Trending

Monday, McDonalds issued a health warning in their earnings announcement. The warning is not about the physical health of its consumers but the customers’ financial health. McDonalds global sales were down 1%, and U.S. sales fell by 0.7% in the second quarter. Moreover, as shown below, its same-store sales have fallen for the first time since 2020. Same-store sales only account for revenue from existing stores. Thus, revenue added due to the growth in the number of stores is eliminated. This is the preferred measure of sales for most retail outlets.

The McDonalds CEO opened the earnings call by saying low-end consumer weakness has deepened and broadened. We have heard this theme in many retail earnings announcements over the past six months. Savings have been depleted, and credit card debt has accelerated, leaving many consumers lacking funds to consume at prior rates. Typically, lower-end restaurants like McDonalds fare well during economic slowdowns or recessions due to their low prices. This time, however, its prices are not so low in the consumer’s mind. The Big Mac, for instance, averages $5.29, an increase of over 20% since the pandemic. Throw in fries and a drink, and the meal is over $10 in many locations. Any wonder McDonalds extended its $5 value meal, and many of its competitors offer similar deals.

What To Watch

Earnings

Economy

Market Trading Update

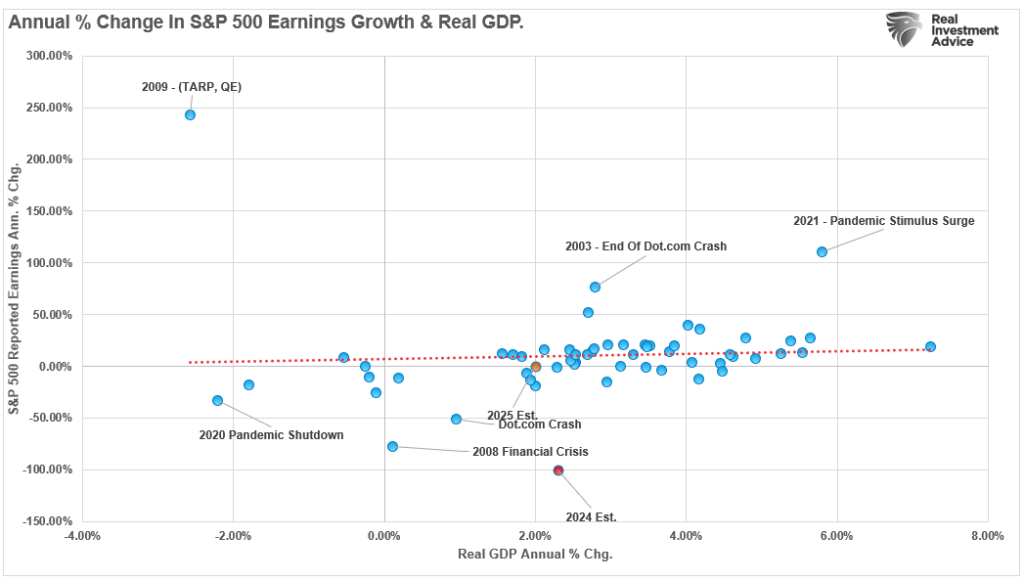

At the beginning of July, we discussed the “lowering of the earnings bar” for the Q2 reporting period. To wit:

