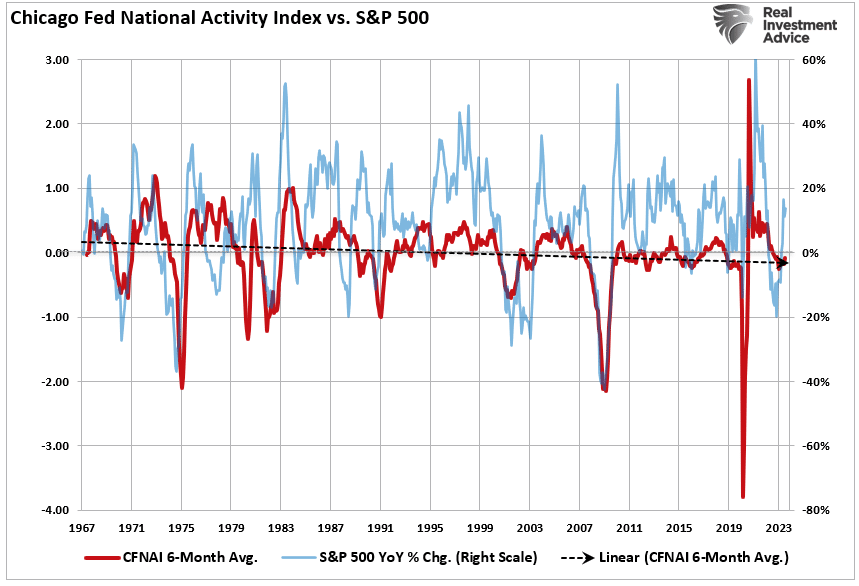

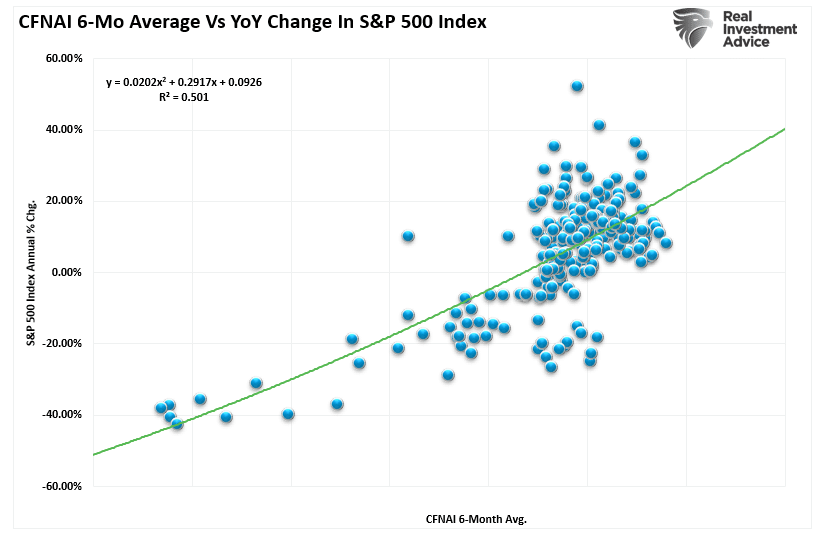

The second point should not be surprising, as the stock market reflects economic growth. Both the EOCI index above and the CFNAI below correlate to the annual rate of change in the S&P 500. Again, the correlation should not be surprising. (The monthly CFNAI data is very volatile, so we use a 6-month average to smooth the data.)

How good of a correlation is it? The r-squared is 50% between the annual rate of change for the S&P 500 and the 6-month average of the CFNAI index. More importantly, the CFNAI suggests the S&P 500 should be trading lower to correspond with the economic data. Throughout its history, the CFNAI tends to be right more often than market players.

