Written by: Andy Acker, CFA and Daniel Lyons, PhD, CFA | Janus Henderson

Though healthcare may have flown under the market’s radar this year, the sector’s attractive valuations and new growth opportunities are not to be overlooked.

Healthcare stock returns have been essentially flat so far in 2023, which may lead some investors to overlook the sector.1 That could be a mistake given recent trends that, in our view, make the case for investing in healthcare even more compelling.

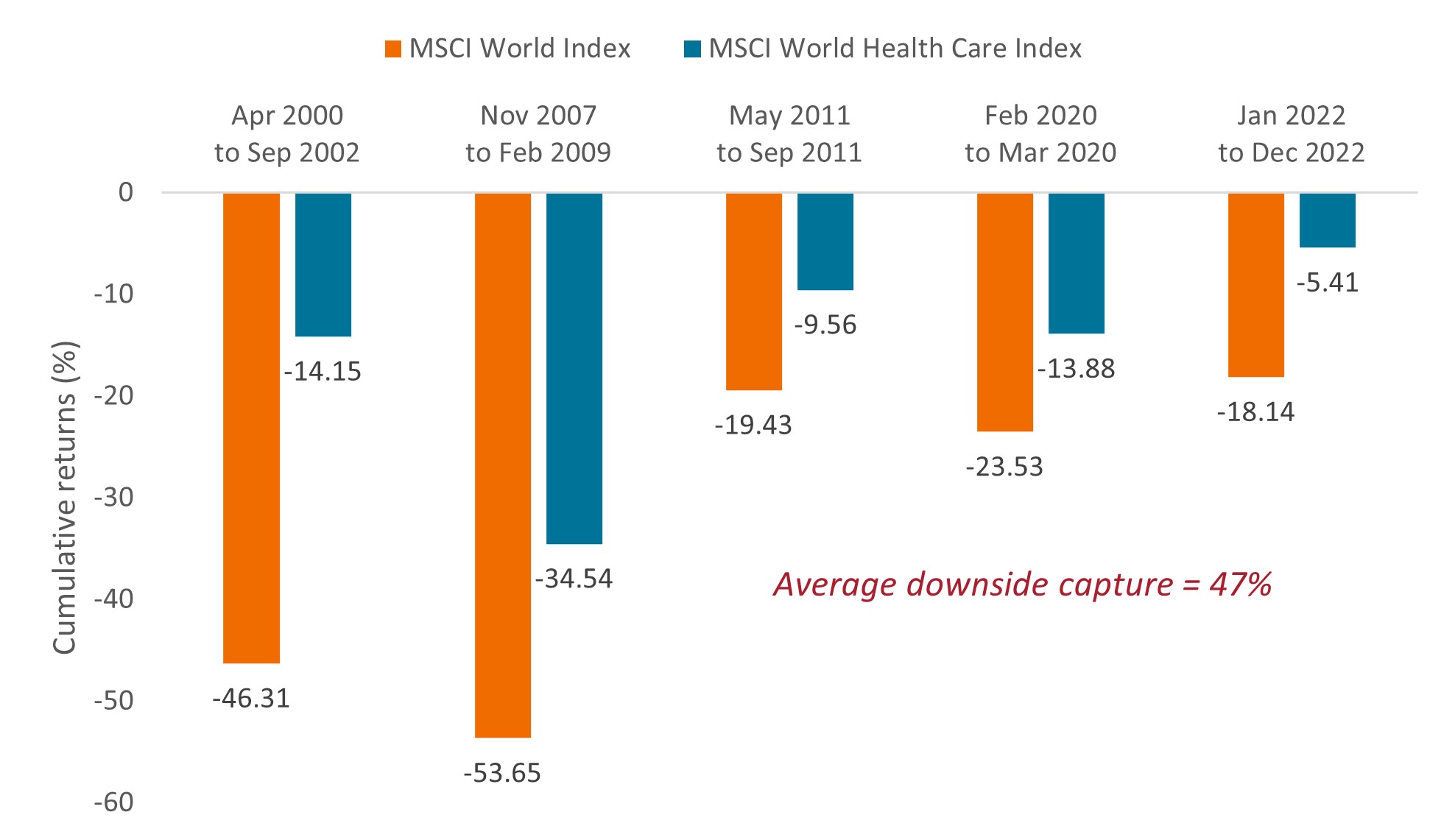

A history of downside protection

Although expectations for a recession have diminished, we believe the chances of an economic slowdown remain significant and underappreciated. The effects of monetary-tightening cycles take one to two years to fully materialize as higher rates and more restrictive lending work their way through the economy. Should a downturn occur, healthcare could be a port of refuge: Since 2000, the MSCI World Health Care IndexSM has, on average, captured just 47% of the downside when the MSCI World IndexSM has declined by 15% or more (Figure 1).