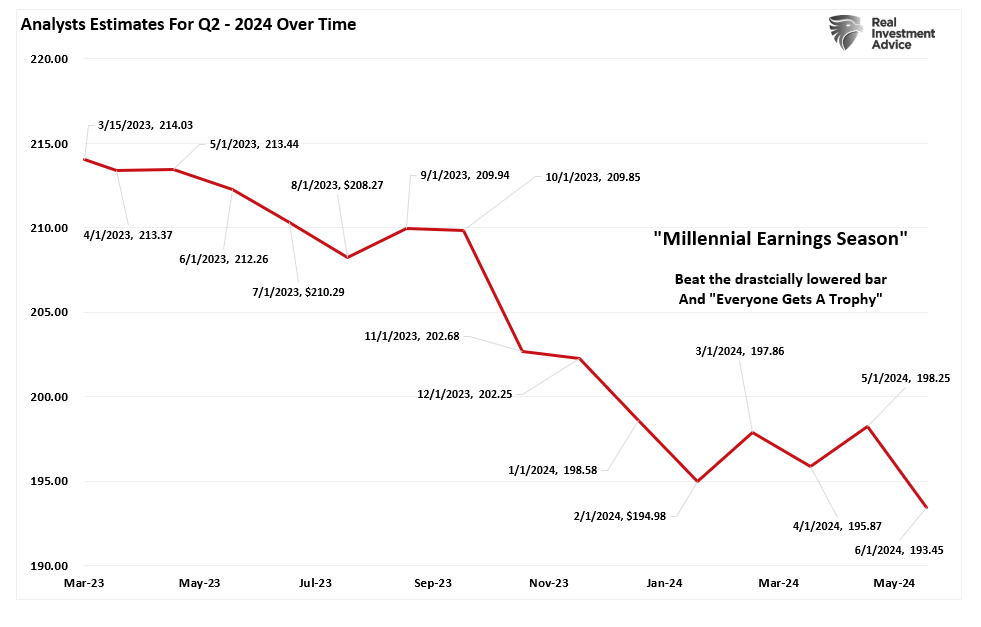

“It will be unsurprising that we will see a high percentage of companies “beat” Wall Street estimates. Of course, the high beat rate is always the case due to the sharp downward revisions in analysts’ estimates as the reporting period begins. The chart below shows the changes for the Q2 earnings period from when analysts provided their first estimates in March 2023. Analysts have slashed estimates over the last 30 days, dropping estimates by roughly $5/share.”

“That is why we call it “Millennial Earnings Season.” Wall Street continuously lowers estimates as the reporting period approaches so “everyone gets a trophy.” An easy way to see this is the number of companies beating estimates each quarter, regardless of economic and financial conditions. Since 2000, roughly 70% of companies regularly beat estimates by 5%, but since 2017, that average has risen to approximately 75%. Again, that “beat rate” would be substantially lower if investors held analysts to their original estimates.”

During just this past month, the expected earnings for not just Q2 but through 2025 have been cut further. As noted by Jefferies:

“….the negative revision skew (to earnings) is below the magic 1x level and bottom quartile. Although the magnitude of cuts is different vs. lockdowns & the tech layoffs, the mismatch between CY25 expectations earlier in the year vs. now looks widespread across most sectors as 7 of 11 are <1x.”

Given the current state of consumer data and the potential for slower economic growth in the months ahead, current Wall Street expectations seem overly optimistic. Furthermore, given the correlation between earnings and economic growth, a more cautious outlook would seem in order.

As noted previously:

“For investors, the most significant risk to portfolios is not inflation but most likely disinflation as the economy, and ultimately earnings, come under pressure in the months ahead. Such is crucial given that expectations for earnings growth in the overall index remain elevated, but that growth depends on just 7 stocks. In fact, since the beginning of this bull market cycle in Q4 of 2022, there has been ZERO earnings growth in the bottom 493 stocks of the S&P 500.”

We must pay close attention to consumer data. It will likely provide the warnings necessary to reduce equity risk in portfolios.

As the economy slows, the subsequent decline in earnings is unsurprising. With valuations high, a deeper correction to revert company prices to slower underlying earnings growth is becoming a higher probability event. As such, we suggest remaining cautious for now and managing exposure to companies with the highest probability of negative earning revisions in the near term.

