Trending

Written by: David Waddell | Waddell and Associates

THE BOTTOM LINE:

Markets continued their record run as last week’s rate cut and expectations of another of similar magnitude, further buoyed investor sentiment. But China gets the nod as this week’s rally champion with the announcement of sizable stimulus measures aimed at defibrillating the Chinese economy. Given China’s economic size, stimulus there amounts to stimulus everywhere. Radiating outward, the Chinese market (ETF: FXI) rallied 18%, international markets outside the US (ETF: CWI) rallied 3%, and the USA itself (ETF: SPY) rallied .62% on the week. Politicians may not like China, but clearly investors should this week for keeping this rally aloft. Thanks, China!

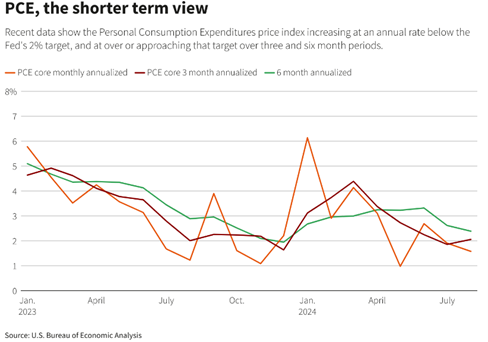

This week marked a continuation of the current stock market rally into record territory. Jerome Powell’s bold .50% rate cut boosted markets last week and gained further validation on Friday as the Bureau of Economic Analysis reported annual inflation of just 2.2% across the US economy. Nearer-term measures add even further validation that Jerome cut correctly:

The Fed will meet again a mere 40 days from today and futures markets place a 53% probability of another .50% cut. We continue to favor bold action from the Fed, as will the markets, but this week’s boost came from offshore. China unleashed a cornucopia of stimulus to jumpstart their sagging economy.

Before we get to the specifics and implications, let’s revisit some rules of thumb when considering China. First, the #1 goal of the Communist Party in China is to stay in power. There are 1.4 billion Chinese citizens. Rising prosperity leads to rising political opinion. This has been the grand bargain between the Party and the people. Falling prosperity invites political scrutiny and rising civil unrest. China spends more on domestic security than national defense, indicating that the Party sees the larger existential threat inside its borders, not outside. For this reason, economic growth is a matter of self-preservation.

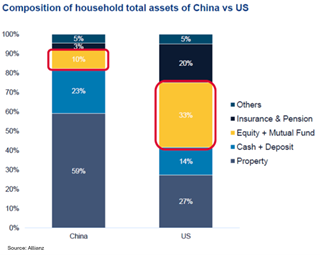

Unfortunately, the Chinese economic model needs restructuring away from state-owned build and export to privately-owned serve and consume. Rapid urbanization powered the domestic economy for decades, but structural overcapacity has led to deflating property values and defaulting developers. Consider the composition of Chinese household balance sheets vs. US household balance sheets:

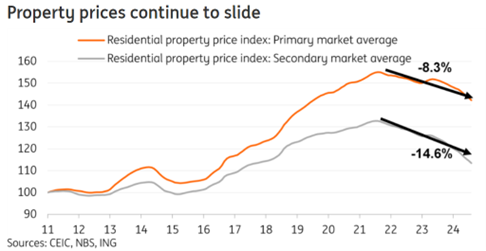

US households have 27% of their net worth tied up in property, while Chinese households have 59% of their net worth tied up in property. Now look at recent property price trends:

In sum, the world’s largest population has the largest portion of household assets in depreciating real estate assets, leading to a record low in consumer sentiment measures, and heightened political concerns within the Chinese Communist Party. Cue the stimulus!

(I asked Matt Gentzkow, an investment strategist within W&A, to write me an internal memo on the Chinese stimulus announcement and found it so well done that I have included it verbatim below. Well done, Matt!)

What is going on in China?

“If you’ve got a bazooka, and people know you’ve got it, you may not have to take it out.” – US Treasury Secretary Hank Paulson, July 2008

While Jerome Powell started the US rate cut regime last week to steer the US economy towards a successful ‘soft landing,’ the Chinese economy has already crash-landed, and their government is using its tools to stimulate a deteriorating economy. This week, China announced a fiscal stimulus of 2 trillion Yuan (or ~ USD 285 billion) aimed at increasing consumer consumption and helping local municipalities reduce debt load while also reducing reserve requirements for banks by 0.5% to encourage lending. In theory, this allows banks to lend more to consumers who use that money to buy goods or assets, boosting GDP.

Immediately following these emergency policy measures, the government signaled further fiscal support through unnamed government sources and various US media outlets. This reminds me of the quote above, when amidst the 2008 Global Financial Crisis, then US Treasury Secretary (and former Goldman Sachs CEO) Hank Paulson hoped that signaling of drastic fiscal measures would help calm market participants. Of course, we know from history that Hank Paulson ultimately did take out his bazooka to save the US economy.

What do the markets think?

