Trending

The latest annual report from the Social Security Trustees showed the insecurity of social security.

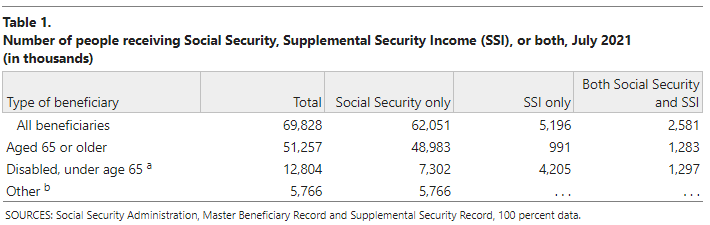

According to the July 2021 snapshot from the Social Security Administration, nearly 70-million people receive a monthly benefit check, of which 51.3 million are over the age of 65.

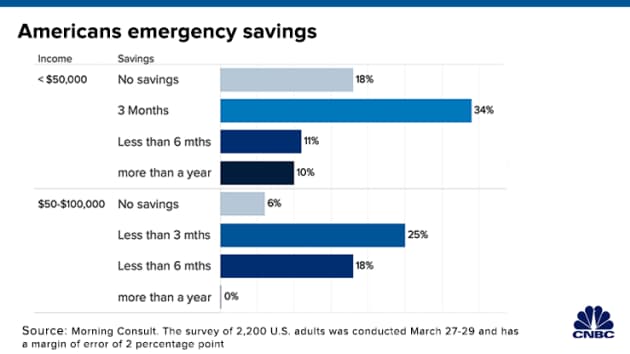

Social Security provides the majority of income to most elderly Americans. The system provides at least 50 percent of incomes for about half of seniors. For roughly 1 in 4 seniors, it provides at least 90 percent of total incomes. But, that dependency ratio is directly tied to the financial insolvency of the vast majority of Americans. According to a CNBC report:

“Morning Consult found that nearly 18% of adults with an annual income of $50,000 or less have no savings, while some 34% have enough to cover just three months of expenses. Another 11% would deplete savings within six months. Only 10% of that income group has more than a year’s worth of cash.

Higher-income households are only somewhat better prepared, the survey found. Among those with annual incomes of $50,000 to $100,000, about 18% said they have between three months and six months of savings. About 25% said their cash would last less than three months, and 6% had set aside nothing at all. None of those questioned in that income group had more than a year’s worth of savings.”

Such is a huge problem that will impact boomers in retirement.

The Insecurity Of Social Security

Given the financial insecurity of the bottom 90% of Americans, the dependency on social security is problematic. Here are some facts from the latest SSI report from CRFB:

