Trending

One thing is clear from this week’s “Liberation Day” tariff announcement –the market has decided that there is pretty much no way to spin it as a positive. Thus, here we are with a substantial selloff on our hands, abetted somewhat by traders whose commitment to buying every dip left them wrong-footed.

We wrote yesterday that traders seemed to be pricing in a “sell the rumor, buy the news” scenario. The probability of outcomes indicated by S&P 500 Index options expiring today and tomorrow showed peaks above at-money levels. In other words, speculators became more concerned with missing a rally than protecting against a drop. Remember, thrice this week we saw early selling abate quickly, which was seen as yet another “buy the dip” opportunity by aggressive traders. Some must have thought that a bottom was in place.

Yet we also pointed out a significant concern about a “buy the news” outcome – there was no clear consensus on what might be considered “good” or “bad”. We normally go into a “known unknown” type of event, like earnings, a Fed meeting, or an economic report, with a clear consensus for what outcomes might be considered positive or negative for asset prices. In this case, the range of potential outcomes was so wide and the administration was so tight-lipped about their plans that it was impossible to state a clear set of desired or consensus outcomes for the market.

That’s why the first move was up when “reciprocal tariffs” was mentioned. That sounded rather benign. At the time, one of my colleagues reminded me of my perpetual admonition to our trading desk after an FOMC announcement: “the first move is often the wrong move.” This time it certainly was, and as soon as the magnitude of the tariffs was visibly displayed, the reality became clear — this was not going to helpful for prices or economic output. We could see in black and white that the tariffs were quite far-reaching and combined some amount of baseline tariffs and variable rates. Again, while we didn’t have a clear delineation of good/bad, or positive/negative, there was no real way to interpret those tables in a market-friendly manner.

We then tried to learn more during an interview with Treasury Secretary Bessent on Bloomberg. His comments were spectacularly unhelpful. He admitted to being unsure about why Canada and Mexico were left off the charts (the administration did decide to honor goods and services covered by the USMCA, except autos), claimed not to care about after-hours market movements, and asserted that the selloff was “a Mag 7 problem, not a MAGA problem”. He also said that we’re “going to go to the warning track” about a potential debt ceiling breach in May or June. Nervous traders wanted to hear something to assuage them, and nothing of that nature was forthcoming. Commerce Secretary Lutnick made the rounds this morning, hitting a wide range of financial and mainstream media outlets, but his comments also failed to mollify nervous global investors.

Interestingly, the tariffs aren’t even truly reciprocal, though they are described that way. Instead, they are essentially calculated by the US trade deficit with each country, divided by total imports from that country (the math is on the USTR website), subject to a minimum of 10%. This too has not helped the market mood.

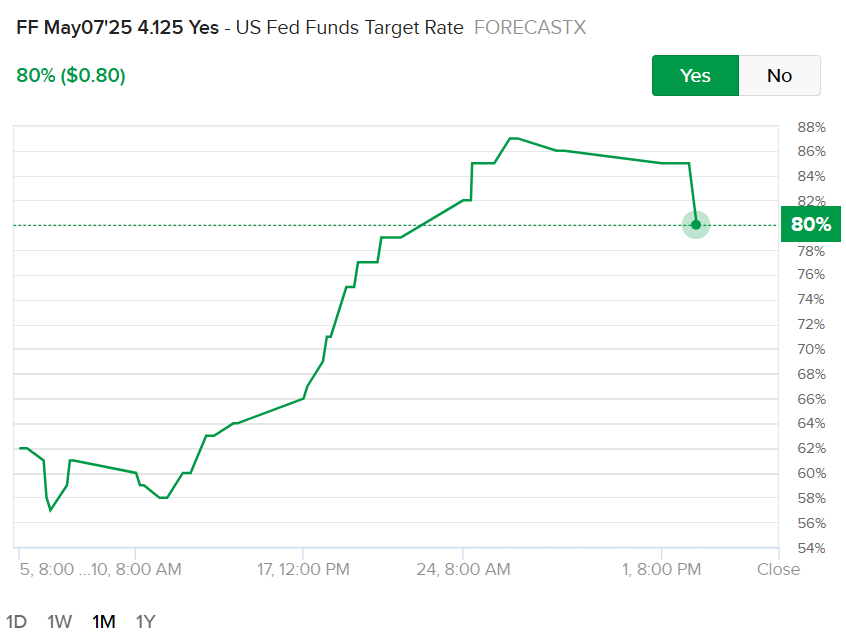

Thus, we find ourselves staring at significant dislocations across a wide range of asset classes. We have SPX -3.8% at midday, the Nasdaq 100 (NDX) -4.4% lower, and the Russell 2000 (RTY) down by -5.5%. The US Dollar has lost over 3 yen and 2 Euro cents this morning. Part of that move is caused by plunging bond yields, with the 2-year yielding 13 basis points less than yesterday and the 10-year down -8.5bp. Some of that move is caused by increasing expectations for Fed rate cuts this year. Here is just one example from the IBKR Forecast Trader:

