Trending

When I query my Magic 8 Ball about major financial decisions, it rarely disappoints. Frankly, the track record for correct responses stands at 80%. Not too shabby. I received a resounding YES ABSOLUTELY to the following best money ideas for 2022:

First best money idea: Fund a Roth IRA or Roth 401k.

Unless you believe your future tax burden is lower, 2022 is time to switch from the tax-deferred lane of traditional IRAs and 401ks to the tax-favored Roth IRA or Roth 401k.

Entrepreneur Peter Thiel’s Roth balance is currently the government’s unhealthy obsession. For those who have forgotten: Peter opened a Roth IRA in 1999 with roughly $2,000 and purchased 1.7 million shares of PayPal. The initial deposit is now worth over $5 billion. Keep in mind; this transaction was legal. So, Roth is bad because an individual who took the risk to create a business and thousands of jobs, enjoys massive (ultimately), tax-free growth in a Roth.

Although Mr. Thiel somehow morphed the Roth into an enemy of working-class Americans, most investors, even those in lower marginal tax brackets at retirement, can benefit from the tax-free benefits of Roth. Moreover, as readers know, RIA has been on the Roth bandwagon for years – Long before the mainstream financial media began to tout them.

Roth may not be appropriate if you believe taxes won’t be a formidable issue in the future. Anyone? Bueller?

Want greater tax control in retirement? Read on.

At the least, maintaining pre-tax, after-tax, and tax-free accounts allows for greater lifetime tax control. It’s imperative throughout the retirement income distribution phase. At RIA, we teach the importance of ‘diversification of accounts’ whereby a retiree can maintain greater distribution flexibility and control over tax liabilities when unexpected expenses arise or ordinary-income distributions risk placing a retiree in the next highest marginal tax bracket.

Most of the conventional financial wisdom that argues against Roth fails to consider taxation on Social Security benefits and the impact of additional surcharges (based on modified adjusted growth income) for Medicare Part B and D.

House legislation targets Roth.

Although there’s a negative focus on Roth from the executive branch, don’t count it out just yet. Recently, House Democrats passed a $2 trillion package that included future limitations on Roth conversions. For example, single taxpayers earning more than $400,000 and married couples earning more than $450,000 would be prevented from Roth conversions beginning in 2032.

Also, the legislation passed by the House placed a halt on mega-backdoor Roth conversions and backdoor Roth conversions overall beginning in January. However, due to stalemates, changes to the tax law for 2022 become more doubtful every day.

Roth contribution limits for 2022.

As a reminder, Roth IRA contribution limits are based on income. Contributions for single tax filers completely phase out if their earnings exceed $144,000. Married filers who earn more than $214,000 in 2022 cannot contribute to Roth. A taxpayer can contribute $6,000 to a Roth IRA in 2022. For those 50 and older, add another $1,000 in catch-up contribution.

Roth 401ks work like traditional 401ks. The difference is employees contribute on an after-tax basis. Employer matching contributions remain tax-deferred. For 2022, an employee may contribute $20,500 to a 401k. Those 50 and older can add another $6,500.

Funding a Roth to the max is my personal favorite on the list of the five best money ideas for 2022. So much so I make sure my daughter auto-contributes monthly to hers and will continue to do so in the new year.

Second best money idea: Make your emergency cash work harder.

The Fed will probably raise short-term interest rates next year. The CME Fedwatch tool shows a 94.6% probability that the Federal funds rate will be 50 bps higher in December 2022.

Generally, depositors see rates increase for money market and savings accounts along with CDs soon after the Fed moves. But is this the case? After the Fed takes action, brick and mortar banks no longer seek to benefit savers by increasing rates. They’re sitting on enough cash already so they don’t need to pay depositors more for parking cash. However, virtual banks are quick to increase what savers earn! So, why wouldn’t a consumer explore cash maximization options with FDIC-insured virtual banks?

Forget on line and go online.