Figure 1: Healthcare’s performance and downside capture

Source: Janus Henderson Investors, FactSet, as of 30 June 2023. Chart reflects market declines of 15% or greater in the MSCI World Index since 2000. Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Even if a recession is avoided, healthcare could still perform well. Strong employment, for example, drives demand for employer-provided insurance policies, benefiting managed care providers. And positive clinical trial data and regulatory approvals can propel stocks higher regardless of the economic backdrop. This past May, one drugmaker saw its shares more than double in a single day after delivering groundbreaking data for its ovarian cancer drug candidate. Another firm saw double-digit gains after delivering positive data for a promising pneumococcal vaccine.

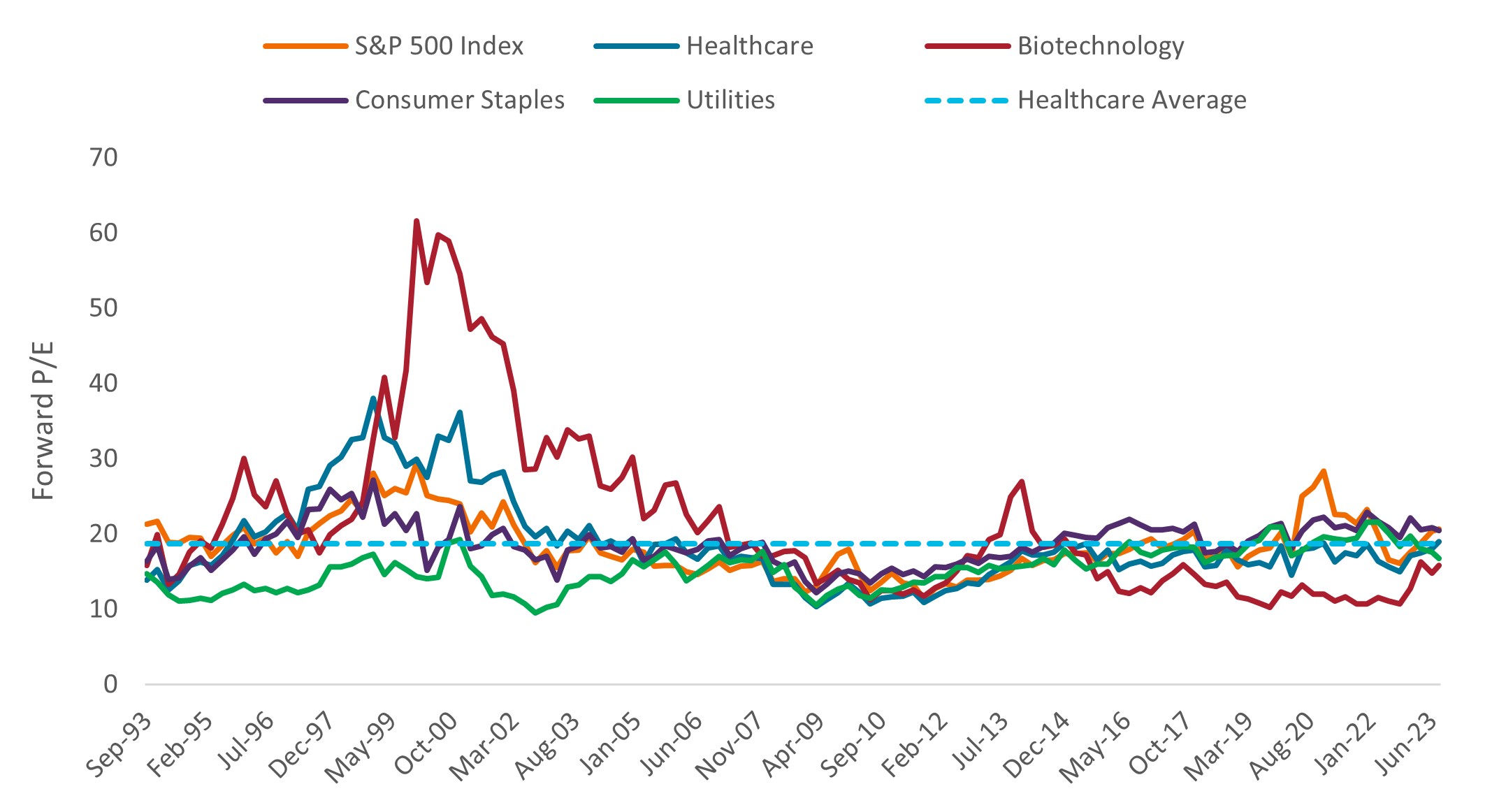

Attractive valuations

The healthcare sector trades at a discount to the broader equity market and roughly in line with its own long-term average. That is comparatively better than other traditionally defensive sectors, which as of the end of August traded at premiums to their historical valuations. In addition, after one of the worst drawdowns on record (Feb 2021 – May 2022), many biotechnology stocks trade at substantially depressed levels, with many priced below the level of cash on their balance sheets (Figure 2).

