Trending

Several articles published lately suggest that stocks perform well in higher inflation environments. That may be the case when inflation rises due to more robust rates of sustainable economic growth. However, history suggests sharply rising inflation not only negatively impacts economic growth but triggers adverse market environments.

Let’s start with the “bullish spin” from Dimensional Advisors. To wit:

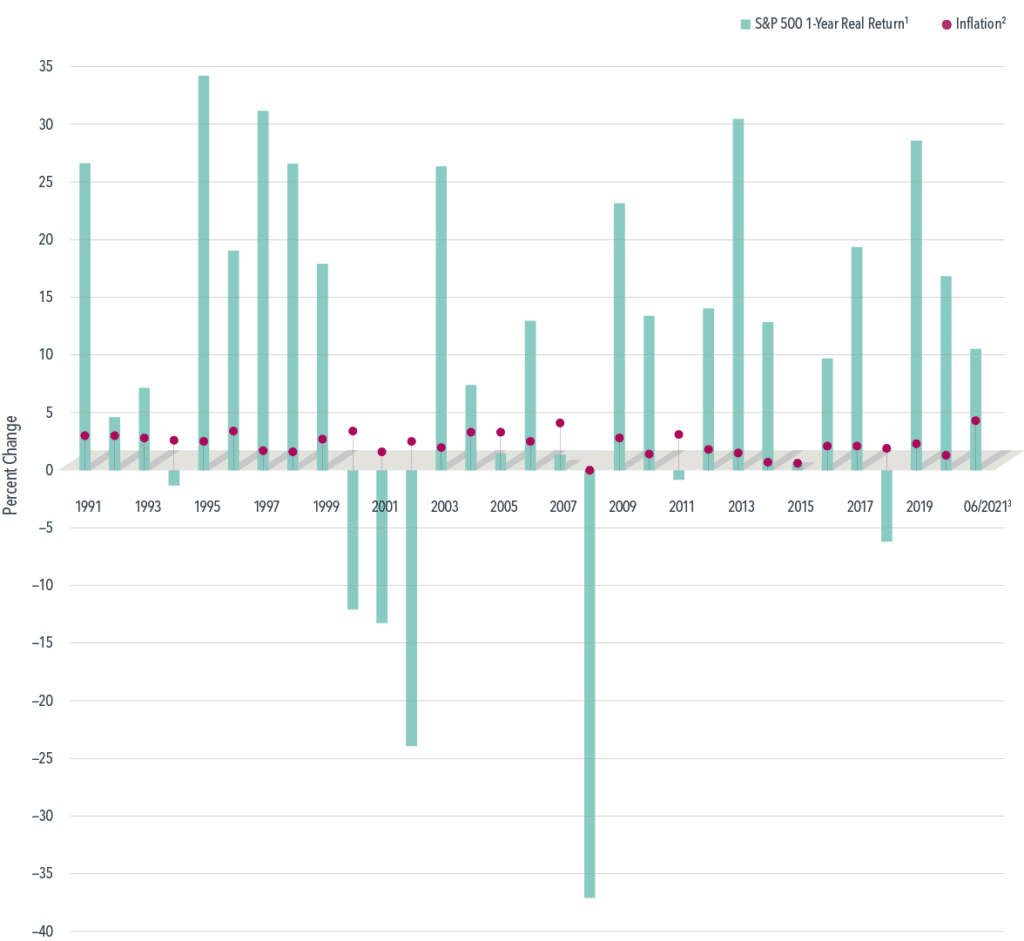

“A look at equity performance in the past three decades does not show any reliable connection between periods of high (or low) inflation and US stock returns.

Since 1991, one-year returns on US stocks have fluctuated widely. Yet weak returns occurred when inflation was low in some periods, and 23 of the past 30 years saw positive returns even after adjusting for the impact of inflation. That was the case in the first six months of 2021, too (see Exhibit 1).”

Since 1991, the period they chose to represent the market, the S&P 500 posted an average annualized return of 8.5% after adjusting for inflation. However, even going back to 1926, the annualized inflation-adjusted return on stocks was 7.3%.

As Dimensional Fund Advisors suggest, investors should not worry about inflation as stocks outpace inflation over time.

The problem with the analysis is the “cherry-picking” of starting points.

