Trending

Written by: Marc Ado | Swan Global Investing

Assessing the Current Market Conditions

It’s been a year since the market bottomed out during the COVID-19 sell-off. The 33.8% drop in the S&P 500 brought to a sudden end one of the longest bull markets in history. But as the dust has settled and the markets have returned to all-time highs, many people were left wondering: was that really a bear market?

On one hand, the COVID sell-off met the strict definition of a bear market, that is, losses in excess of 20%. On the other hand, the suddenness of the sell-off and the rapidity of the recovery has led to a counter argument, that this was more of an extreme correction rather than a true bear market.

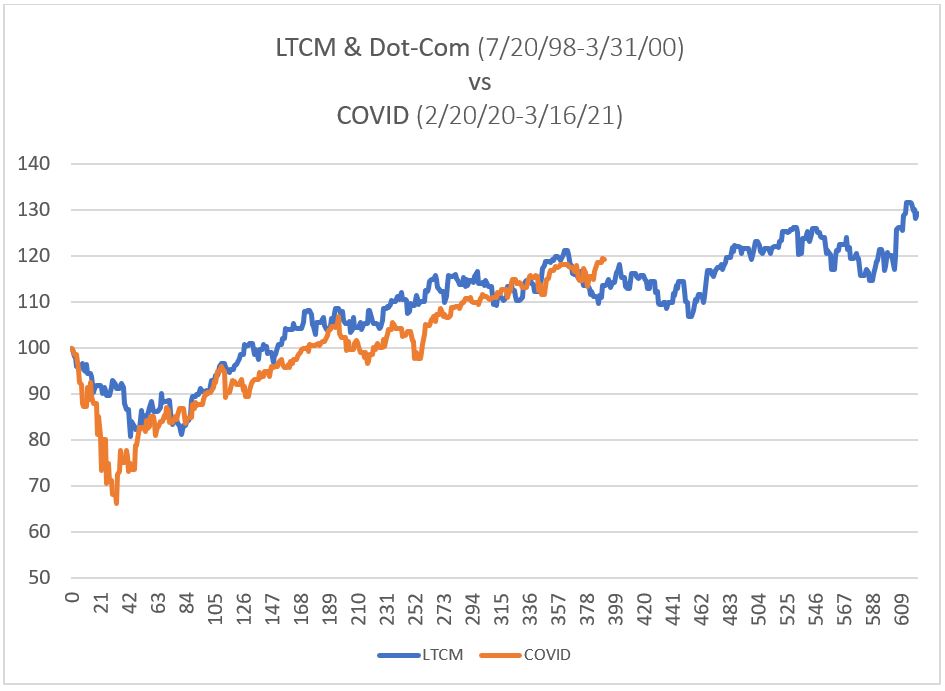

The massive COVID-19 sell-off and subsequent rebound of 2020 was unprecedented:

- Fastest sell-off from market highs: -33.8% in just 33 days

- Largest and fastest recovery: +51.2% in 140 days

- Volatility closed at an all-time high of 82.7 on March 16th

That said, if I were to look for a historical comparison, I would find the closest parallel in the 1998-99 period.

- During the Long-Term Capital Management crisis, markets rapidly sold off by -19.8% over 43 days, narrowly missing a bear market

- The Federal Reserve organized a bailout in order to keep markets liquid

- Markets rallied and recovered all of their losses 84 days later

- Markets continued to run through 1999, ending the year up 56.2% off of the market lows of 8/31/98

Beyond the numbers, there are other parallels between 1998/99 and 2020/21:

- The first and most obvious is that the market gains were led by the mega-cap technology names typified by the NASDAQ. The narrative then and now was that the economy was being radically restructured due to the impact of the internet on all aspects of society

- Value stocks trailed badly in both environments. Although value stocks have staged a recent rally in 2021, in 2020 it was all growth stocks.

- An element of existential dread hung over the globe. Today it is COVID-19, twenty years ago it was Y2K.

- In both periods we had a tightly contested and bitterly divided political environment with a contested election

- Twenty years ago there was deafening hype surrounding no-earnings dot-com stocks, whose boosters claimed we were in a “new paradigm” and old valuation metrics did not matter. Today the hype machine is focused on crypto-currency and non-fungible tokens, where the same earnings and valuations criticisms apply.

This late-90’s period was known at the time of “Irrational Exuberance.” Although then-Fed Chairman Alan Greenspan first used the phrase in December 1996, the bubble continued to form for several more years, brushing off the near-miss bear market of August 1998.

Students of history know what happens next: the long bear market of 2000-2002.

While the Dot-com bubble burst in March 2000, this period was marked by other calamities and challenges. The terrorist attacks of September 11th and the accounting scandals of Enron, Tyco, and WorldCom led to an extended drawdown. The S&P 500 drew down by almost 45% and did not recover its losses until October 2006. Meanwhile, the NASDAQ lost nearly three-quarters of its value and did not fully recover until December 2013, almost a decade and a half later.

That was a true bear market.

While there are many similarities between the 1999 period and today, there is one large difference. The markets entered the new millennium with yields at comfortable levels. The 10-year Treasury was around 6.5% on January 1st, 2000. This had several benefits to diversified investors:

- The Fed had a lot of room to maneuver and was able to lower yields, providing a helping hand to the economy;

- Falling yields provided a boost in the value of bonds. The Barclays (or Lehman Brothers) U.S. Aggregate Bond index was up 33.5% during the first three years of the 2000’s, helping offset the losses seen in equities.

Today, in stark contrast to the 2000’s, yields on the U.S. 10 year Treasury Note are a paltry 1.6%. It is highly unlikely bonds will be able to provide those levels of positive returns should we face a true bear market again.

Investors currently find themselves faced with unpleasant realities and challenges. Some are familiar, as the equity market today resembles that of the Irrational Exuberance period. Other challenges are new, like the doubt surrounding bonds being able to perform their traditional protection role.

Swan believes that this widespread uncertainty requires new thinking. Our “always invested, always hedged” approach was designed to navigate such treacherous waters. In fact, Randy Swan created the Defined Risk Strategy all the way back in 1997, when his concerns about market valuations and irrational exuberance led him to create a hedged equity strategy that would hedge the gains he made in the bull market.

Today many investors face a similar conundrum: how does one participate in equity markets gains, yet defend against potential losses? We believe that hedged equity as a strategic investment approach is more relevant than ever.