Trending

A recent warning by YahooFinance warns investors to sell their cash and buy bonds and stocks now as the Fed pauses. To wit:

“Get out of cash now. Take advantage of some of these incredible things in the fixed-income markets, especially in the belly of the curve. Take advantage of the companies that are still available to you at reasonable prices,” said Gargi Chaudhuri, head of investment strategy at BlackRock iShares Americas.

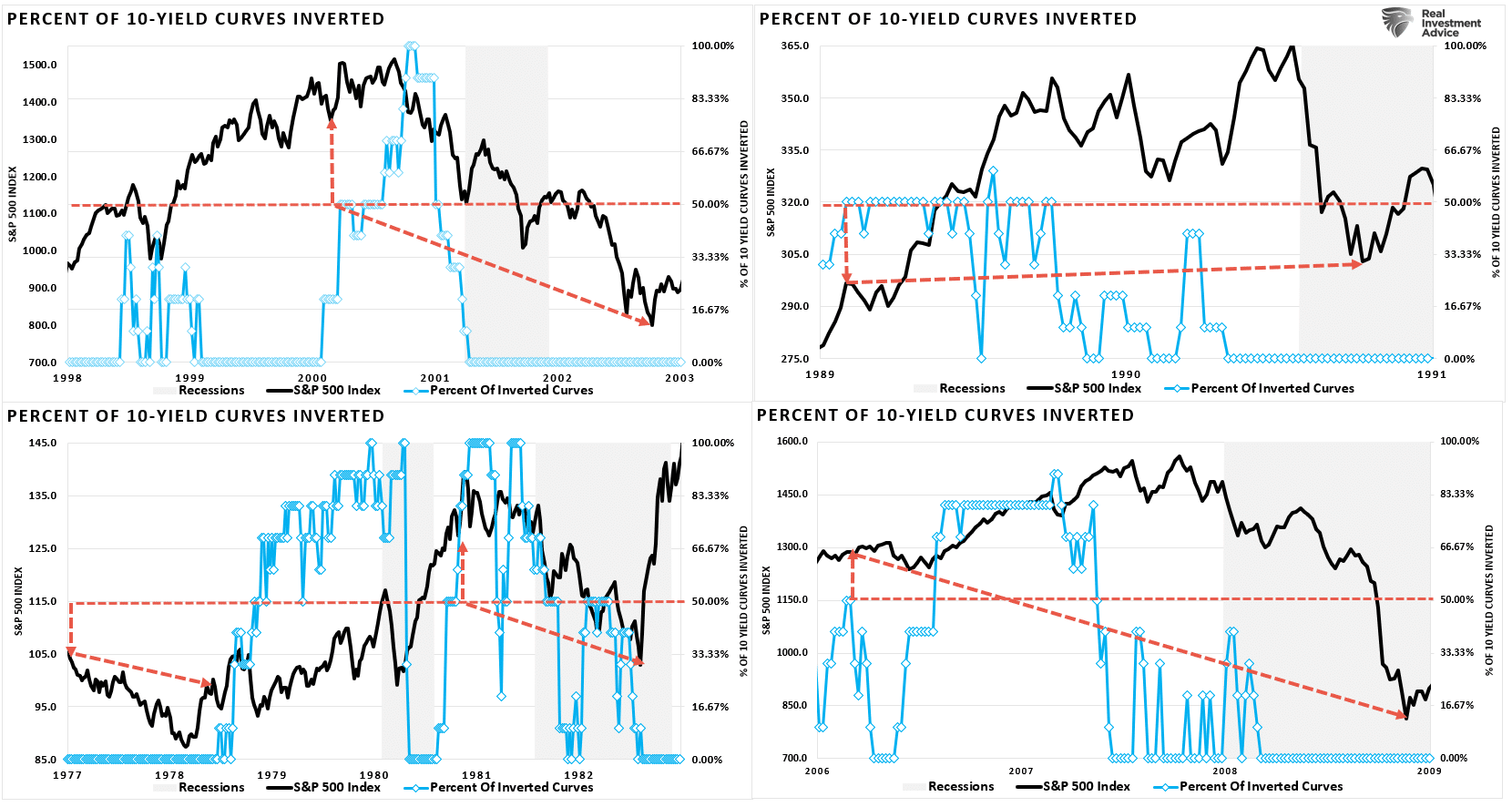

Such advice certainly goes against a mountain of historical evidence from both inverted yield curves and Fed rate cuts that suggest investors should be selling stocks and heading to the safety of cash. For example, the four-panel chart below shows the previous yield curve inversions when more than 50% of the ten economically sensitive yield spreads we track were inverted. (Read this for a complete history.)