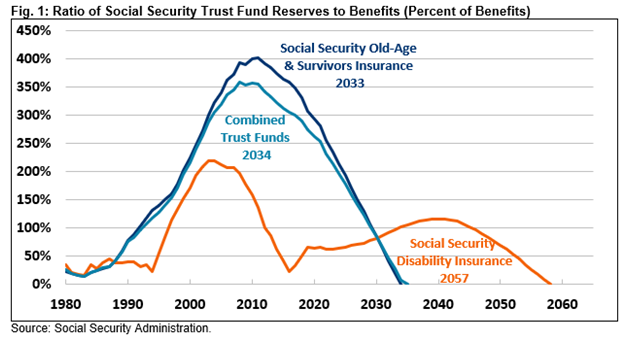

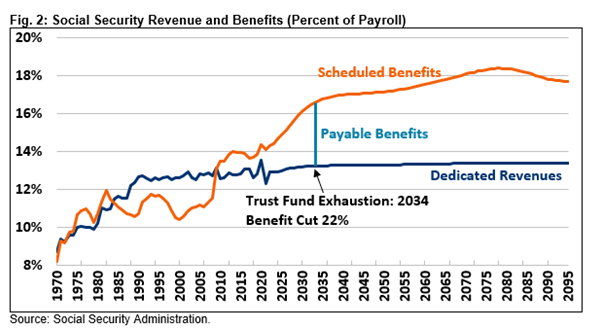

- Social Security is Only 13 Years from Insolvency. Social Security cannot guarantee full benefits to current retirees under current law. The Trustees project the Social Security Old-Age and Survivors Insurance (OASI) trust fund will deplete its reserves by 2033. The Social Security Disability Insurance (SSDI) trust fund will be insolvent by 2057. The theoretical combined trust funds will exhaust their reserves by 2034. Upon insolvency, all beneficiaries will face a 22% benefit cut.

Source: CRFB

- Social Security will run cash deficits of $2.4 trillion over the next decade. Such is the equivalent of 2.3% of taxable payroll or 0.8% of (GDP). Social Security’s 75-year actuarial imbalance totals 3.54% of taxable payroll. That is 1.2% of GDP or nearly $21 trillion in present value terms.

- Finances Are Deteriorating. Social Security’s finances worsened over the last year. Current projections show Insolvency occuring a year earlier, and the 75-year actuarial deficit is over 10 percent larger. The 75-year shortfall is nearly 85% larger than orginally estimated in 2010.

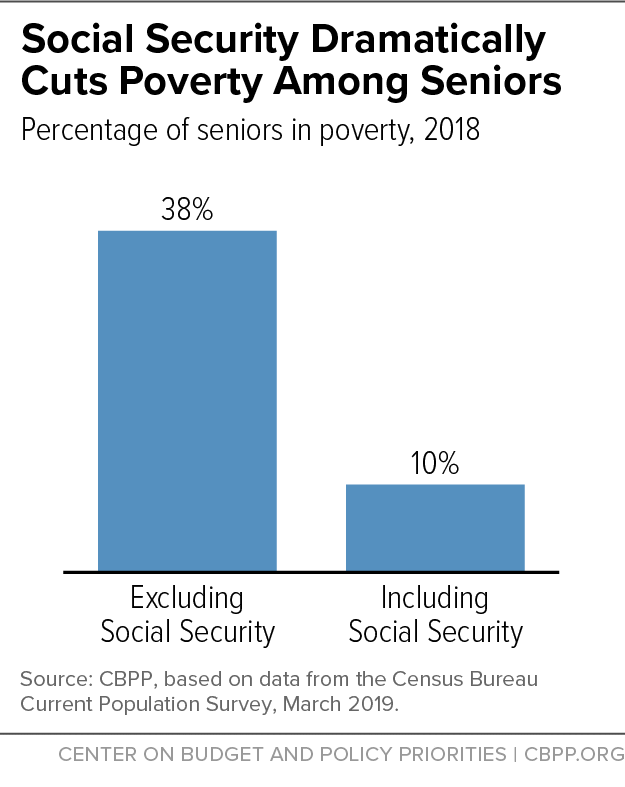

The problem is evident. Given the large and growing dependency on social security, benefits will get cut for recipients if Congress fails to act. As noted by the Center Of Budget & Policy, social security for many retirees is the difference between living in poverty or not.

Demographics Are Destiny

One of the primary contributors to the insecurity of social security is demographics.

In 1940, the life expectancy of a 65-year-old was just 14 years. Today it is over 20 years. By 2035, the number of Americans 65 and older will increase from approximately 56 million today to over 78 million.

The problem for social security is that in 1940, nearly 16-workers paid into the program for each person receiving benefits. Currently, that ratio is just 2.8 workers for each Social Security beneficiary. By 2035, that ratio will decrease to 2.3 covered workers for each beneficiary.

“Social Security will see negative cash flow of $147 billion this year. The deficits will keep adding up as the population ages as fewer workers pay into the system relative to the number of retirees collecting benefits.” – Reason

Such increases in the number of retirees and lower birth rates decrease the relative number of workers. However, this decline in the “support ratio” is not just domestic, but global.

