Trending

It is said that the name “Led Zeppelin” was coined by Keith Moon when Jimmy Page proposed starting a band together after the “Beck’s Bolero” session.[i] Keith is said to have replied, “it won’t just go down like a lead balloon, it will be a lead zeppelin.” Moon kept his role in the The Who, but Page. The tie-in to today’s market is that I’m afraid that no one told the President that to tariff implementation would go over similarly with investors.

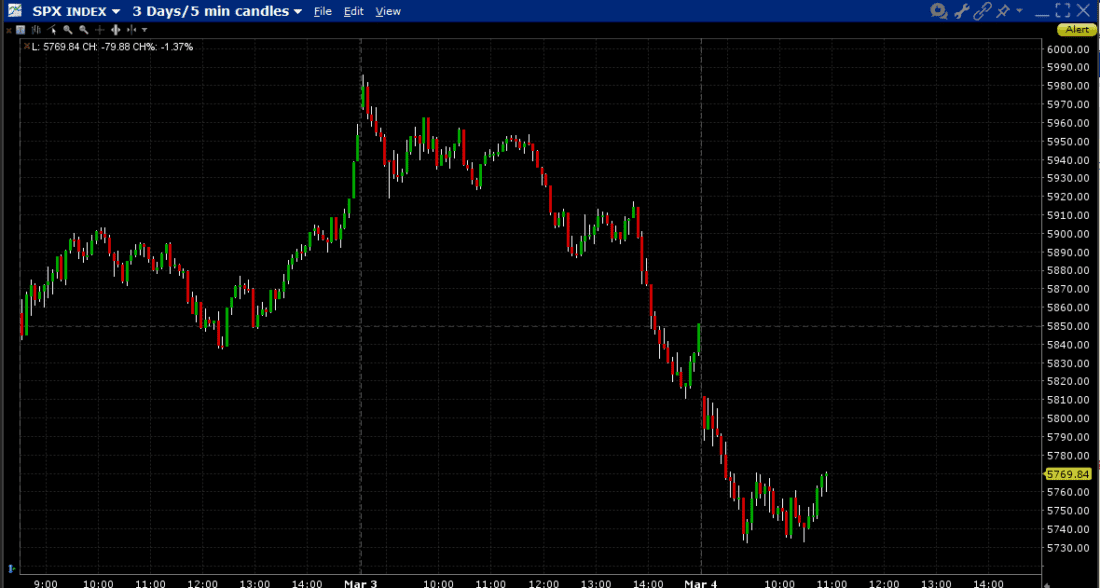

Trading has gotten ugly quickly. The first leg of the decline should not have been unexpected, considering that we had an epic end-of-month markup just before Friday’s close. The early declines were simply the market giving back those suspicious late gains from the prior session. But there was no way around the tariff promise at the end of President Trump’s media event for TSMC, which occurred at about 2:42 ET.

SPX Index, 3-Days, 5-Minute Candles

Source: Interactive Brokers

Considering the near misses that accompanied prior tariff threats regarding Mexico, Canada and others, the market had been in a bit of wait-and-see mode about tariffs – not willing to react too much until they seemed imminent. There was some hope that a reprieve might have been announced at tonight’s joint session of Congress, but it was unequivocal that tariff implementation would indeed occur before the speech.

As a result, we’ve given back nearly all of the post-election rally. For reference, SPX closed at 5782.76 on Election Day, with a gap to 5864.89 on the next day’s open. As I type this, we’re below the lowest level of November 5th, and have closed the gap between the Election Day close and the next day’s open (that said, the gap was already closed on Jan 13th). The open question is whether today’s move is capitulation or confirmation of a medium-term top. Considering that today is shaping up to be an outside reversal – higher intraday high today accompanied by a close below Friday’s low, the market has some work to do if a bounce is in order.