Average And Required Returns Aren’t The Same

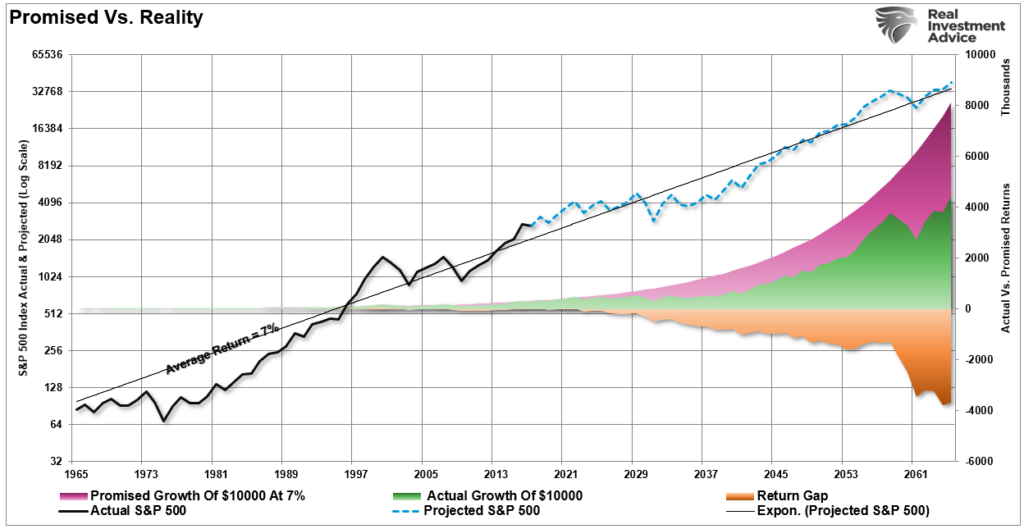

The problem with AVERAGE returns, as noted by Dimensional, is there is a vast difference between “average” returns over a given period and “required” returns to meet financial goals. As we discussed in the “Best Way To Invest:”

“There is a massive difference between AVERAGE and ACTUAL returns on invested capital. Thus, in any given year, the impact of losses destroys the annualized “compounding” effect of money.

The chart below shows the difference between ‘actual’ investment returns and ‘average’ returns over time. See the problem? The purple shaded area and the market price graph show ‘average’ returns of 7% annually. However, the return gap in ‘actual returns,’ due to periods of capital destruction, is quite significant.”

There are two other problems with Dimensional’s analysis.

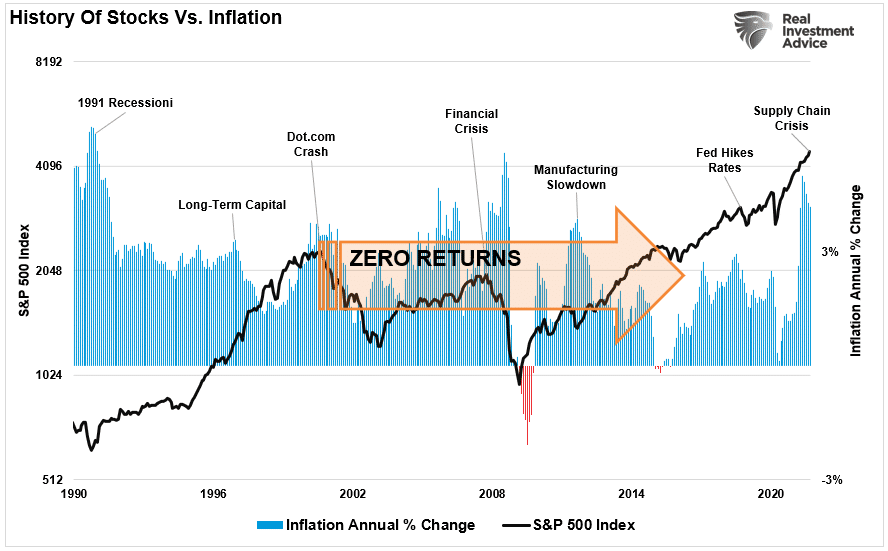

Since 1990, the first data point used for the “bullish” case, inflation has steadily fallen. Such gave a significant boost to equities as input costs fell, increasing corporate profitability. More importantly, however, returns were heavily front and back-end loaded, masking the nearly 13-year period of ZERO returns for investors.

The second problem stems from their use of 1926 to the present time frame. While using such a time frame certainly paints a very bullish picture of 8% annualized returns, the reality is that you died somewhere around the early 1950s. Such sounds great until you realize you barely got back to even following the crash of 1929 and the “Great Depression.”

As noted, there is a massive difference between an “average rate of return” and what actually happens to your money when “bear markets” destroy the “compounding effect” of your investment capital.