“Recently released official U.S. birth data for 2020 showed births fell continuously for more than a decade. The ‘total fertility rate,’ is a measure constructed from the data to estimate the average total number of children born. That rate fell from 2.12 in 2007 to 1.64 in 2020. It is now well below 2.1, the value considered to be ‘replacement fertility,’ which is the rate needed for the population to replace itself without immigration.“

However, the problem isn’t just the “replacement rate” of workers paying into the system. But also the structural change to the workforce itself.

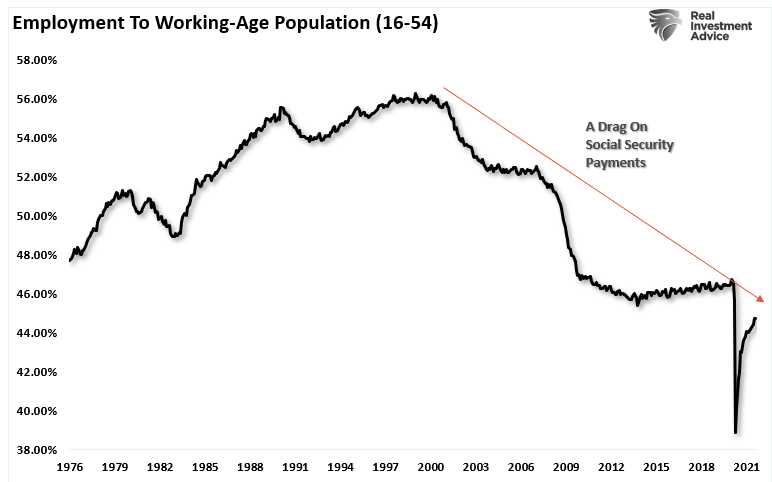

A Structural Employment Problem

The structural shift in employment is due to technology and automation. Yet, it is an overarching problem most give little attention to.

While the mainstream media focuses their attention on the daily distribution of economic data points, there is a hidden depression running along the country’s underbelly. While reported unemployment is heading back to historically lower levels, there is a swelling mass of uncounted individuals. These are individuals assumed to have either given up looking for work or are working multiple part-time jobs.

The chart strips out the argument of retiring baby boomers, who ironically, aren’t retiring. Such is not because they don’t want to retire, but because they can’t afford to.

These higher levels of under and unemployment apply downward pressure on wages even as work hours increase. Real wage declines are evident as companies opt for increasing productivity, continued outsourcing, and streamlining employment to protect corporate profit margins. However, as the cost of living is affected by the rising food, energy, and health care prices without a compensatory increase in incomes, more families are forced to turn to assistance to survive.