The red lines denote where 50% of the yield curves became inverted and how investors fared during the un-inversion process. In every case, investors were better off in cash, except for 1990, when it was virtually breakeven.

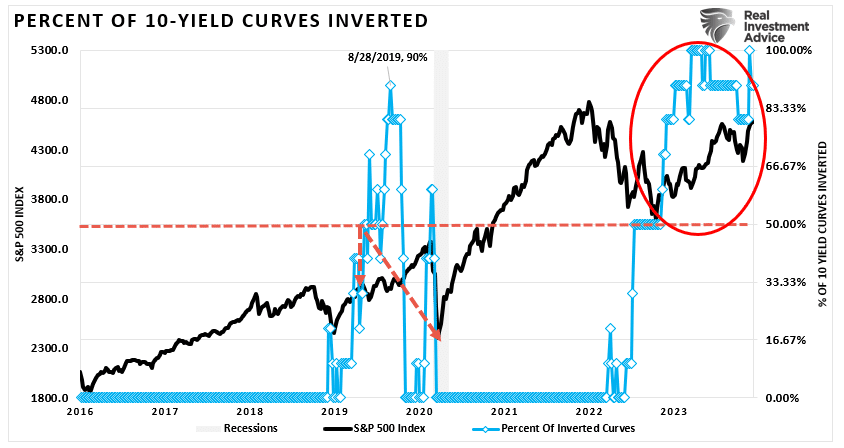

In recent years, investors prospered by selling stocks and going to cash in early 2019, avoiding the eventual market downturn and recession in 2020. While it seems as if the “yield curve” is broken, and investors should “get out of cash,” the yield curve has yet to UN-invert, which is where economic recessions become visible.

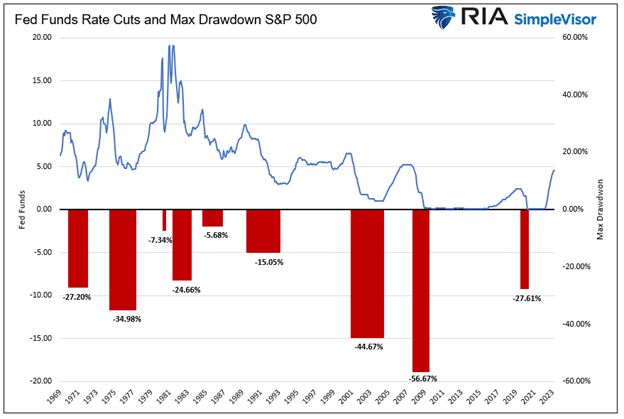

As noted, another historical precedent that goes against “selling cash to buy stocks” is the Fed rate-cutting cycle. Such was a point discussed last week in “Markets Are Front Running The Fed:”

“Since 1970, there have been nine instances in which the Fed significantly cut the Fed Funds rate. The average maximum drawdown from the start of each rate reduction period to the market trough was 27.25%. The three most recent episodes saw larger-than-average drawdowns. Of the six other experiences, only one, 1974-1977, saw a drawdown worse than the average.”

Of course, the point of that particular article was the 13 years of massive monetary and fiscal interventions have trained investors to buy stocks at the first sign of trouble. Whether or not “quantitative easing” and zero interest rates directly influence stock prices, psychologically, investors now associate any easing of financial conditions as a reason to own equities.

Should We Discard The Warning?