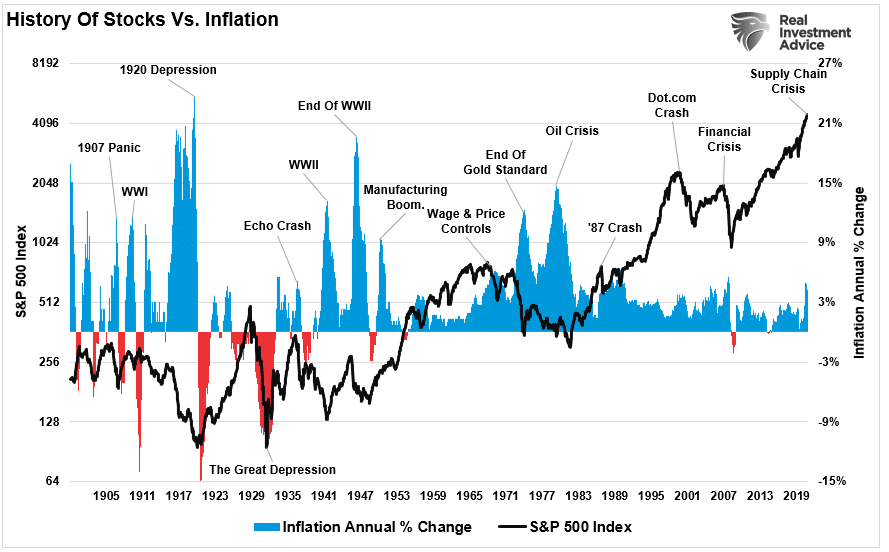

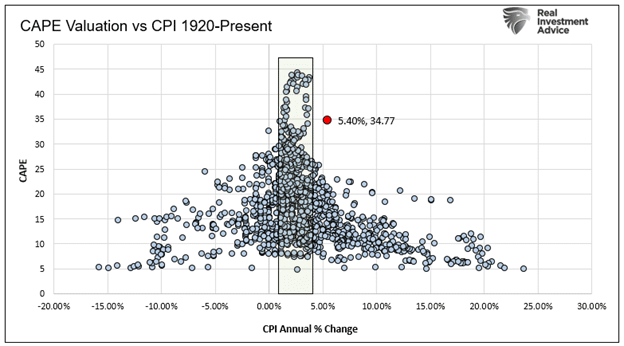

History Of Inflation & Markets

However, the long-term view of inflation helps determine its impact on the economy and market over time.

Not surprisingly, as shown below, spikes in inflation have been coincident with crisis events throughout history. From banking crisis to economic recessions, to devastating bear markets, inflation spikes triggered revulsions.

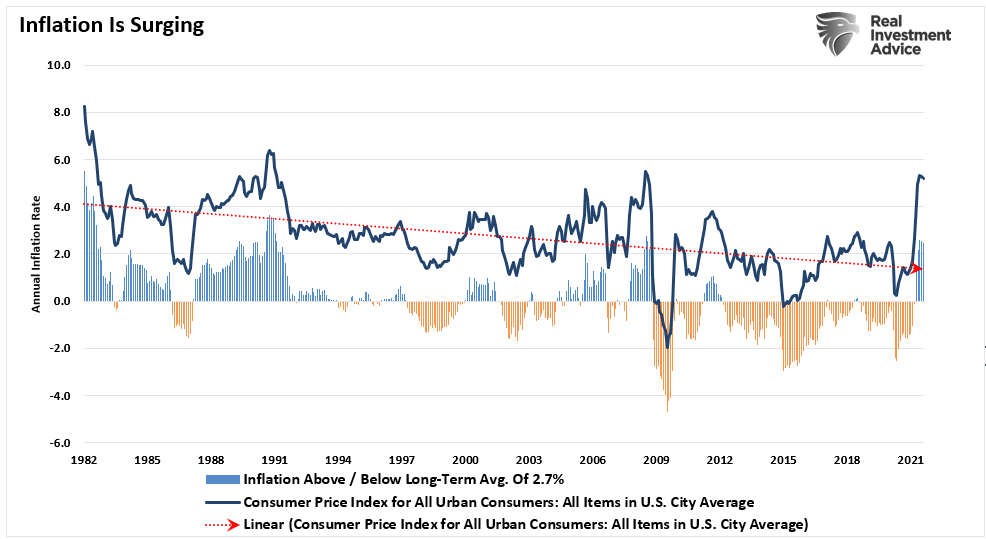

The current spike in inflation is still minor relative to historical triggers but is worth watching closely. Earlier this year, the primary belief by the Federal Reserve was that inflation was “transient” and would quickly resolve itself. However, as Michael Lebowitz noted recently, that outlook is changing for the worse.

“The Fed is starting to acknowledge this bout of inflation may last longer than a “transitory” period. Per Atlanta Fed President Raphael Bostic, ‘U.S. inflation is broadening, not transitory.’ His statement is the first recognition from a Fed member that higher inflation may no longer be transitory.”

As he notes, the big problem, when it comes to the stock market, is “margin compression.”