Forecast Contract by ForecastEx LLC: Will the US Fed Funds Target Rate be set above 4.125% at the FOMC meeting ending May 7th, 2025

Source: IBKR ForecastTrader

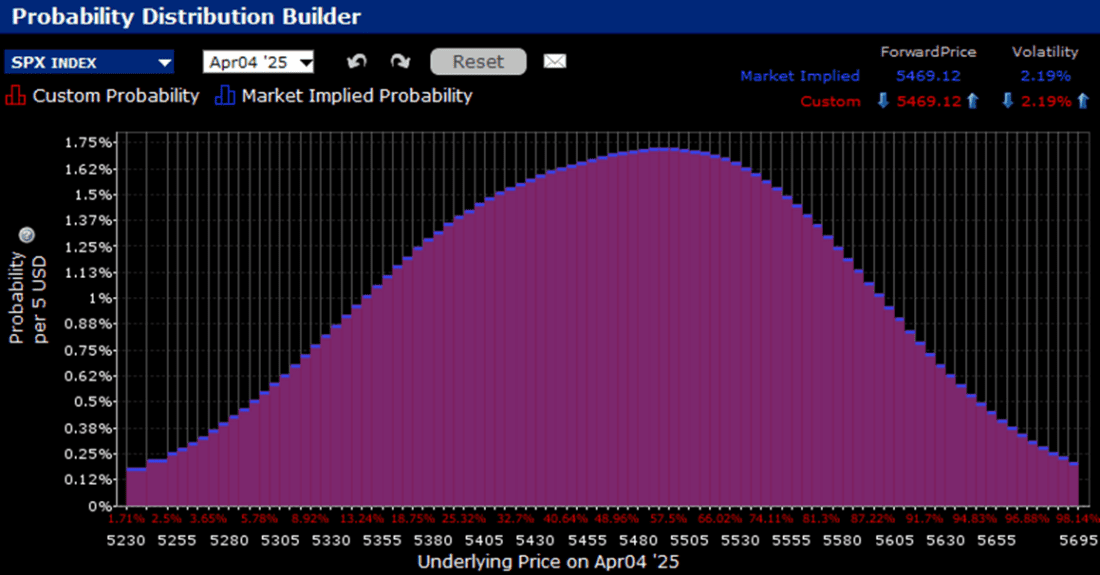

Amidst all today’s volatility, we have yet another potential market mover on tap for tomorrow morning – the March employment report. Consensus expectations – remember them? – are for an increase of 140,000 Nonfarm Payrolls, down from 151k in February, and an Unemployment Rate that will remain at 4.1%. The IBKR Probability Lab once again shows a slight bias toward a bounce, though far less pronounced than yesterday – and at far lower levels.

IBKR Probability Lab for SPX Options Expiring April 4th, 2025

Source: Interactive Brokers

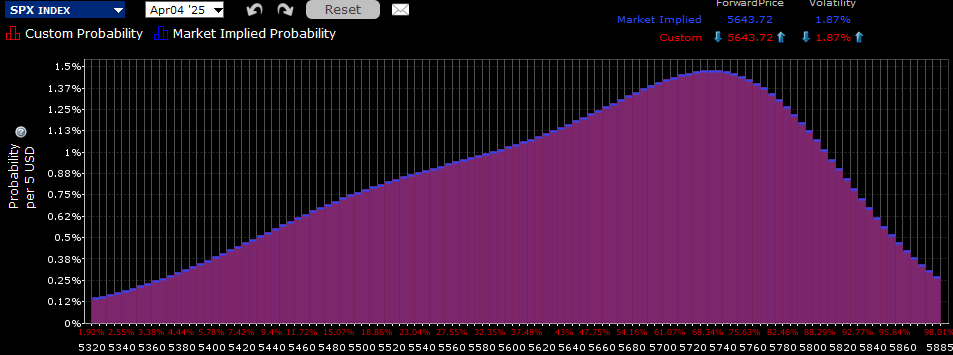

IBKR Probability Lab for SPX Options Expiring April 4th, 2025, as of April 2nd, 2025

Source: Interactive Brokers

Related: Tariff Clarity: What It Means for Businesses, Investors & Consumers