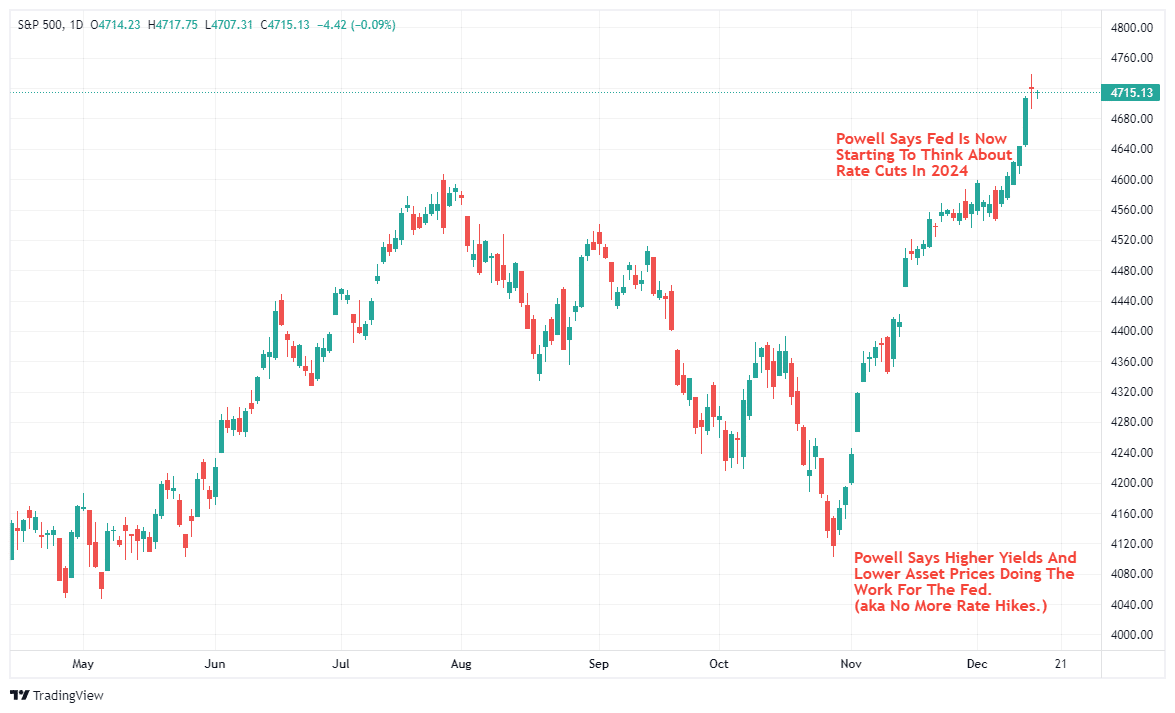

Since November, the runup in asset prices has been stunning. Such is particularly the case given the more extreme investor bearishness that existed until October’s end. In just two months, investors went from being assured a recession was forthcoming to believing a “no recession” scenario was not just possible but probable.