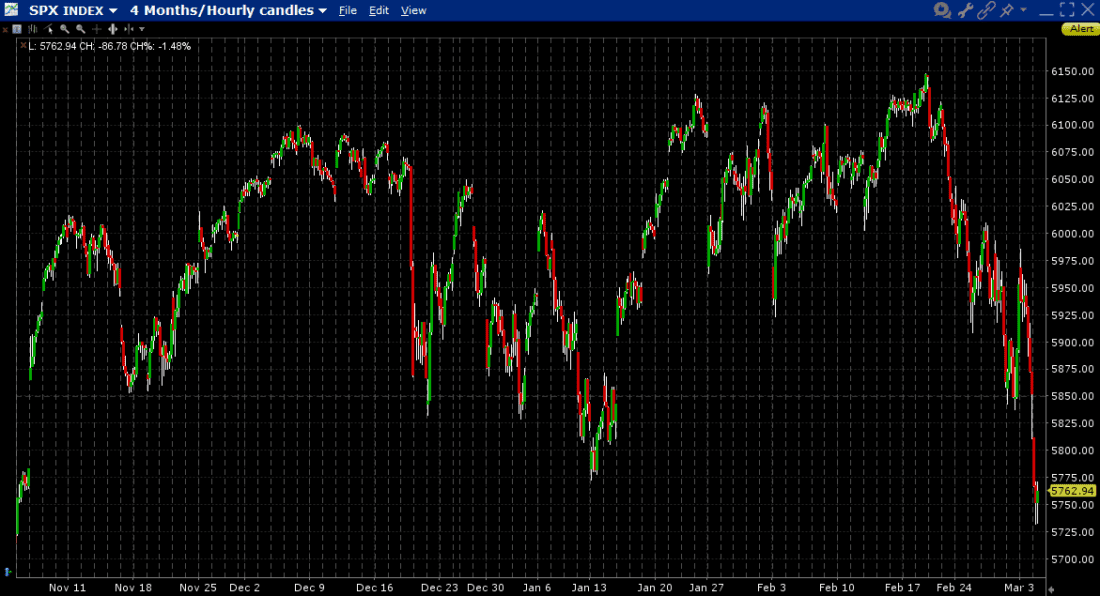

SPX Index, 4-Months, 1-Hour Candles

Source: Interactive Brokers

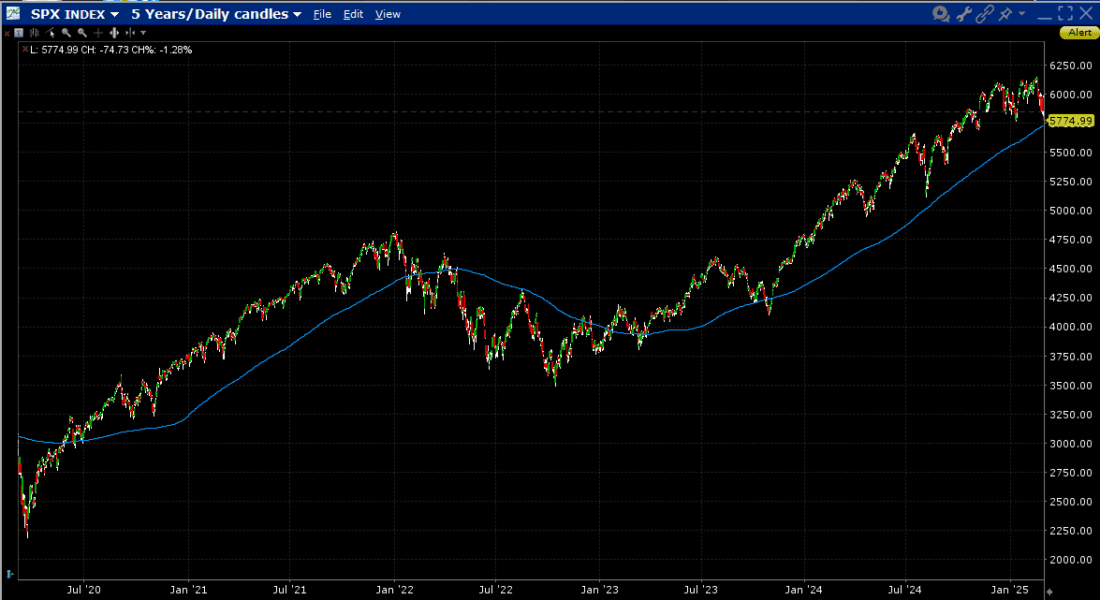

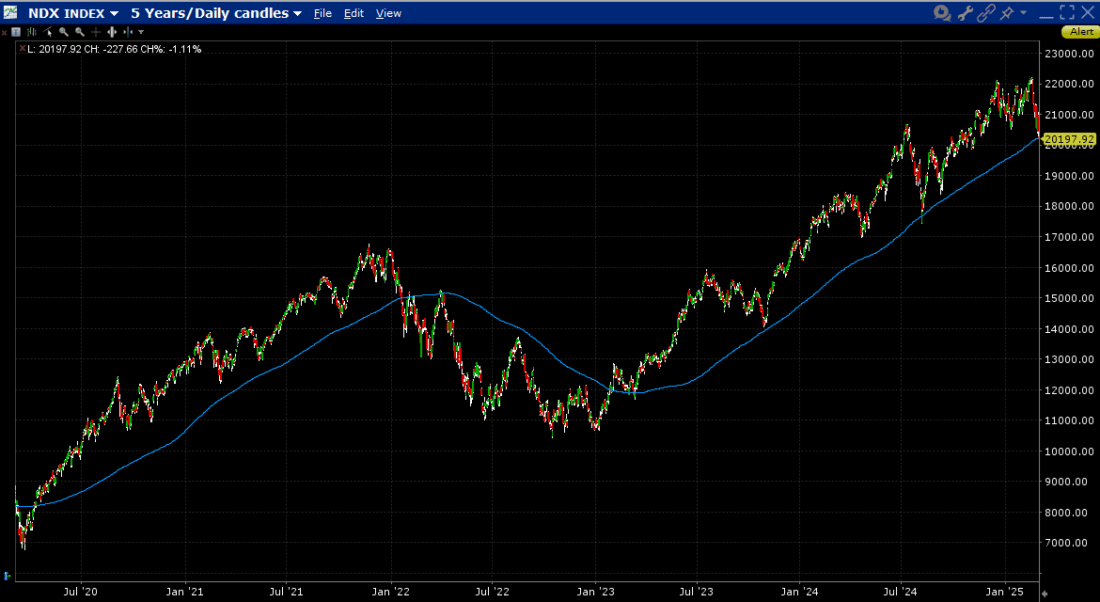

That said, could a bounce be in order? Certainly. Both the S&P 500 (SPX) and Nasdaq 100 (NDX) indices tested their 200-day moving averages successfully this morning, and one could certainly posit that a bounce is in order after such sharp recent selloffs. We can see from the charts below that while both indices might have briefly breached their 200-day averages during the past two years, that long-term trend has held. It reasonable for risk-tolerant traders to take a shot at finding a tradeable bottom around these levels. As I type this, the bounce seems to be occurring. Whether it sticks has much to do with overall risk tolerance and exogenous events.

SPX Index, 5-Years, Daily Candles

Source: Interactive Brokers

NDX Index, 5-Years, Daily Candles

Source: Interactive Brokers

It is important to remember that intraday moves can be exacerbated during periods of higher volatility because liquidity can become constrained. I believe that I’ve discussed[ii] the sign that used to hang above my desk when we were active options market makers:

- Raise vols

- Widen spreads

- Shrink sizes

These were the standard defensive moves that we undertook when markets got hectic. The logic:

- When there is high demand for anything, one should expect prices to rise. The same applies for volatility protection. The marketplace was eager to buy volatility, so this reflects normal supply and demand.