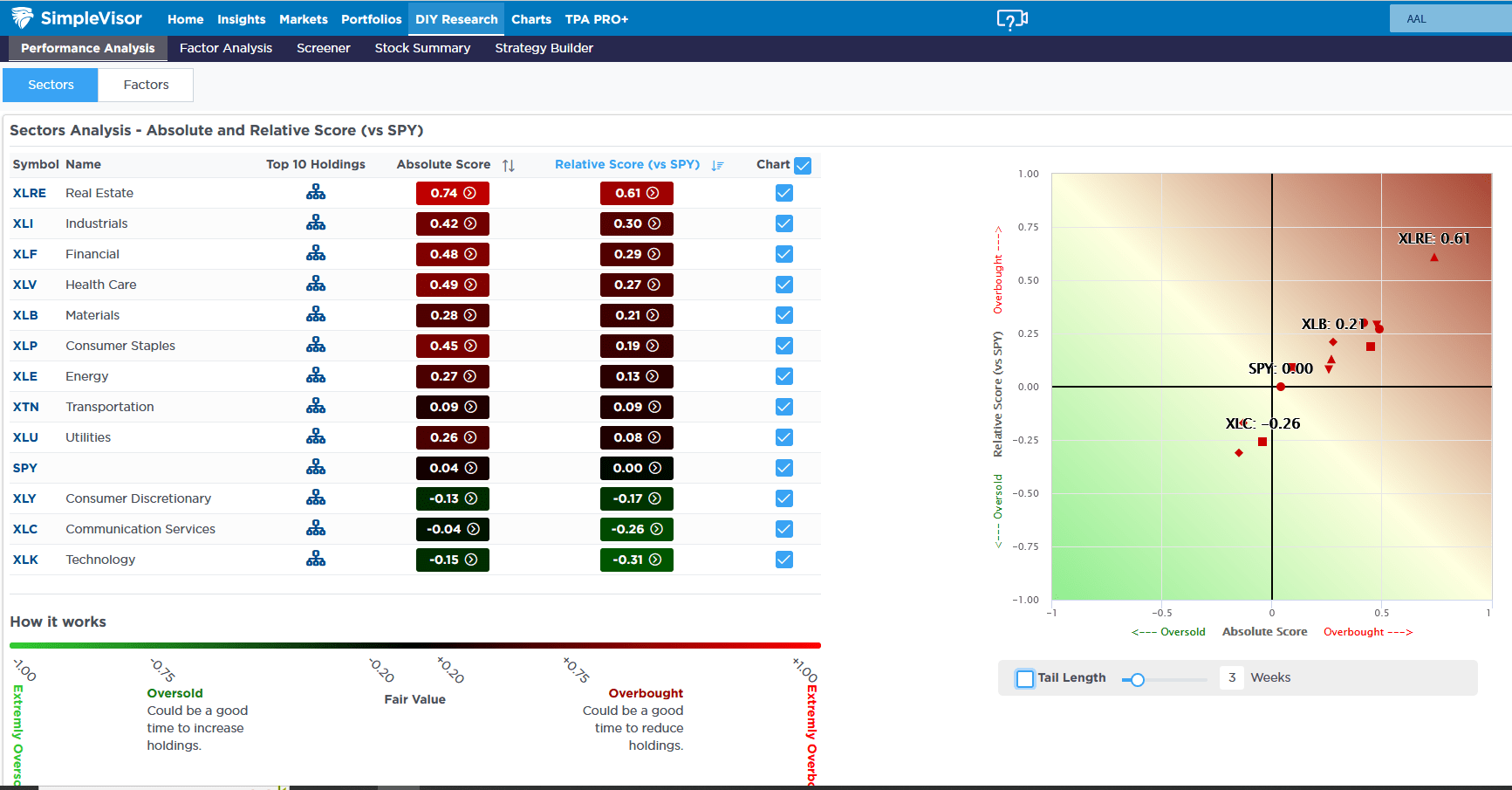

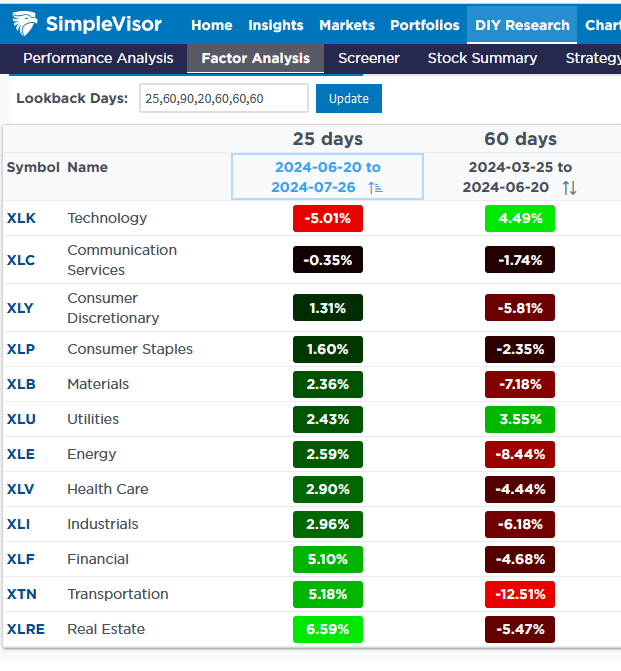

Is The Rotation Trade Over?

