Trending

Written by: Vinay Thapar, CFA and Edward Bryan, CFA

In November, Americans will head to the polls to elect a president, reorder Congress, and weigh in on countless state and local races. Investors often view healthcare stocks as a risky prescription in election years, but the historical record tells a different story. And this time, the prospect of a divided government could be a mitigating factor.

Even minor shifts in political power can result in new legislation with meaningful implications for healthcare stocks. At first blush, 2024 would seem to be no exception. Drug pricing is a hot topic, with lawmakers on both sides of the aisle taking aim at the high cost of prescription medicine.

Perception vs. Reality: Healthcare Stocks and Politics

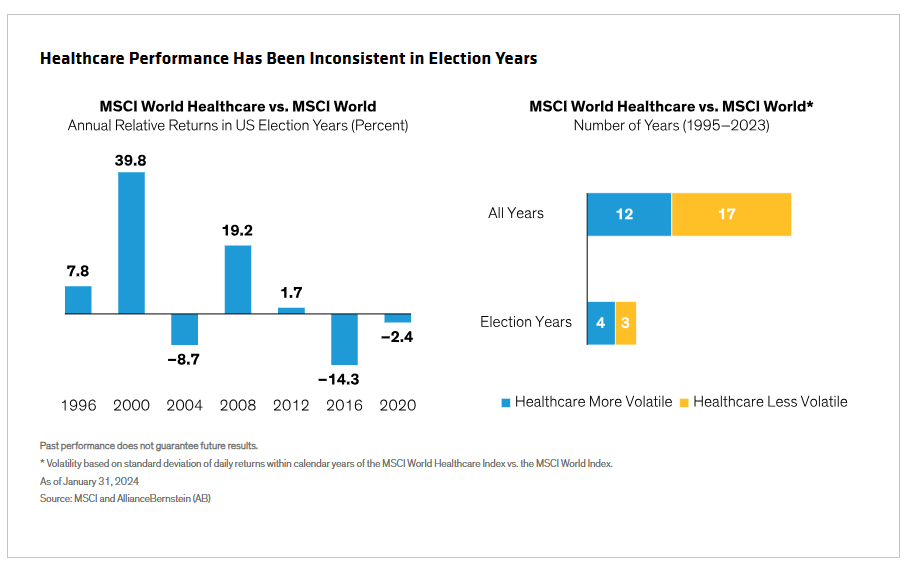

It’s true that public policy can influence healthcare stocks, but political uncertainty doesn’t always equate with market turbulence. In fact, the healthcare sector hasn’t shown any consistent return patterns or extreme volatility in election years (Display).

Why the disconnect between perception and reality?

For one, US companies with global business units aren’t always tied to specific US healthcare mandates. In addition, 10% of global GDP is spent on healthcare—a structural tailwind that should pick up momentum as populations age, regardless of short-term policy changes. Even firms that are more domestically oriented may have business models that are partially sheltered from US regulatory and reimbursement risks. Examples include “picks and shovels” stalwarts that operate behind the scenes to supply drug developers, medical device manufacturers and hospitals.

Diagnostics and software services are unlikely to face political pressure, particularly because they can help reduce costs for healthcare systems. Healthcare companies are also beginning to explore how to use artificial intelligence to unlock efficiencies for patients and medical systems—a trend that we doubt will be derailed by politics.

There’s also the reality of a divided government. We have it now, and we could have it again after November’s elections. A divided government, when the President’s party doesn’t control Congress, doesn’t typically bode well for passing major new legislation—especially in an election year. It also limits the potential for budget cuts that could imperil funding for big agencies like the US Food and Drug Administration and National Institutes of Health.

Legislation Can Be a Catalyst for Healthcare Spending

But even when new legislation is passed, it isn’t always a lead weight on the healthcare sector. Consider the past couple years as an example.

The Inflation Reduction Act (IRA) of 2022 provided Medicare with newfound powers to negotiate drug prices, while capping insulin costs at $35-per-month for Medicare beneficiaries and incentivizing drug companies to put a lid on price hikes.