Figure 2: Healthcare looks comparatively attractive

Price-to-earnings (P/E) ratios based on estimated forward 12-month earnings

Source: Bloomberg, as of 31 August 2023. Average is for the 30-year trailing period. Data based on quarterly forward P/Es for the S&P 500 Index, the S&P 500 Health Care Sector, the S&P 500 Biotechnology subsector, the S&P Consumer Staples Sector, and the S&P Utilities Sector.

Some of this reflects the overhang from COVID-19: After the public health emergency ended, sales of vaccines and therapeutics declined sharply in 2023. That has also weighed on the fortunes of life sciences tools makers, which supply the components for manufacturing biologics. Meanwhile, a rebound in routine medical care, which many put off during the pandemic, has threatened to raise costs for insurers.

In our view, this reversion to the mean is more a return to normalcy and likely to be short-lived. Case in point: Insurers reported better-than-expected earnings during the second quarter as companies increasingly shifted to value-based services, keeping a lid on expenses. Premium increases next year could also help defray higher costs. Meanwhile, as COVID-19 wanes, other therapeutic areas such as obesity and Alzheimer’s are taking off, with the potential to lift revenues for branded drugs and tools.

Accelerating innovation

Indeed, rapid advances in clinical research have continued across numerous disease categories. This year, more than 80 novel medicines are up for Food and Drug Administration (FDA) review, with more than half already approved.2 That puts the sector on track for a record year of drug launches and creates the potential for years of revenue expansion, as drug product cycles typically last 10 years or longer.

This innovation has ignited a surge in mergers and acquisitions (M&A). Thirteen deals valued at $1 billion or more each have been announced so far in 2023, the most of any year in recent memory (Figure 3). Small- and mid-cap biotech companies have been the biggest targets of acquisitions – and the biggest beneficiaries, with some fetching premiums of between 60% and 100% (and even more).

Figure 3: M&A takes off

Source: Thomson Reuters, TD Cowen. Includes only deals ≥$1B USD. *2023 data as of 4 September 2023.

A complex sector ripe for stock picking

To be sure, many blockbuster drugs are set to lose patent protection by the end of the decade. (A blockbuster drug is defined as having sales of $1 billion or more annually.) There are also worries about the impact of the Inflation Reduction Act (IRA) on drug prices in the U.S. and the affordability of healthcare globally.

But as is often the case in healthcare, the details matter. Patent expirations, for one, have been another catalyst for M&A, as large-cap biopharma companies, flush with cash, seek to replenish pipelines. And while the loss of exclusivity opens some branded drugs to competition, it also works to improve affordability for patients and free up capital for the system to invest in newer innovations.

Regulation is also nuanced. Although the IRA allows Medicare, the U.S. insurance plan for the elderly, to negotiate prices for select drugs starting in 2026, the mandate comes with caveats. Orphan drugs (those treating rare diseases) are excluded. Small molecule medicines are exempt from negotiation for nine years and biologics for 13 years – around the time branded drugs lose patent protection anyway. Some aspects of the law could even be beneficial for the industry: Starting in 2025, out-of-pocket drug costs for seniors will be capped at $2,000 annually, which should improve affordability and perhaps grow sales volumes.