“In six of the seven inflationary periods, including both episodes in the 1970s, corporations experienced margin compression. The era of moderate inflation, following the 2008/09 recession, was the only period where margins improved.

Profit margins are now at their highest levels since at least 1947. If inflation continues higher and margins decline, profits will suffer. If earnings decline due to declining margins and valuations fall to levels in line with prior periods of inflation, stocks could easily fall by 40-50%. Even more significant declines would not be abnormal.”

The biggest problem is the Fed won’t be able to bail investors out.

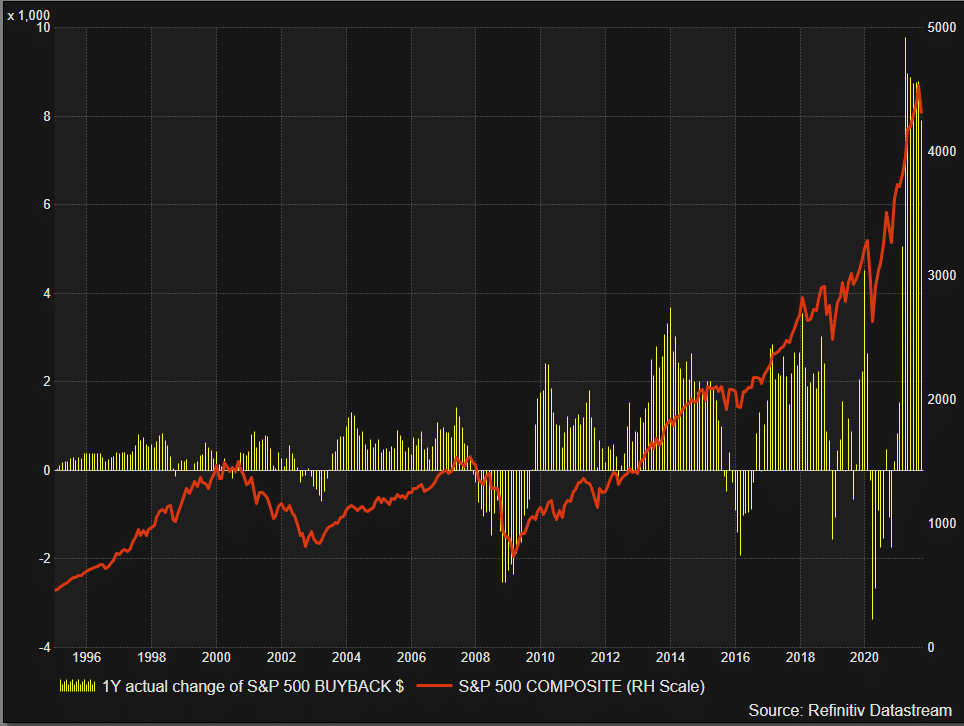

The Fed Will Be Trapped By Inflation

Over the last decade, two primary supports significantly elevated asset prices; 1) share repurchases, as shown below, and 2) the Fed’s monetary policy.

The problem for the Fed is inflation. In July 2020, we pinned our concerns about an inflationary surge:

“The ‘unlimited QE’ bazooka is dependent on the Fed needing to monetize the deficit to support economic growth. However, if the goals of full employment and economic growth quickly come to fruition, the Fed will face an ‘inflationary surge.'”

As we suggested then, should such an outcome occur, it will trap the Fed. The surge in inflation will limit the ability to continue “unlimited QE” without further exacerbating inflation. Furthermore, the Fed will have to hike rates, further tightening monetary policy, to counter inflation.

“It will be increasingly hard for Powell to claim the economy needs to make ‘substantial further progress’ toward achieving maximum employment before the Fed starts talking about tapering. Powell has repeatedly said the Fed is awaiting substantial further progress in the economy before terminating its stimulus. Given the performance of the economy, it is reasonable to expect they will start to taper before the end of the year, and a few months later they will start to raise the federal funds rate.” – Ed Yardeni

However, when they do that, asset prices fall, a recession starts, and the Fed gets trapped between fighting inflation and bailing out markets.

It’s a no-win situation for the Fed.

Conclusion

The issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter.

Since interest rates affect “payments,” increases in rates quickly negatively impact consumption, housing, and investment ultimately deters economic growth.

Given the current demographic, debt, pension, and valuation headwinds, the future growth rates will be low over the next couple of decades. Even the Fed’s own “long-run” economic growth rates currently run below 2%.

Notably, inflation driven by artificial infusions of capital, supply chain disruptions, and rising wages will eventually crush economic growth and corporate profit margins.

Unfortunately, the Federal Reserve, and the Administration, will have to face hard choices to deal with the current “liquidity trap.” The only question is do you bail out the stock market, or fix what is broken in the economy?

The problem for the Fed is they can’t do both.