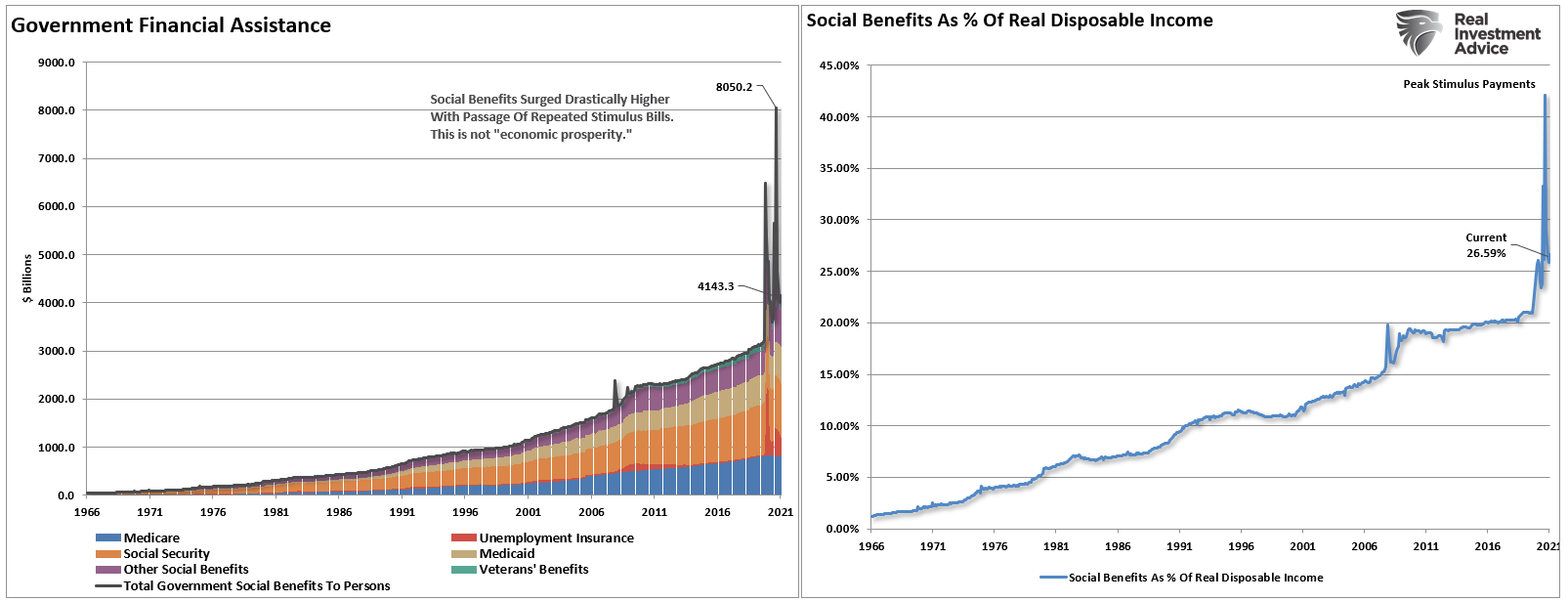

Without government largesse, many individuals would live on the street. The chart above shows all the government “welfare” programs and current levels to date. The black line represents the sum of the underlying sub-components. Thus, while unemployment insurance did taper off after its sharp rise post-pandemic, social security, Medicaid, Veterans’ benefits, and other social benefits continue to rise.

Importantly, these social benefits are critical to the average person’s survival as they make up more than 25% of real disposable personal incomes.

With 1/4 of incomes dependent on government transfers, it is not surprising the economy continues to struggle. Recycled tax dollars used for consumption purposes have virtually no impact on the overall economy.

The Social Security Insecurity Endgame

As stated above, the biggest problem for Social Security, and the U.S. in general, comes when Social Security begins paying out more in benefits than it receives in taxes. Then, as the cash surplus gets depleted, Social Security can not pay full benefits from its tax revenues alone.

