Trending

Written by: James T. Tierney, Jr. and Michael Mathay, CFA

When Tesla delivered disappointing news on vehicle deliveries on April 2, it jeopardized its status in the so-called Magnificent Seven stocks. Whether or not it maintains its spot among the top US mega-caps, we think the news reflects a speedbump for equity investors seeking to access the disruptive potential of electric vehicles.

Tesla has been at the vanguard of electric vehicle (EV) production for 15 years. The company launched its first EV model in 2008, and its brand became a household name globally. Competitors were slow to react, and at first, few could match Tesla’s quality or features.

EV Market Dynamics Are Shifting

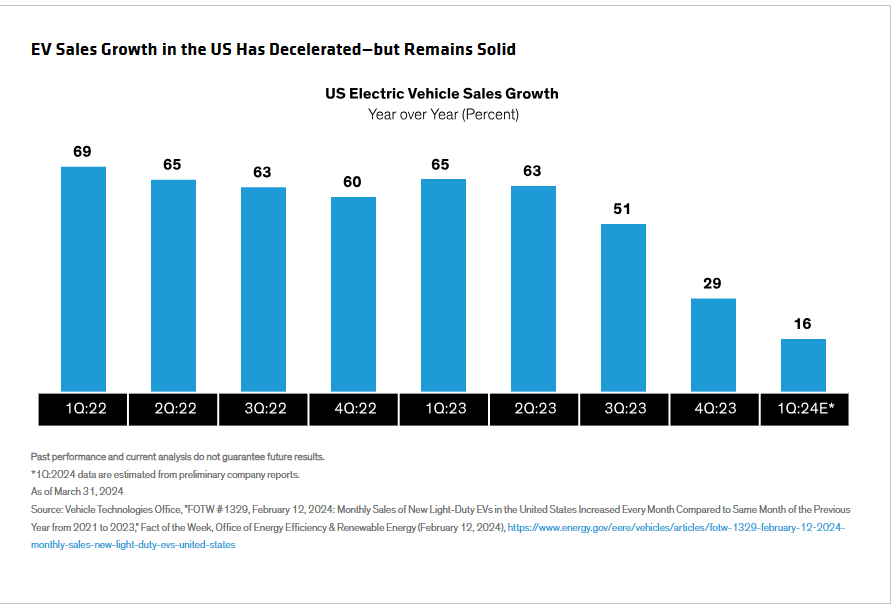

In recent years, the market has changed. By S&P’s count, 48 EV models are now sold in the US versus just six in 2019.1 Quality has been improving. And at the same time, the pool of early EV enthusiasts is drying up. This dynamic is most clearly seen in the US, where growth in the number of EVs sold has decelerated sharply (Display) versus expectations of continued robust growth. The industry is still growing, but more slowly, with far greater competitive pressures.

Of course, EVs are still important for efforts to help the transition toward renewable energy sources. For many prospective buyers, EVs are an excellent option for local transportation. However, buyer anxiety around vehicle range and charging infrastructure remains a deterrent.

Technology will solve these problems over time. Improvements in battery materials and other key technologies will ultimately extend the range of EVs. With more charging infrastructure and quicker cycle times, the charging experience will become more like filling up your gas tank today. But we aren’t there yet. So, what does this mean for the industry?

Mounting Competition to Press EV Profitability

For some auto manufacturers, we believe a more competitive EV industry is likely to lead to lower profitability, or in some cases, prolonged losses. In our view, equity investors must be very selective in holding shares of automakers whose earnings growth is predicated on winning more EV market share.

That said, we don’t think this speedbump will undermine the long-term potential of the EV market. For equity investors, we believe the key to capturing the EV opportunity is via technology enablers to the industry, also known as pick-and-shovel providers.

Charging and Range: Overcoming Barriers to EV Adoption

Consider the charging infrastructure. EV drivers need more chargers—and confidence in their functionality. Eaton is an electrical equipment manufacturer that we believe is poised to play an instrumental role in providing equipment to expand the US charging infrastructure. Since the US government has allocated significant spending on EV charging via the Inflation Reduction Act, this segment of the industry should enjoy solid structural support in the coming years, in our view.

What about range anxiety? Possible solutions include battery materials, hybrids, new technologies and improvements on existing systems. Aptiv, an Irish-American auto technology group, will likely be a key supplier for many of these upgrades, in our view. EVs contain as much as three times this type of content, compared with internal combustion engines; hybrid vehicles have about twice as much. Meanwhile, the increasing intelligence of automotive systems should support demand for all sorts of electronic equipment. Amphenol, which manufactures sensors and connectors for automotive products and for many other industries, is likely to see rising demand.

Don’t Mistake Competition for a Lack of Demand

Outside the US, the EV story is changing in a different way, particularly in China. EVs accounted for 8.1% of US vehicle sales in the fourth quarter of 2023, according to BloombergNEF. In contrast, EV sales reached nearly 80% of the total in Norway, 35% in the Netherlands, 24% in China, 20% in Germany and 18% in the UK.

These numbers tell us that consumers are adopting EVs even as competition reshapes the market. BYD of China has now surpassed Tesla as the world’s largest EV manufacturer by volume, according to company reports. And dozens of other smaller Chinese EV manufacturers are scrambling to grab market share. At this stage of the market’s development, we think it’s very difficult to identify which EV vehicle manufacturers will rise to the top—especially since it’s hard to predict which of the new entrants will successfully penetrate markets in Europe, Latin America and North America.

While EVs span a range of price points and features, they all have something in common: many of the electrical component needed are similar. As a result, we believe the pick-and-shovel providers are better positioned to offer earnings growth from EVs than global automakers.

Enthusiasm for new technology—from AI to EVs—often creates excitement for equity investors. Yet accessing equity opportunities in evolving industries requires a sober eye on the industry dynamics and business quality that will determine long-term earnings power.

1. S&P Global Auto Outlook, March 2024

Related: Fixed-Income Outlook: Seeing the Forest Beyond the Trees