- This reflects both uncertainty and supply/demand. Wider spreads mean that buyers will need to pay a greater premium to buy, and this also protects the market maker against if the mood changes

- The amount of capital that one is willing to risk should change with market conditions. The riskier the market environment, the smaller the desired commitment.

It should be clear that the latter two diminish market liquidity. While I can’t be 100% certain that current market-makers utilize that rubric, I’d be shocked if they didn’t do something similar. It’s a basic form of both self-preservation and profit maximization. It also means that relatively modest amounts of buying and selling can move prices substantially when buyers and sellers are sufficiently motivated.

My advice under those circumstances is to think like a market maker. Lower your risk tolerance, raise your price targets, and get paid to provide liquidity by using limit orders inside the wider markets instead of chasing stocks and options. I’m not sure that everyone will take this to heart in this FOMO-driven environment. We’ve seen not only a willingness to buy dips, which can be done using that suggested tactic, but also a desire to chase rallies. That might work, but realize that rather than exploiting market inefficiency, you’re facilitating it. If you chase, you make more money for whomever is on the other side of the trade. Is that what you really want to be doing right now?

Related: The End of Easy Gains? Why Buying Dips Isn’t Working

[i] Listen for “Moon the Loon’s” scream at the 1:32 mark that introduces Zep’s future sound and perhaps the onset of all heavy rock.

[ii] I can’t find the link where I explained this topic.