Written by: Steve Majoris | Advisor Asset Management

Through the first half of 2021, fixed-income investors have been faced with their greatest fear: inflation. This evolving phenomenon has led to higher interest rates, sparking volatility in fixed-income markets. 2021 has seen U.S. Treasuries off to one of their worst starts in years as the Bloomberg Barclays U.S. Treasury Index was down 4.25% through Q1 (the first quarter), with the Long Bond portion down a whopping 13.51%. This type of volatility has left most bondholders scratching their heads and wondering how their portfolio could fare in an inflationary environment. Investors and economists likely would agree that a steady increase in prices over time is normal and healthy for a consumer-based economy, but too much of it in a short timeframe could cause serious volatility. The main fear is that in order to counter inflation and keep it from running too hot, the Federal Reserve would have to raise the federal funds rate, which could ultimately put pressure on financial markets.

Bonds typically underperform when interest rates trend higher and we have seen this come to fruition this year. As the economy recovers from the pandemic-induced shutdown, a little inflation was certainly expected; however, recently passed fiscal stimulus, record-setting deficits, unprecedented accommodative monetary policy and supply chain disruptions are all adding up into a nice stiff inflation cocktail that’s stronger than what the market expected. Despite seeing some of the highest inflation upticks in over 10 years, the Federal Reserve holds the position that these changes will be temporary.

This begs the question, is this spike in inflation transitory or non-transitory?

Source: Bloomberg

Source: Bloomberg

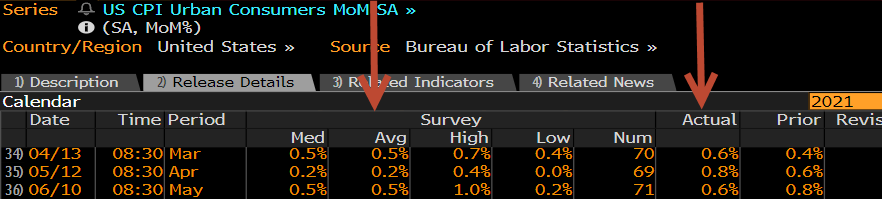

The latest Consumer Price Index (CPI) reading from the Bureau of Labor Statistics – the headline measure used to track inflation – on June 10 came in at 0.6% for the May release. This is the third month in a row in which the number has come in above expectations and pushes CPI year-over-year to 5.0% – the biggest increase since August 2008. The bond market’s reaction was certainly interesting and perhaps confusing to some. The numbers showed inflation above expectations but yields trended lower across the curve over the course of the trading day. Since CPI is a lagging indicator, the market could be attempting to get ahead of future trends and may still be debating whether recent consumer price spikes could be short lived.

Interest rates appear to have somewhat stabilized after a volatile Q1 and perhaps bets that inflation could cool down quicker than previously anticipated are being placed. When taking a deeper dive into what is driving broad consumer prices higher, it is understandable to think that the transitory side of the argument may appear to hold water.

Source: Bloomberg

There have been several disruptions in normal business activity since the pandemic and although the broad economy has experienced a speedy recovery, some sectors are still experiencing issues. One that has made major headlines is the global chip shortage affecting consumer-based products ranging from toaster ovens to automobiles. The chip shortage and its effect on automobiles appears to have translated into higher costs to the consumer. According to CNBC, the shortage is expected to cost the global auto industry $110 billion in revenue in 2021. Demand for both new and used cars has spiked this year and there is simply not enough supply to meet the demand, which is starting to factor into prices. The lack of new vehicles has led to a significant spike in used car and truck prices with May showing a 7.3% increase.

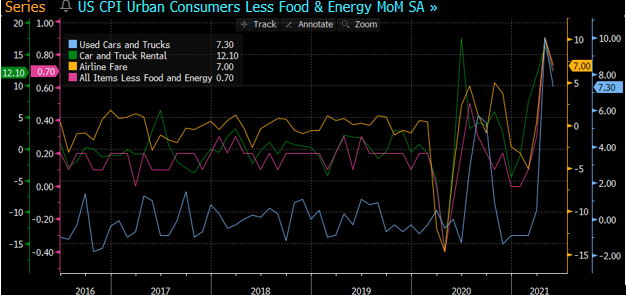

The CPI Ex Food and Energy is another measure commonly used for tracking inflation as it removes volatile components such as oil. A recent print came in at 0.7% vs. 0.5% estimate for the month of May and to get a better idea of what’s moving the number, it can be broken down into two segments: commodities and services. The commodities portion was 1.80% while services rose 0.4% and it looks as though both had their largest increases due to a spike in transportation-related costs. On the services side, one theme as of late has been the return to air travel which explains both the uptick in vehicle rentals and airline fares, up 12.10% and 7% respectively.

Source: Bloomberg

Daily passenger numbers tracked by the TSA continue to recover toward pre-pandemic norms with 2.09 million travelers reported on June 14, the highest since March 2020. It appears the latest month-over-month change in CPI is in large part due to the demand for plane tickets and a supply disruption affecting automobiles which would further support the transitory argument. That said, is this the case for the year-over-year inflation number that was above expectations as well?

