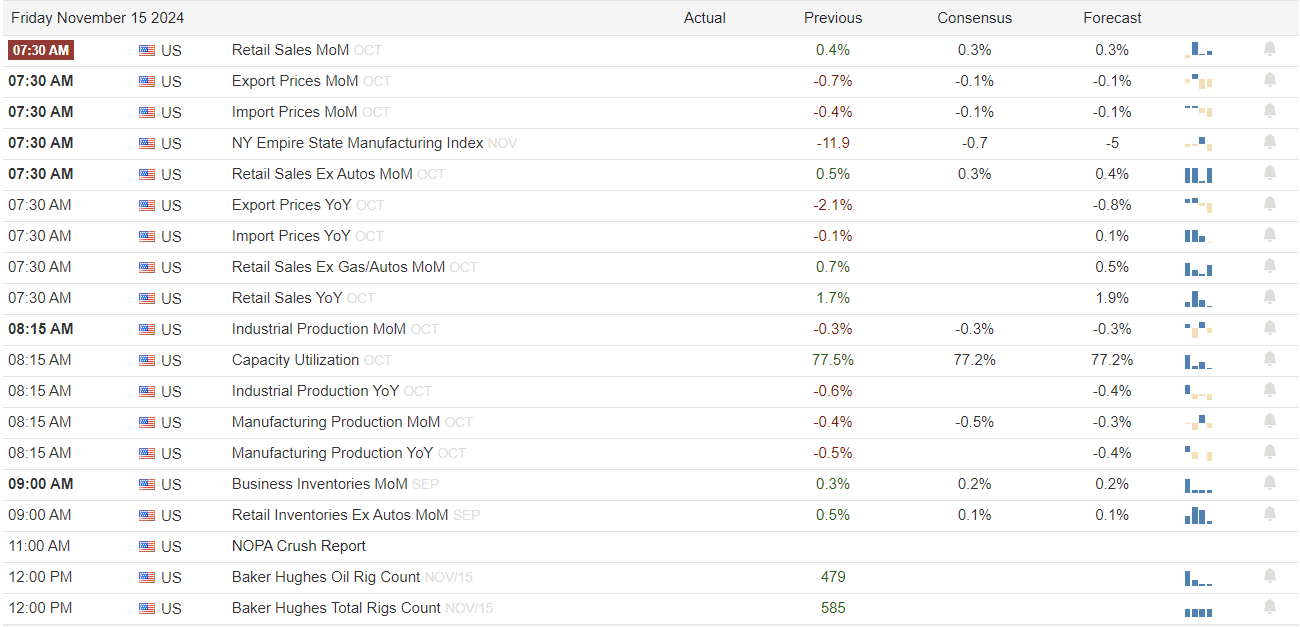

Trending

2% CPI is a headline you won’t find in today’s Wall Street Journal. The reason is that official inflation gauges, such as CPI, are in the mid to upper 2% range. Last Wednesday, for instance, the year-over-year CPI rate clocked in at 2.6%. We claim inflation is at 2% because we know that 40% of the CPI data considerably lags behind market prices and is, therefore, inaccurate. In particular, the shelter component of CPI, accounting for 40% of CPI, measuring rental prices and imputed rents, has been running close to 5% annually. Zillow, Redfin, and a host of other firms in the rental industry have been reporting that rental prices have not increased for the last year and a half. Consider the following from Redfin:

The nationwide median asking rent was $1,647 in July, down $53 from the all-time high in 2022.

Rents for 3+ bedroom apartments fell the fastest, dropping 2.4% year over year.

We could provide more data showing near-zero inflation in rental prices, thus justifying that CPI is likely 2%. However, what may be more critical is where market rental prices are headed. The graph and commentary below, courtesy of Rick Palacios Jr., warn that rent prices may start falling as existing home sale listings rise. Furthermore, if mortgage rates head lower, the number of existing homes for sale will likely increase, further pressuring rent prices.

For-sale housing supply trends are key leading indicators to watch for the single-family rental (SFR) industry, as there’s an inverse relationship between for-sale listings and SFR occupancy (see chart below).