Over the last few weeks, the gross market imbalances of 2024 have somewhat normalized. The question now facing investors is whether the rotation trade away from the largest stocks continues. The recent severe rotations and the minor S&P 500 correction from record highs leave the market in a healthier condition than it was a few weeks ago. SimpleVisor can help us appreciate the changes in the market by sector and help guide us on what’s next.

The first graph below highlights that the sectors’ relative scores (versus the S&P 500) show that 2024 laggards like Real Estate and Financials are the most overbought. Conversely, Communications and Technology are the most oversold. Neither the overbought or oversold sectors are in extreme territory. Thus, the rotation can undoubtedly continue. The second table compares the relative performance of each sector to the S&P 500 over the last 25 days and the 60 days before that. This, too, shows the market balance has improved markedly over the previous five weeks.

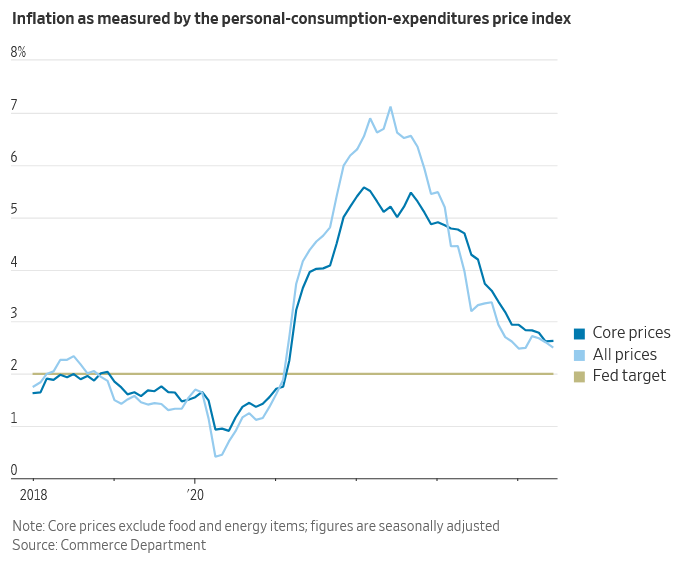

WSJ’s Nick Timiraos Signals September Rate Cut

The Fed’s media mouthpiece, Nick Timiraos of the Wall Street Journal, all but affirmed the Fed would not change rates tomorrow but will likely cut in mid-September. Per his latest, A Fed Rate Cut Is Finally Within View.

At each of their four meetings this year, interest-rate cuts have been a question for later. This time, though, inflation and labor-market developments should allow officials to signal a cut is very possible at their next meeting, in September.

Per his article, the Fed’s case rests on three factors as follows:

The Fed’s newfound readiness to cut rates reflects three factors: better news on inflation, signs that labor markets are cooling and a changing calculus of the dueling risks of allowing inflation to remain too high and of causing unnecessary economic weakness.

Regarding his three points, the graph below shows that PCE prices are closing in on the Fed’s 2% target. Per Fed estimates, it should reach the target in late 2025. In regards to the labor market, they are comfortable with current levels of hiring and unemployment but are mindful of the weakening trends. Moreover, they want to arrest any further weakness that may develop. The third point is risk management, or balancing inflation and labor market goals properly. They appear fearful of cutting too late, just as they waited too long to raise rates in 2022.

The Fed was late to raise interest rates two years ago in part because it had incorrectly judged inflation would subside rapidly. The Fed was able to correct that mistake, but to do so, had to rapidly raise rates from near zero in 2022 to around 5.3% in July 2023, the highest in more than two decades. One lesson: “When you’re too confident that your view is correct, you’re prone to mistakes,” said San Francisco Fed President Mary Daly.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Is the Market Decline and Rotation Linked to the Yen