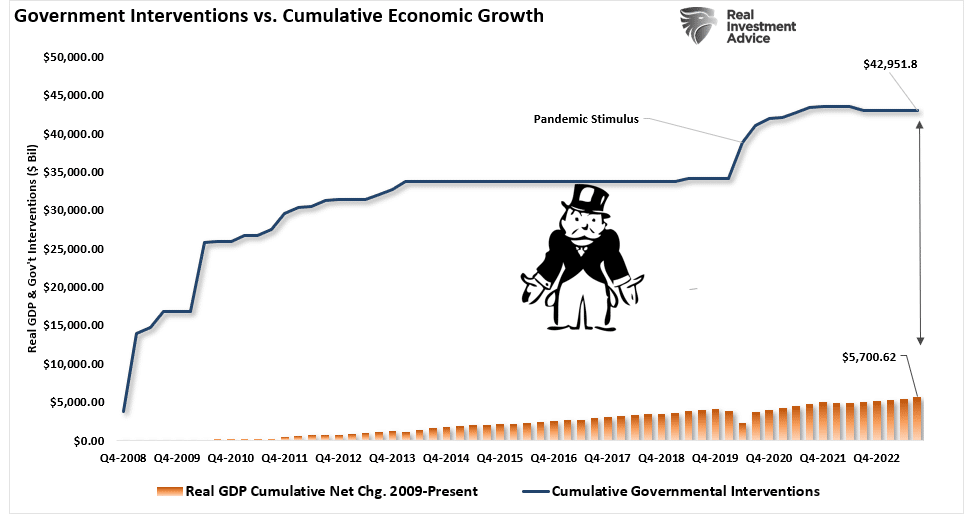

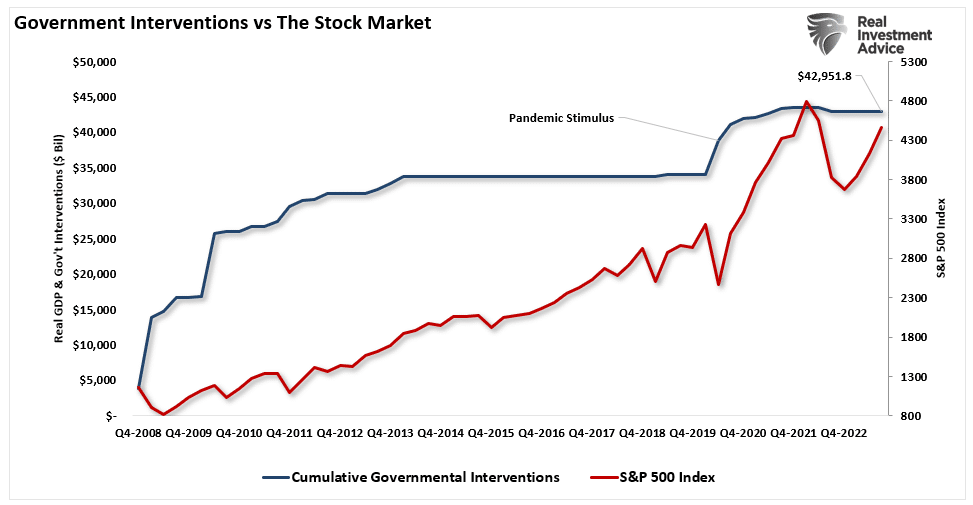

As discussed in our last post, this rapid psychological change is a function of more than a decade of fiscal and monetary interventions that have separated the financial markets from economic fundamentals. Since 2007, the Federal Reserve and the Government have continuously injected roughly $43 Trillion in liquidity into the financial system and the economy to support growth.

That support entered the financial system, lifting asset prices and boosting consumer confidence to support economic growth.

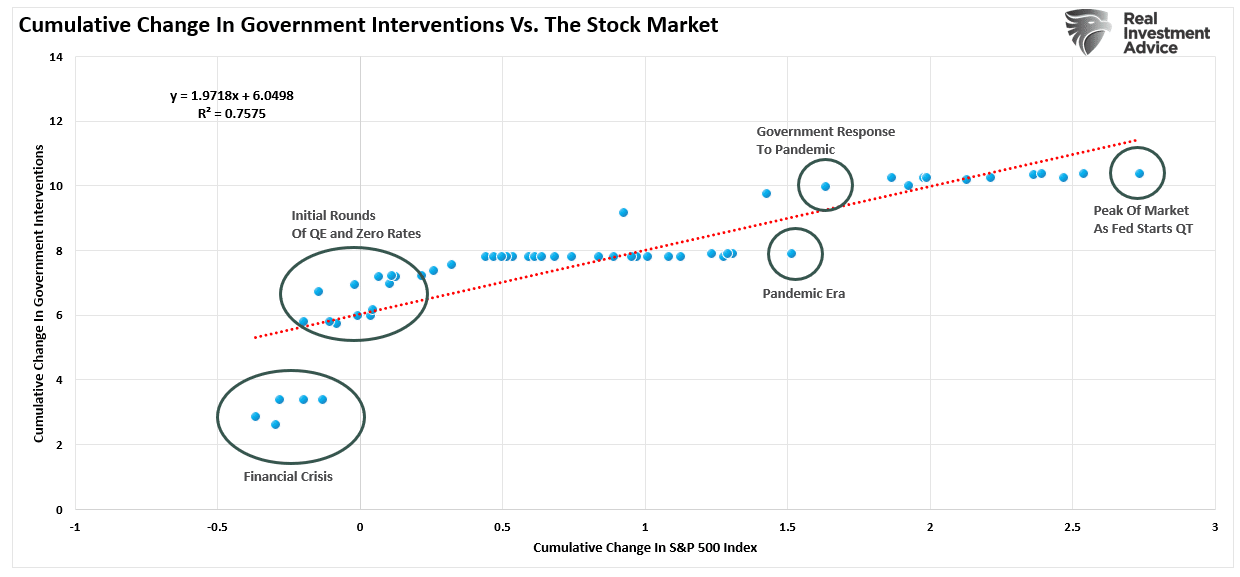

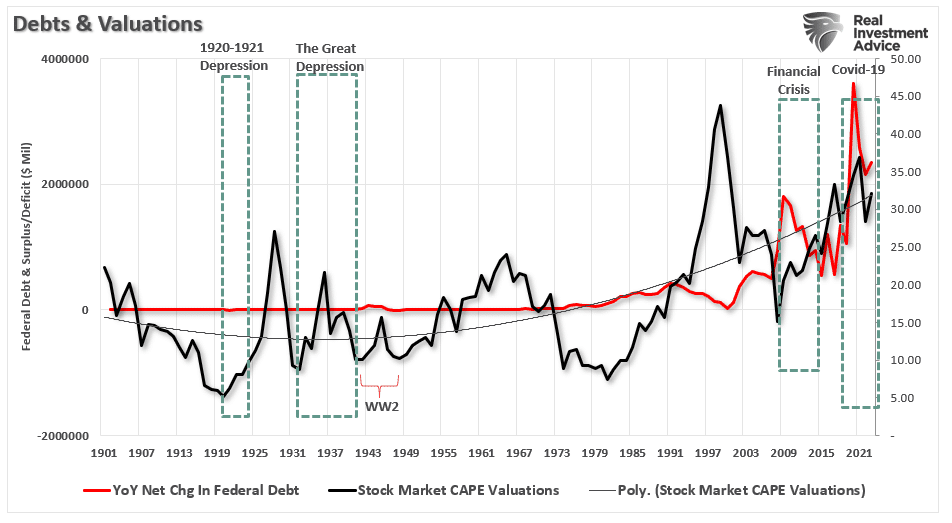

The high correlation between these interventions and the financial markets is evident. The only outlier was the period during the Financial Crisis just before the Fed launched the first round of Quantitative Easing or Q.E.