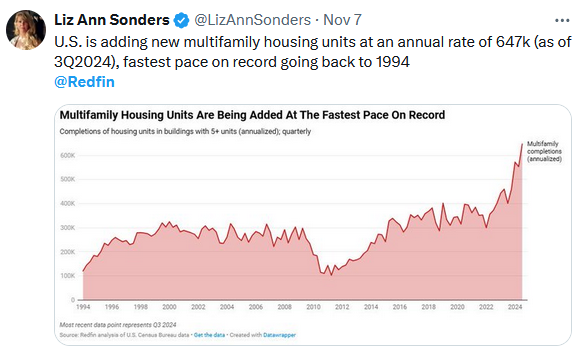

Check out our Tweet of the Day below. It shows that the multifamily supply is increasing rapidly, another factor that will present a headwind to rental prices. Accordingly, when the CPI data catches up with reality, we will likely find that CPI runs at 2% or even lower.

What To Watch

Economy

Market Trading Update

As discussed previously, professional investors are underweighted equity risk heading into year-end. That, along with $6 billion daily in corporate share buybacks, continues to put a bid under the market. However, in the short-term, the market is overbought and extended from the 50-DMA, so the recent pause was not unexpected, particularly heading into a holiday-shortened trading week.

With CPI and PPI now behind us, today’s retail sales report will be the next critical piece of economic news to drive the market. Credit card delinquencies continue to rise at the highest level in over a decade, but consumers have continued to “show up” month after month. It is worth noting that retail sales make up approximately 40% of PCE, which comprises 70% of GDP. Therefore, watching the retail consumer is very important to future corporate earnings and profits outlooks.

Technically, there is nothing wrong with the market. Yes, it is currently overbought, but the recent “choppy” action is beginning to work off some of that condition. I would expect a continuation of choppy performance into Thanksgiving, with a pop into the first week of December. That pop will be met by additional selling as mutual funds make their annual distributions, setting the market up for the year-end “Santa Claus” rally as managers window-dress for year-end reporting. In short, the trend is higher into year-end, but expect some bumps along the way.

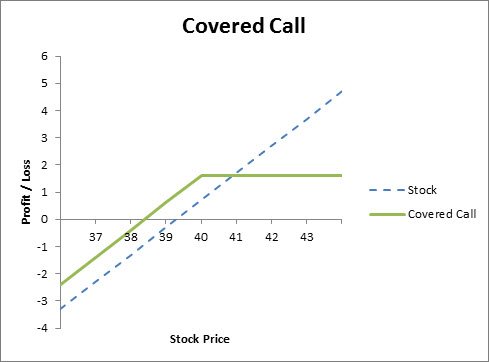

Can Covered Call ETFs Protect You?

We recently received the question below about option strategy ETFs. Accordingly, let’s examine JP Morgan’s Equity Premium Income ETF (JEPI) and answer the question.

The ETF (JEPI) offers an attractive yield, but how will it behave during more volatile market periods? If we do enter more volatile periods, will these strategies continue to generate a reliable stream of income?

Some investors use options with traditional stock portfolios to hedge risks, enhance upside performance, or generate income. JEPI is a covered call ETF strategy designed to participate in the market upside and create additional income beyond dividend payments. The ETF invests in U.S. large-cap stocks and then writes (sells) call options against those positions to generate income. Additionally, the fund reduces risk and upside by having a beta of .50. Thus, its stocks should be half as volatile as the S&P 500. We share the graph below courtesy of Fidelity to show how a covered call strategy works.

The income from writing calls will boost returns above the S&P 500 in all negative and smaller positive market return scenarios. However, the calls limit gains beyond the strike prices of the options. Thus, the performance flattens out as the market moves higher. Furthermore, the beta of .50 should cut the potential upside in half, but it will also cut the downside risk in half.

The simple answer is that the JEPI strategy is defensive primarily because it has a beta of .5. While it does provide extra income and will in a drawdown, it comes at the expense of reduced capital gains.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Harnessing Momentum: Understanding the MACD Indicator