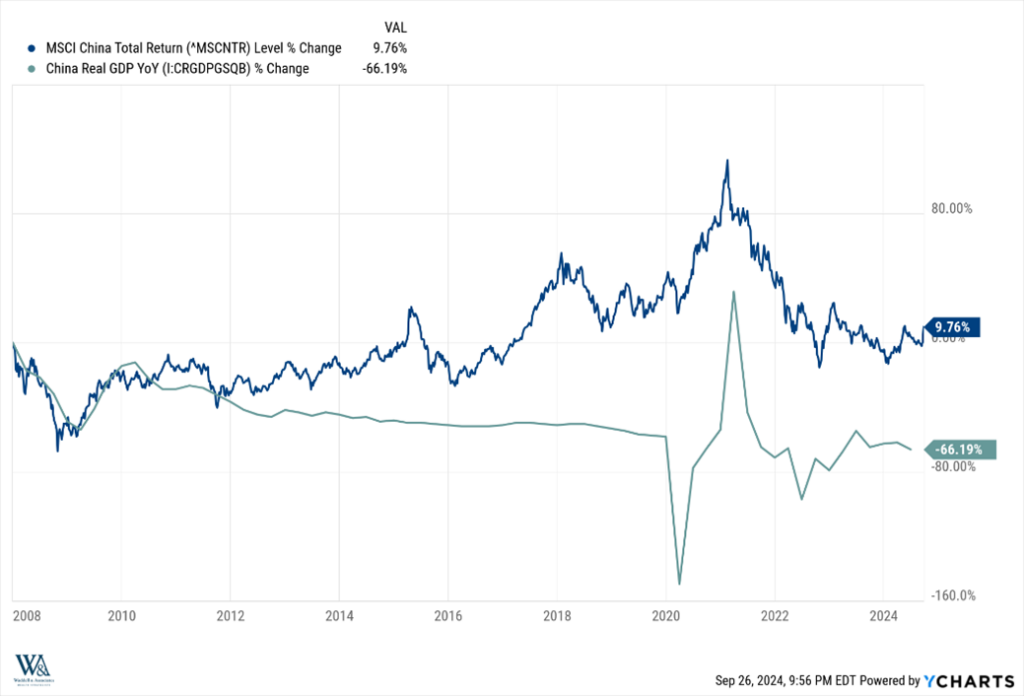

Well, the good news: The Chinese stock market (measured by the Shanghai Composite Index) has rallied over 12% this week on the stimulus news. But what does this mean for investors going forward? An accommodative fiscal policy will certainly help the Chinese economy and asset prices, but we also need to remember that publicly traded equity markets like when economic growth is positive and accelerating.

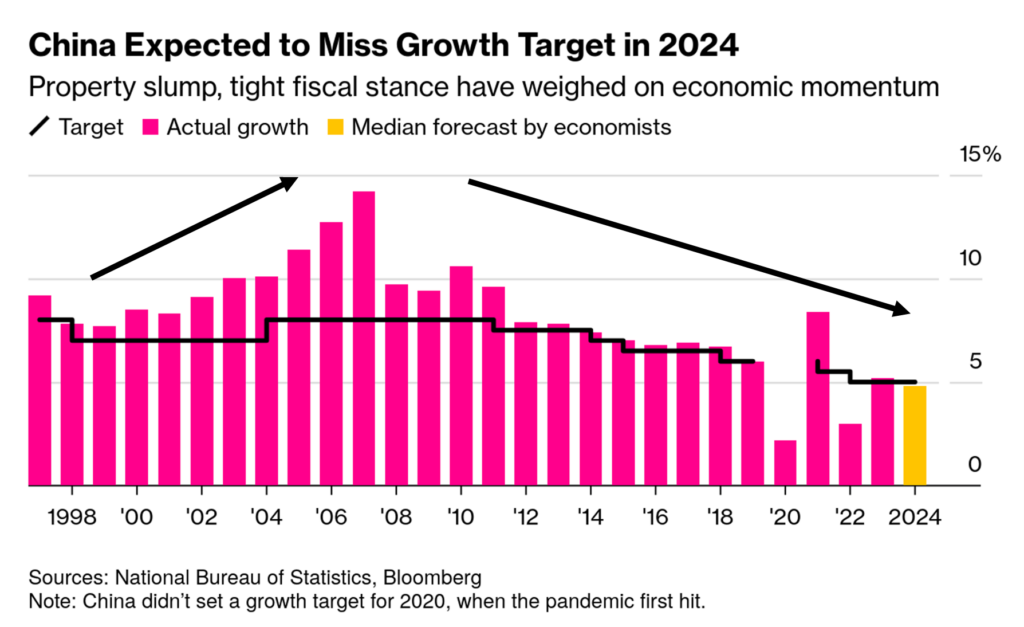

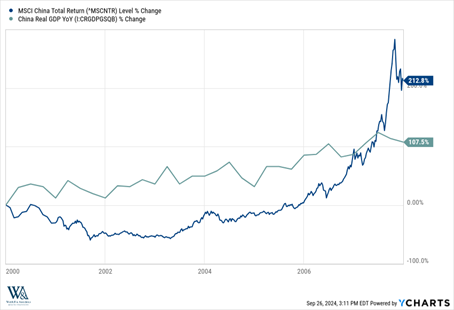

For example, peek at the chart above. From 2000 through 2007, China’s reported GDP was positive and accelerating in rate of change terms. Not surprisingly, the MSCI China Total Return Index was up 212% over the same time frame!

However, GDP growth has been mostly decelerating in rate of change terms since 2008, which has corresponded to a paltry 9.76% total return since 2008.

For the first part of the 21st century, China was a wonderful growth story, and investors were paid handsome returns; however, as economic growth rates have slowed, so have local equity markets. China has been easing economic conditions now for a few years post Covid-19 pandemic, but they have no choice but to bring out the ‘bazooka’ in months to come as they attempt to re-ignite an acceleration in economic growth and lift asset prices.

Sources: U.S. Bureau of Economic Analysis, Allianz, CEIC, NBS ING, Y Charts, National Bureau of Statistics, Bloomberg

Related: Is a Soft Landing Possible Amidst a Crumbling Economic Landscape?