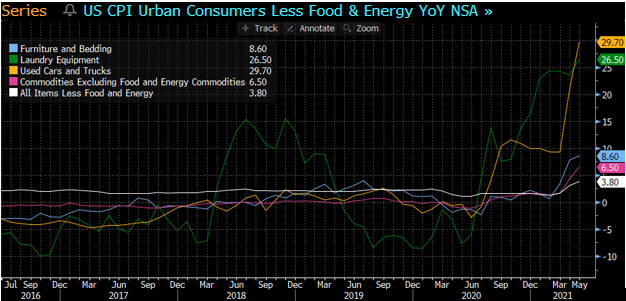

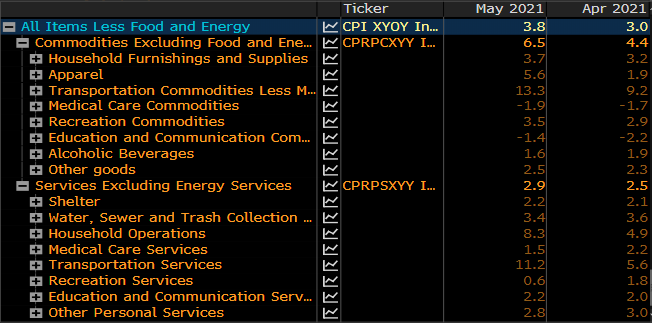

CPI year-over-year (YoY) numbers came in at 5% versus 4.7% estimate and CPI Ex Food and Energy YoY – perhaps the better indicator to measure inflation because it removes the 28.5% increase in Energy – came in at 3.8% versus 3.5% estimate. The lumber shortage we’ve all heard about, as well as the lack of chips, are both leading to higher consumer prices over the past year. Commodity products experienced the biggest jump at 6.5% while services came in at 2.9%. Along with used vehicles, products like laundry equipment (affected by the chip shortage) and furniture (affected by the lumber shortage) both saw a significant increase at 26.5% and 8.6% respectively.

Source: Bloomberg

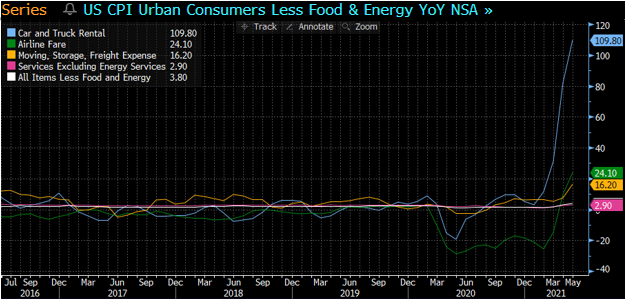

In the services sectors, we’ve all heard our own anecdotal stories about folks moving as a result of the pandemic and expenses related to moving, which saw one of their sharpest upticks in years at 16.20% for moving, storage and freight expenses. Airfares rose 24.10% and car rentals spiked 109.80% for YoY changes. As supply chain disruptions are addressed and the travel and relocation trends begin to normalize, perhaps it is fair to say that we have seen the largest spike in broad consumer prices and that there is a good chance they stabilize going forward?

Source: Bloomberg

While the largest upticks have been mentioned above, there are a few categories and businesses that have yet to recover from the pandemic and may soon result in higher prices as we get closer to a fully re-opened economy. The chart below shows how the many different categories of CPI Ex Food and Energy are broken down by the Bureau of Labor Statistics. Medical Care Commodities such as healthcare equipment and supplies, which experienced a -1.9% decrease in prices over the past year, could see a rebound as hospitals become less overwhelmed with COVID-19 patients and begin performing more elective surgeries again. Education and Communication Commodities, like computer software and accessories, might reverse its downward trend with prices as schools and offices reopen and get back to full capacity. Recreation services pricing, which partially consists of movie theater tickets and sporting events, could see an uptick as well as we reopen and return to normal. If the current unemployment rate of 5.80% continues to recover from pandemic highs and more people return to work, this could lead to more broad business activity and overall higher prices as well. It may be that these factors support the notion that we still have a way to go before reaching peak inflation. Even the Federal Reserve in their most recent minutes on June 16 admitted some of these forces could persist.

Source: Bloomberg

Only time will tell how long these above-average inflation trends could continue; but in a time like this, we believe fixed-income investors worried about inflation should remember:

- Know your risks

- Know what you own

- Understand how different market scenarios could impact your portfolio

If inflation continues to trend higher, higher duration and interest-rate-sensitive assets such as longer-dated Treasuries, have the potential to remain underperformers versus the broad bond market. Investing in shorter duration and less interest-rate-sensitive assets is one of the primary ways to try to limit volatility during periods of inflation and rising rates. Another potential way to hedge is a slight move lower in credit quality to try to benefit more from a cyclical economic recovery as lower investment grade has outperformed typical AAA and higher quality bonds so far in 2021. Finally, a laddered structure within bond portfolios that provides frequently recurring maturities and ample liquidity, have the potential to give investors opportunities to take advantage of rising rates and capture elevated yields when available. If a bond investor knows their short duration positioning could reduce portfolio volatility and that they have maturities coming due on a recurring basis, it might have the potential to aid in alleviating some of the inflation-induced concerns facing market constituents today.

Transitory or not, these different strategies have the potential to be used to help fixed-income investors overcome the bond market’s greatest fear: inflation.