Trending

Written by: Mary Park Durham and Gabriela Santos

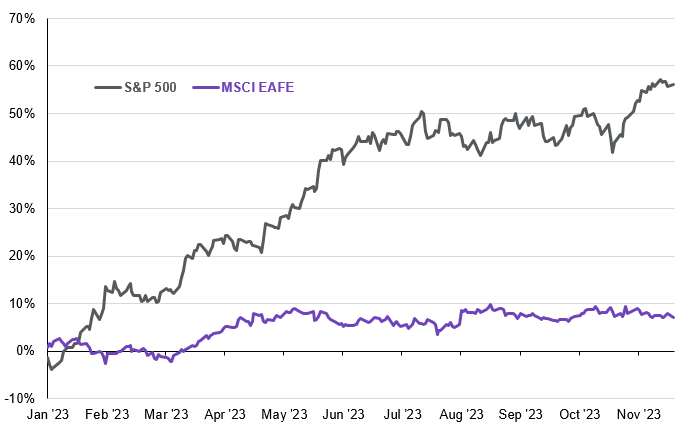

The big story for U.S. equity markets this year has been the remarkable performance of the largest seven technology stocks or the “magnificent 7.” These handful of stocks account for nearly 100% of S&P 500 YTD returns and are up over 72% this year. This has been concerning investors as it is reminiscent of the spike in internet stock valuations during the early 2000s. Is this dynamic also affecting markets outside the U.S.? Fortunately, no - performance in developed markets excluding the U.S. (the MSCI EAFE Index) has been much less concentrated year-to-date: the top 10 companies in the index are up 13.7%, while the remaining stocks are up 6.7%.

There are many reasons behind the greater breadth of returns in international developed markets:

1. More diversified sector composition: While U.S. equity markets are highly exposed to technology, international markets are more balanced and offer greater sectoral diversification. Tech stocks make up 28% of the S&P 500 while no single sector in the MSCI EAFE makes up more than 20%. The sector composition of the MSCI EAFE Index has also been improving over time and is now less concentrated in “old economy” sectors, like financials and commodities. In 2007, financials made up 23% and commodities 16% but have both decreased by 4%. Technology has nearly doubled over this time to 8%.

2. Better quality of returns: Earnings growth and dividends in the Eurozone and Japan account for over 60% of returns this year compared to only 40% in the U.S. Returns in the U.S. have been primarily driven by multiple expansion, especially due to AI enthusiasm which has caused a strong increase in valuations of tech names while the impact on earnings has yet to show up to the same extent. Europe is also seeing “growth-y” enthusiasm, benefiting a leading weight-loss drug manufacturer and luxury goods companies, but solid earnings have not been limited to a handful of themes or companies.

3. Improved profitability and shareholder returns across sectors: The end of negative interest rates in Europe and the softening of yield curve control in Japan are helping the profitability of the financial sector for the first time in many years. In addition, European banks have not faced the same issues as U.S. ones, given a more concentrated banking sector and stricter regulations. As a result, European banks are up 25% this year, while U.S. ones are down 3%. The improved profitability is not just limited to the financial sector as overall European profits have grown 51% since their post-pandemic peak, outpacing U.S. profits by 16% over the same period. In Japan, corporate governance reforms announced in April 2023 should also help EPS growth going forward. Buyback yields have stayed above 1% this year, the highest levels in decades, and the number of companies with price-to-book values below 1x has steadily decreased.

While international markets have underperformed the U.S. over the last 15 years, the path ahead is looking brighter. In addition to discounted valuations and currencies, the fundamental outlook is improving driven by higher nominal growth, higher interest rates benefiting value sectors for the first time since pre-GFC, and increased focus on returning capital to shareholders.

DM ex. U.S. equity markets returns have been less concentrated than in the U.S.

Return spread between the top 10 constituents and rest of index, YTD, price return, USD

Source: MSCI, Standard & Poor's, FactSet, J.P. Morgan Asset Management. Top 10 stocks in the S&P 500 Index include: Apple, Microsoft, Amazon, Nvidia, Google, Berkshire Hathaway, Facebook, ExxonMobil, United Healthcare and Tesla. Top 10 stocks in the MSCI EAFE Index include: Novo Nordisk, Nestle, ASML, Shell, Louis Vuitton Moet Hennessy, Novartis, Toyota, AstraZeneca, Roche, SAP, and BHP. Data are as of November 27, 2023.

Related: Does Technical Analysis Matter?