When did you last wait in line at a bank? I maintain my checking and savings with an online institution. For example, Marcus Bank, backed by Goldman Sachs, offers high-yield savings, checking accounts, and CDs. Their rates on savings are currently four times the national average. In addition, there are many FDIC-insured choices such as Ally and Synchrony.

If indeed earmarked for emergencies or a financial vulnerability cushion, avoid the temptation to transfer cash to risky investments. RIA defines an FVC as an additional six months of cash reserves set aside for expenses such as a job loss.

Already I’m reading mainstream financial media articles about how cash is trash and pulverized by inflation. While it’s true that cash doesn’t keep up with inflation, it provides benefits in the form of liquidity and stability. In addition, cash on hand can reduce the use of high-interest credit cards to cover emergency expenses.

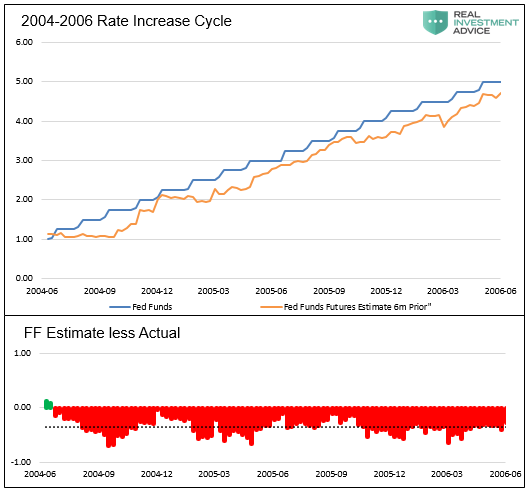

My thought is to stick with high-yield savings for now and avoid CDs. Then, by mid-2022, look to investigate a CD ladder, especially when there is clearer Fed policy visibility. Per Michael Lebowitz, the market consistently underestimates the number of times the Fed hikes the Fed Funds rate. As a result, consumers in online banks may benefit quickly from rising rates on savings and money market accounts.

In the chart below, Michael (data courtesy of Bloomberg) outlines how the market underestimated (red bars) the pace of Fed Funds rate increases for the 2004-2006 rate hike cycle.

Making your cash work harder is another of the best money ideas for 2022. The Fed may make cash more desirable to hold in the new year.

Third best money idea for 2022: Take on a health regimen, pay for and stick with it.

Health and wealth are connected. Whether a gym membership or increased food and lifestyle expenses, long-term investing in health has a high return on investment. Don’t feel guilty for spending on a treadmill if you’re going to use it consistently!

When people cut expenses, gym memberships are always one of the top three categories on their chopping blocks. Seemingly, I add it back to the budget!

Most likely, if you’re a good steward of financial health, you’re also proactive when it comes to maintaining your financial health. A study from 2014 in the Journal of Psychological Science titled Healthy, Wealthy and Wise: Retirement Planning Predicts Employee Health Improvements by Timothy Gubler and Lamar Pierce outlines how the same underlying psychological factors drive poor physical and financial health.

People who save for their future also make smart choices to improve and maintain their health.

From the authors in the study’s abstract:

We found that existing retirement-contribution patterns and future health improvements were highly correlated. For example, employees who saved for the future by contributing to a 401(k) showed improvements in their abnormal blood-test results and health behaviors approximately 27% more often than noncontributors did.

According to the Fidelity Retiree Health Care Cost Estimate, an average retired couple age 65 in 2021 may require $300,000 saved (after tax) to cover health care expenses in retirement. Healthcare is expensive enough for healthy individuals. And thankfully, Medicare expenses are easily accounted for in financial plans and make healthcare expenses more manageable.

However, my analysis shows that unhealthy retirees can suffer from significant out-of-pocket costs. Sometimes in the range of 20-50% higher for expenses outside of what Medicare covers.

Think of wellness expenses as one of the best money ideas for 2022 and forever.

Wellness costs can seem unnecessary. However, good health has a long-term benefit that can make for a wealthier and more satisfying retirement. Usually, I recommend clients add a separate spending category for wellness expenses. In my budget, I reduced discretionary items such as eating out. I add spending for membership to Orange Theory fitness, purchasing fresh foods, and an auto-subscription for vitamins, including D3.

