Trending

Written by: Jordan Jackson

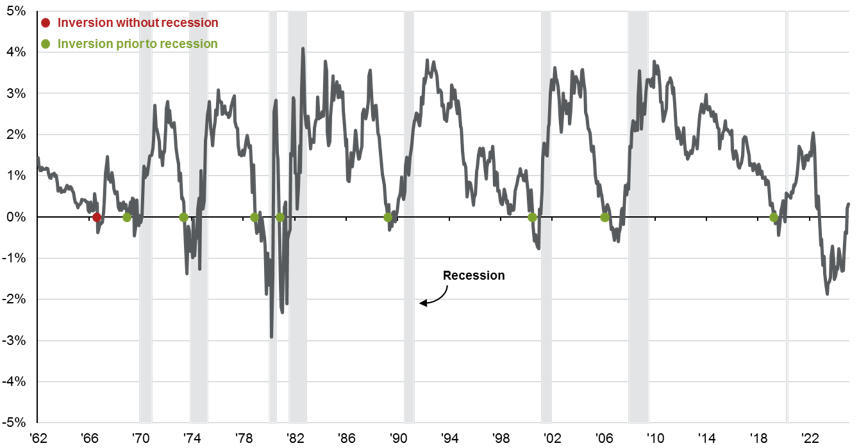

The spread between the 3-month U.S. Treasury bill yield and the 10-year U.S. Treasury yield, commonly referred to as the yield curve spread, is a vital indicator in financial markets and is closely monitored by investors and the Federal Reserve, particularly given the historical efficacy of its inversion predicting U.S. recessions. An inversion signals that markets believe current policy may be too restrictive, potentially triggering an economic slowdown. Indeed, since 1960, the spread between the 3-month and 10-year Treasury yield has inverted before every U.S. recession, making it one of the most reliable indicators of economic downturns. There has only been one instance where this spread inverted and a recession did not follow, or “false positive”—in 1966. With so few false positives, investors are still cautious around the general rosy economic outlook for 2025 following the prolonged inversion over the last couple of years.

The Federal Reserve’s aggressive rate hikes to combat inflation pushed short term yields higher and caused the curve to first invert in October 2022, and the curve remained inverted until December 2024. However, while this has been the longest inversion in recent history, a recession has yet to materialize. That said, the recent steepening and un-inverting in the curve provide key reasons as to why the inversion may not signal a recession:

- While the Fed typically cuts rates in response to weakening economic conditions, the Fed is already well underway in its cutting cycle while growth has remained resilient reducing restriction on the economy.

- Stronger-than-expected economic data such as robust labor markets, consumer spending, business investment and industrial production indicate the economy is likely to remain on solid footing.

- The economy has shown it can withstand higher policy rates and estimates of r-star or neutral rate in the economy have been rising suggesting markets may have been mispricing long-term rates too low.

The spread between the 3-month and 10-year Treasury yields remains a critical economic indicator. Its current positive slope suggests optimism about a soft landing—where inflation continues to moderate without a severe economic downturn. However, it’s important to recognize that while the indicator has an impressive track record, no single economic metric is infallible. However, time will tell; the last four cycles saw the curve un-invert on average six months prior to a recession. This is why investors should consider yield curve inversions alongside other economic indicators to gauge the likelihood of a recession.

U.S. yield curve steepness

Difference between 10-year and 3-month U.S. Treasuries*

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management. In December 2024, the yield curve un-inverted after being inverted for 25 consecutive months.

Data are as of December 31, 2024.