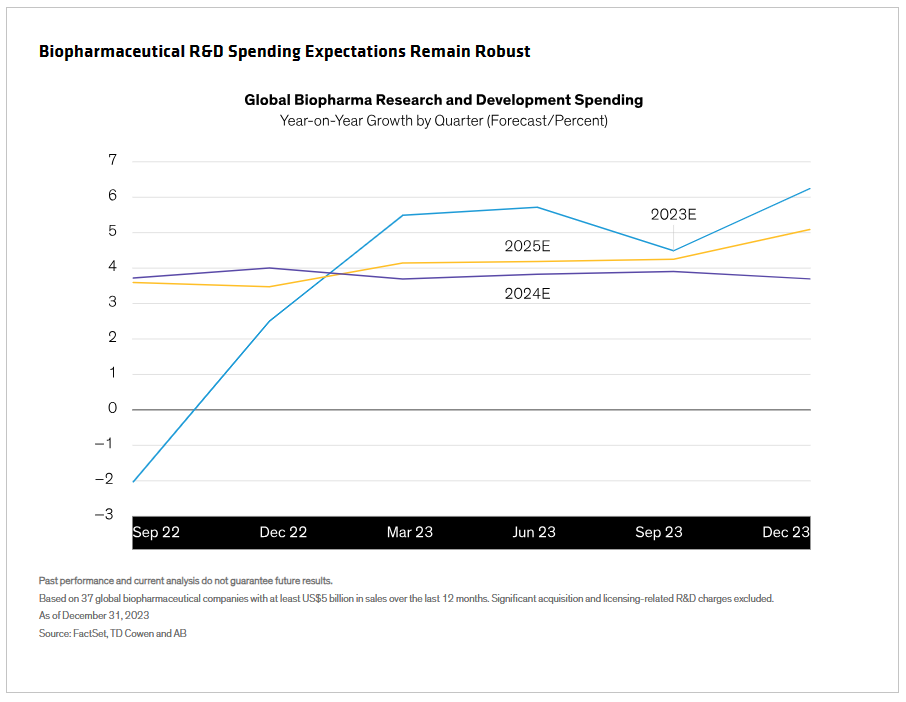

Big pharmaceutical companies initially warned that the legislation would crimp innovation. But in fact, estimates for biopharma research and development (R&D) spending point to continued robust levels of investment following passage of the IRA. R&D spending is now poised to grow at least 4%–5% over the coming years, as companies leverage advances in genomics and artificial intelligence to develop new medicines (Display).

And despite concerns about heightened anti-trust scrutiny, M&A activity in the therapeutics space has also picked up recently, with larger pharmaceutical companies acquiring smaller biotech firms to broaden product pipelines and accelerate revenue growth. This acquisition activity has bolstered funding within the biotech industry and improved investor sentiment.

Keep an Eye on Risks, but Focus on Business Models

Of course, prudent investors should be mindful of the regulatory and policy environment and factor potential policy shifts into the fundamental analysis of healthcare companies. Currently, we’re keeping an eye on the bellicose trade rhetoric between the US and China, as well as implications for biotechnology as a growing national security concern. Unresolved, both issues could lead to increased regulation and new trade restrictions. And, of course, there’s always the potential for sporadic bouts of market volatility as November draws near.

Ultimately, though, we believe investors are better off concentrating on business models rather than budget battles. By focusing on stocks with strong fundamentals, recurring revenue streams and quality growth drivers, investors can keep their healthcare allocations on course, regardless of market disruptions. Companies that aim to unlock efficiencies in healthcare systems should also be more resilient to potential healthcare reform stemming from the election.

Keep in mind, too, that within the healthcare sector, several industries trade at attractive valuations in historical perspective. When the dust settles and Congress is seated, short-term market turbulence—if it materializes—may create even more attractive buying opportunities in high-quality businesses.

The US healthcare system has survived many regime changes over the years. As November draws closer, investors shouldn’t be distracted by short-term political noise and should stay true to their long-term investment goals. Voting for select healthcare stocks in a curated equity portfolio can tap into diverse sources of return from a sector that we think has far more staying power than capricious political sentiment.

Related: European Sovereign Debt: Is the Periphery a Problem?