The health-wealth connection is not only one of the five best money ideas for 2022. Good health is one of the best money ideas for the rest of your life!

Fourth best money idea for 2022: Prepare your portfolio for rising interest rates.

Inflation is a concern, although the Fed has denied its lingering impact. I think the rate of change for inflation will begin to slow soon. However, the Fed benchmark of 2 percent is going to be history. Perhaps the new standard is 2.5 percent. Frankly, nobody knows, and the Fed is more in the dark than most of us!

The Atlanta Fed’s sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly—increased 4.0 percent (on an annualized basis) in November, following a 5.9 percent increase in October. On a year-over-year basis, the series is up 3.4 percent. So, once supply chain issues subside, yes, the heat of inflation will cool off too. But, sticky prices well, don’t get unstuck quickly. Their prices are slow to move. Thus, the Fed will most likely need to move quickly to increase rates, and that action will be highly disruptive to stocks.

Next year could be a nail-biter for investors.

First, in 2022 investor emotions will be an obstacle to portfolio performance. After a decade of Fed market bailouts and buying the dip, stocks will suffer from easy money detoxification, and investors will too. The shift from overconfidence to trepidation should couple with a market focused on sluggish economic growth and higher than expected inflation along with minimal support from the Federal Reserve. The RIA investment team has discussed and planned for the headwinds we envision for the new year.

Second, I believe stocks will continue to be one of the five best money ideas for 2022 but look for volatility to shake out many easy money momentum traders and weaker holders of stocks. Thankfully, RIA’s risk management rules have been effective. We’ve trimmed profits, sold losers, and added to winners on weakness. Next year, I suspect risk management will take on significant meaning as the Fed not only tapers but increases the Fed Funds rate faster than anticipated.

Prepare for rising interest rates and sustained higher inflation.

Third, to prepare for rising interest rates, an investor should look closer at sectors that, at the least, may hold up better in erratic markets—for example, consumer staples. Also, financial stocks could prosper if the Fed raises its benchmark rate. Banks significantly benefit from even small increases in interest rates as immediately they’ll charge more on loans. Also, sustained inflation can make energy and materials worth further analysis in 2022.

Ultimately, the game of chicken between the Fed and inflation should have most investors on the edge of their seats in 2022.

Last and most important, investors will find themselves grappling with unfamiliar market tailwinds. As a result, stock investors should become reacquainted with how much portfolio risk they’re willing to tolerate.

Fifth best money idea for 2022: Expand your definition of financial vulnerability.

A Financial Vulnerability Cushion is one thing. A Financial Vulnerability Assessment is the next level of household financial protection. Never forget, your net worth is under constant attack from issues beyond your control. Wealthy households must mitigate liability issues through adequate insurance coverage that protects a home from predatory litigators. Unfortunately, many homeowners forgo umbrella liability coverage which is a mistake.

Most of the time, home and auto owners obtain just enough liability coverage to pass state and loan requirements. However, households with robust net worth statements will look to cover up to the maximum limits of these policies and then wrap the policies in umbrella coverage. Consider the additional insurance more like a blanket that protects your wealth from outside sources who want a piece of your net worth! Umbrella insurance is relatively inexpensive – $200 to $300 annually on average.

Do some homework – examine and increase liability coverage. The first step is to review or have a professional help you go over your policy declarations. For example, Texas law requires drivers to have at least $30,000 of coverage for injuries per person, up to a total of $60,000 per accident, and $25,000 of coverage for property damage. This is called 30/60/25 coverage. I maintain $100,000, $300,000, $100,000 or 100/300/100. Also, I max out uninsured motorist coverage as Houston is replete with uninsured drivers.

One of the best money ideas for 2022 is to protect what you own!

In 2022, you’ll be hearing a lot about FVAs or Financial Vulnerability Assessments from RIA as we roll out a robust financial literacy initiative to help everyone in your family become financially empowered. Look for short videos, writings, and Candid Coffees designed to support this passionate cause.