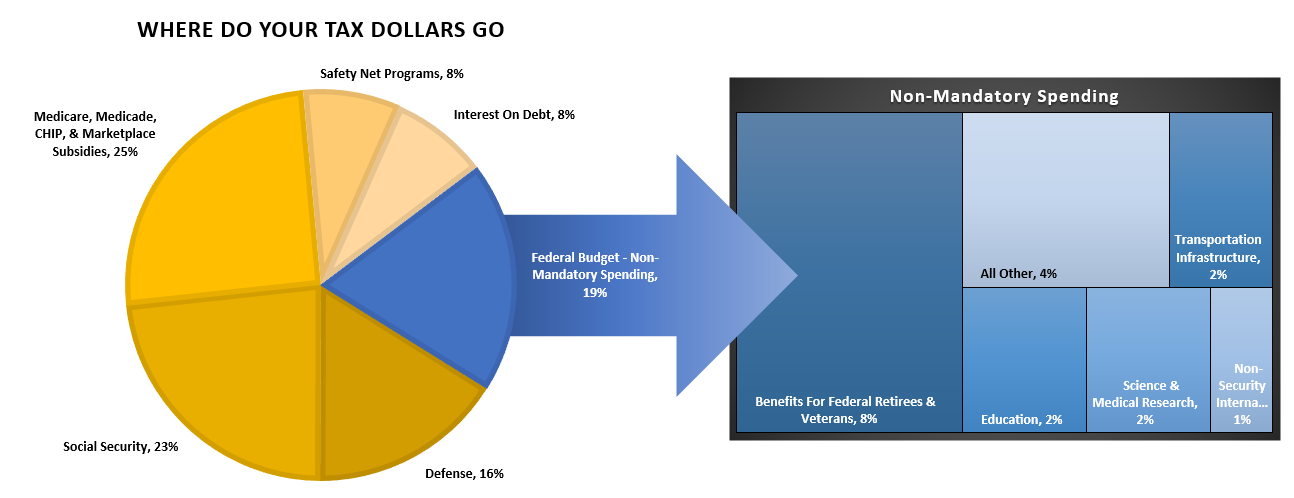

Already, welfare programs in the U.S. are consuming ever-growing amounts of general revenue dollars to meet obligations.As noted recently,mandatory spending already consumes more than 100% of Federal tax revenues.

“In the fiscal year 2019, the Federal Government spent $4.4 trillion, amounting to 21 percent of the nation’s gross domestic product (GDP). Of that $4.4 trillion, federal revenues financed only $3.5 trillion. The remaining $984 billion came from debt issuance. As the chart below shows, three major areas of spending make up most of the budget.”

Think about that for a minute. In 2019, 75% of all expenditures went to social welfare and interest on the debt. Those payments required $3.3 Trillion of the $3.5 Trillion (or 95%) of the total revenue collected. Given the decline in economic activity during 2020, those numbers become markedly worse. For the first time in U.S. history, the Federal Government will have to issue debt to cover the mandatory spending.“

Eventually, either the benefits will get slashed, or the rest of the government will have to shrink to accommodate the “welfare state.” It is improbable the latter will happen.

Conclusion

Demographic trends are reasonably easy to forecast and predict. Each year from now until 2035, we will see successive rounds of boomers reach the 62-year-old threshold. Two problems are resulting from these consecutive crops of boomers heading into retirement.

The first is that each boomer has not produced enough children to replace themselves, which leads to a decline in the number of taxpaying workers. It takes about 25 years to grow a new taxpayer. We can estimate, with surprising accuracy, how many people born in a particular year will retire. The retirees of 2070 were born in 2003, and we can see and count them today.

The second problem is the employment problem. The decline in economic prosperity is the result of four decades of misguided policy:

- Increases in non-productive debt and deficits,

- Reduction in savings,

- Declining income growth due to productivity increases; and,

- The shift from a manufacturing to service based society that generates lower levels of taxable incomes in the future.

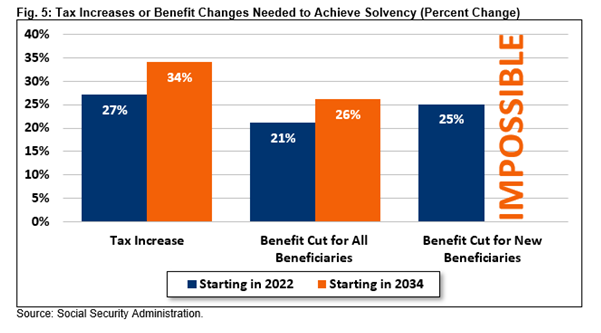

“The more time that passes, the heavier the lift will be. According to an analysis from the Committee for a Responsible Federal Budget, which advocates for low deficits and sustainable entitlement programs, delaying action until insolvency hits in 2034 will make the needed tax increases or benefit reductions about 25 percent larger than if Congress acted today. In either case, the changes will be seriously disruptive to Americans’ retirement plans and financial security.” – Reason

The entire social support framework faces an inevitable conclusion where no wishful thinking will change that outcome. The question is whether our elected leaders will start making the changes necessary sooner, while they can get done by choice or later when forced upon us.