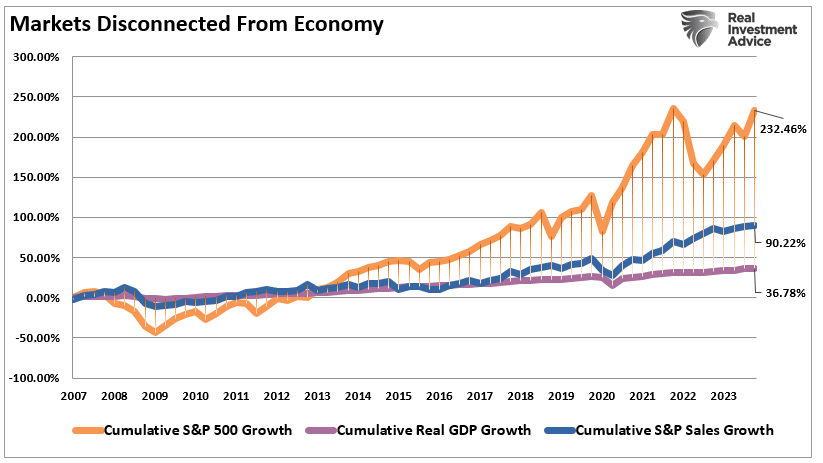

However, as those injections led to a cumulative increase of 232% for the stock market, they did not translate into vastly stronger economic growth. Since 2007, real economic growth has only grown by 37% as corporate revenue rose by just 90%. In other words, stock prices rose 6x more than the economy and 2.7x more than corporate revenue.

As noted in our previous article, the problem is that the Federal Reserve has now trained investors to buy stocks when it is easing financial conditions. To wit:

“Any financial or recessionary event jeopardizing the markets would be met with rate cuts and accommodative policy. That training was completed with the Fed’s response to the ‘pandemic-era shutdown’ that led to massive monetary and fiscal interventions.

There is currently a large contingent of investors who have never seen an actual “bear market.” For many investors in the markets today, their entire investing experience consists of continual interventions by the Federal Reserve. Therefore, it is unsurprising investors are fully trained to “fear of missing out” on the next round of Fed support.“

The problem, however, is that in the future, there will likely be less financial support than seen over the last decade.

Sell Cash And Buy Stocks?

It is logical after 13 years, any hint the Fed will reverse course on policy is met with a rush to buy equities. Since the lows of October, such is precisely what the market has been doing.

However, while lower interest rates will undoubtedly provide some support by boosting consumer confidence and increasing economic activity, there is a difference.

Since 2008, as shown above, lower rates have contributed to higher asset prices. However, because of the current levels of government debt and deficits, there will be less ability to foster similar levels of intervention in the financial markets and the economy. Given substantially higher valuations relative to 2008, the ability for stocks to generate previous returns may become more challenging.

While I agree in the short-term that given the inexperience of most investors in the market today, the sentiment to “sell cash and buy stocks” seems an obvious choice. As a portfolio manager, it is something that we must do or potentially suffer career risk.

However, we are also aware that there is more than a slight chance that the recession indicators will eventually be correct, the economic contraction will impact earnings growth, and valuations will again matter.

Conclusion

The problem is if a recession occurs, it will be due to some exogenous, unexpected event that no one is currently considering. A good example was 2019. The Fed started to cut rates and engaged in a massive repo operation as many indicators warned a recession was coming. No one saw the “pandemic” event coming, but it did, and it was the trigger that pushed the economy into recession.

Once again, all of those warnings are in place. Few believe a recession is coming, and they will likely be correct in their calls to sell cash and buy stocks. That is, for now, until some event occurs.

What that event will be, I haven’t a clue. And, yes, you should be long equities in the current environment because the trend and the sentiment are bullish.

But that doesn’t mean the markets can’t or won’t change for the worse in the future.

Related: The VIX Index Warns of Complacency