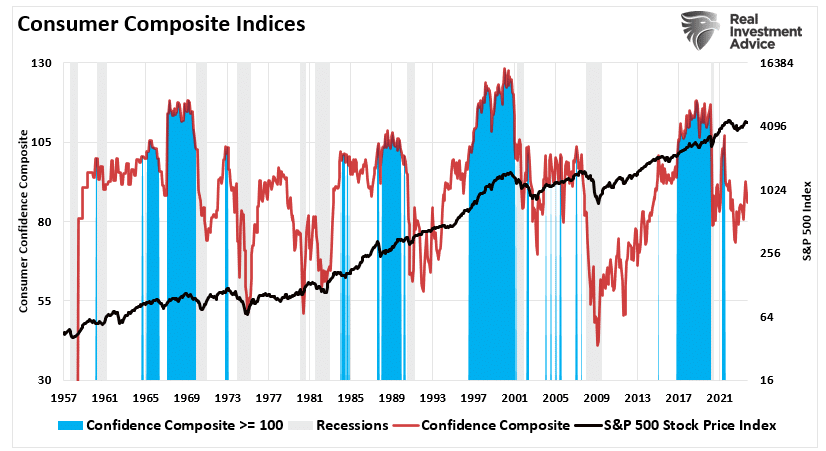

Investors should also be concerned about the current level of consumer confidence readings.

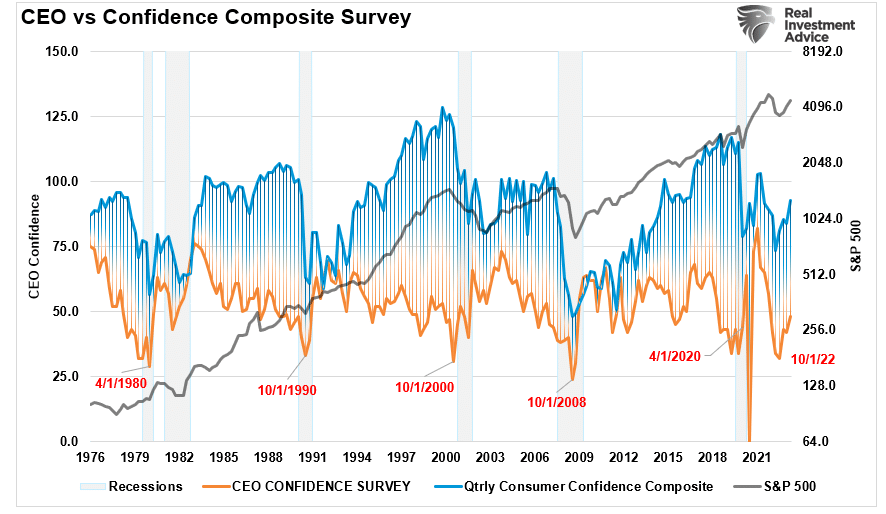

Not So Confident

The chart below is our consumer confidence composite index. It combines the University of Michigan and the Conference Board’s sentiment readings into one index. The shaded areas are when the composite index exceeds 100, corresponding with rising asset markets.

While that index has declined over the last 18 months, it remains elevated above previous recessionary levels, suggesting the economy continues to muddle along. The issue is the divergence between “consumer” confidence and “CEO’s.” The question is, who should we pay attention to?

“Is it the consumer cranking out work hours, raising a family, and trying to make ends meet? Or the CEO of a company that has the best view of the economic landscape. Sales, prices, managing inventory, dealing with collections, paying bills, tells them what they need to know about the actual economy?”

CEO confidence leads consumer confidence by a wide margin. Such lures bullish investors, and the media, into believing that CEO’s don’t know what they are doing. Unfortunately, consumer confidence tends to crash as it catches up with what CEO’s were already telling them.

What were CEO’s telling consumers that crushed their confidence?

“I’m sorry, we think you are great, but I have to let you go.”

Despite the recent uptick in CEO confidence since October, which corresponded with strong equity market performance, confidence is hovering around pre-recessionary levels. Notably, CEO confidence is not uncommon to tick higher just before the recession is announced.

The CFNAI also tells the same story: significant consumer confidence divergences eventually “catch down” to the underlying index.

This chart suggests that we will begin seeing weaker employment numbers and rising layoffs in the months ahead if history guides the future.

Conclusion

While the media hopes for a “no recession” scenario, the data tells us an important story.

Notably, the historical data of the CFNAI and its relationship to the stock market have included all Federal Reserve activity.

The CFNAI and EOCI incorporate the impact of monetary policy on the economy in both past and leading indicators. Such is why investors should hedge risk to some degree in portfolios, as the data still suggests weaker than anticipated economic growth. The current trend of the various economic data points on a broad scale is not showing indications of recovery but of a longer-than-expected recession and recovery.

Economically speaking, such weak levels of economic growth do not support more robust employment or higher wages. Instead, we should expect that 2024 could be a year where corporate earnings and profits disappoint investors as economic weakness continues.