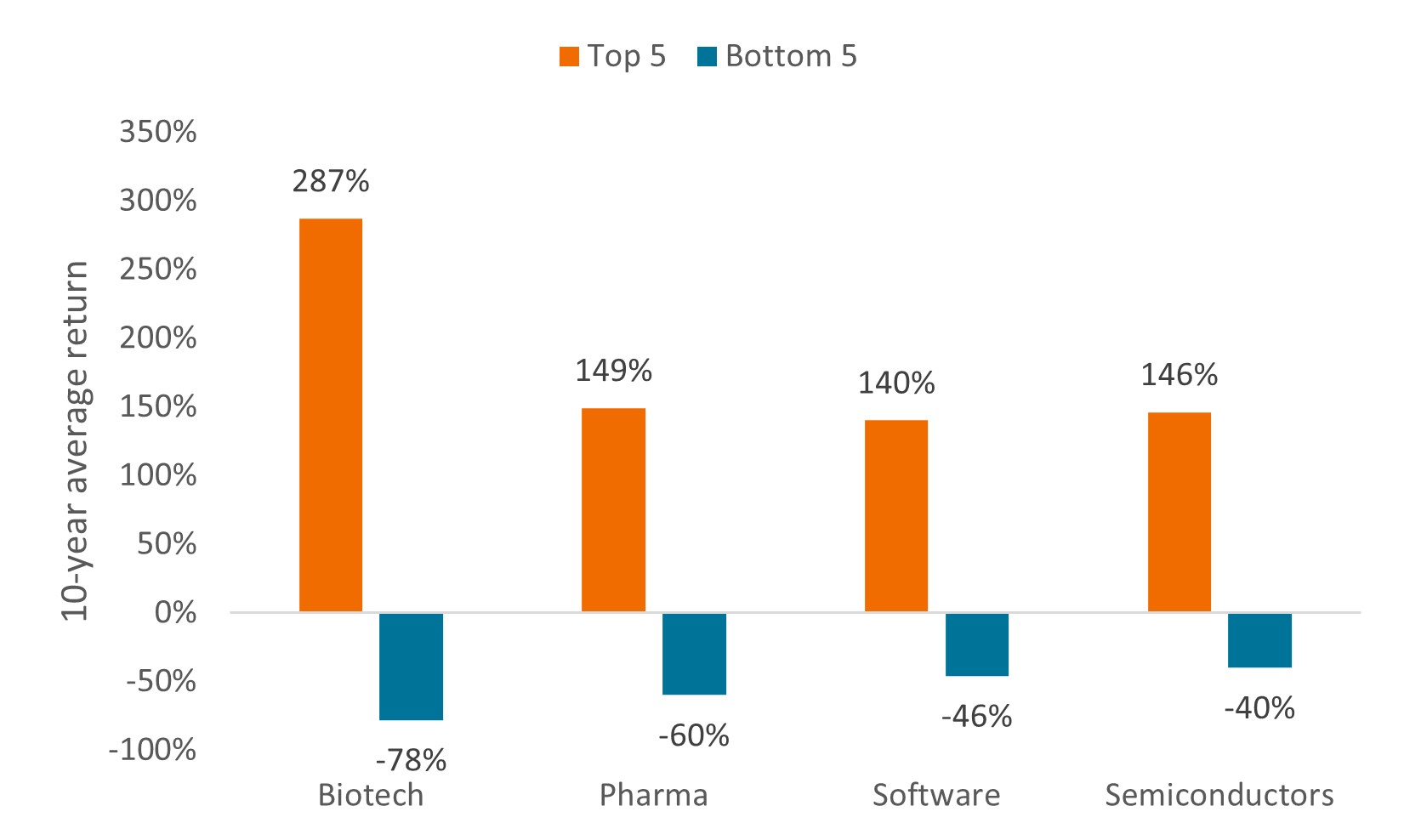

Given these complexities, along with the inherent risk of drug development, it’s no wonder there is a wide disparity between healthcare’s top- and bottom-performing stocks each year (Figure 4). As such, benchmark returns rarely reflect the full picture for the sector – or the investment opportunity.

Figure 4: A wide gap between healthcare’s top- and bottom-performing stocks

Source: Wilshire 5000 Index. Data from 2013-2022. Based on analysis of 10-year period.

A long runway of growth

It’s also worth considering the long term. Although healthcare spending is already substantial – in the U.S. it accounts for about 18% of the nation’s gross domestic product3 – we still see room for growth.

Demographics are one reason. By 2050, the number of people aged 60 and over is set to reach 2 billion, roughly double the figure in 2020.4 That age cohort typically spends three times more on healthcare than younger populations.5

Advances in medicine are also doing their part. Consider cystic fibrosis (CF): About a decade ago, the average life expectancy for CF patients was around 30 years. Now, thanks to improved therapies, the Cystic Fibrosis Foundation projects children born with CF today will live beyond 50 years. By extending lifespans, new therapies prolong demand and create more medical needs, spawning new companies and products.

With innovation expanding at a rapid clip and some of the largest drivers of mortality starting to get addressed, we believe this growth driver will only become stronger in the coming years. Investors should take notice.

Related: High-Net Worth Clients Want Risk Mitigation Strategies

1 Bloomberg, as of 31 August 2023. Returns are for the S&P 500 Health Care Sector and the MSCI World Health Care Index.

2 Food and Drug Administration, as of 31 August 2023.

3 Centers for Medicare and Medicaid Services, data for 2021.

4 World Health Organization, “Ageing and Health,” as of 1 October 2022.

5 JAMA Network, “Comparison of Health Care Spending by Age in 8 High-Income Countries,” 6 August 2020. Data reflect 2015 figures for those age 65 and older for Australia, Canada, Germany, Japan, the Netherlands, Switzerland, the UK and the U.S.