Trending

2021 isn’t over yet. So here are 10 smart money moves to make right now.

Saving money should be a year-round endeavor, but life gets in the way just like anything else. So with 2021 coming to a swift, thankful end, take advantage of the fourth quarter to accelerate your financial acumen, bolster your balance sheet and successfully springboard into the new year.

Tip One: Max Out HSA Contributions for 2021.

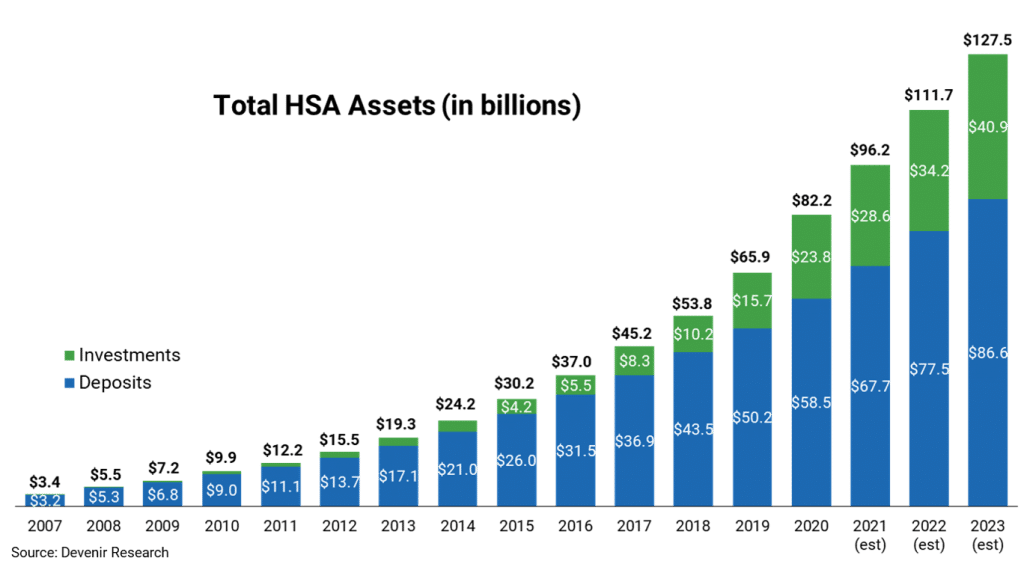

A Health Savings Account is a pre-tax savings miracle account. What other vehicle allows investors to sock money away triple tax-free? There’s no doubt HSAs have caught on with investors. According to Devenir’s latest survey, a national leader of investment solutions for Health Savings Accounts, the number of HSAs has now exceeded 30 million.

The popularity of HSAs makes sense since these vehicles link to high-deductible healthcare plans. High deductible plans lead to lower costs for employers and a more significant share of the expense burden taken on by employees.

HSA Changes For 2022.

Also, for 2022, the IRS defines a high deductible health plan as any plan with a deductible of at least $1,400 for an individual or $2,800 for a family. Thus, an HDHP’s total yearly out-of-pocket expenses (including deductibles, copayments, and coinsurance) can’t be more than $7,050 for an individual or $14,100 for a family. (This limit doesn’t apply to out-of-network services.)

Not all HDHPs qualify for HSAs, but most employers seek to add qualifying plans to their benefits enrollment packages.

HSA contribution limits for this year are $3,600 for individuals, $7,200 for families. Both have a catch-up contribution of $1,000 for employees 55 or older.

RIA’s Recommendation for HSA Distributions.

Most financial professionals recommend HSAs as a vehicle to pay for qualified healthcare expenses 100% tax-free. While this is a valid use, at RIA, we recommend that employees treat HSAs as healthcare retirement savings accounts. In other words, we suggest that employees allow their contributions to accumulate in the HSAs and distribute later for healthcare expenses in retirement. In addition, health Savings Accounts contain multiple mutual fund selections for long-term investment.

According to IRS Publication 969, HSA distributions can be used to pay Medicare premiums (all except Medigap) and long-term care insurance premiums limited to a specific dollar amount by age. For example, older Americans aged 61-70 can use up to $4,520 of HSA distributions to pay long-term care insurance premiums in 2021.

Money Tip Two: Replenish Your Financial Vulnerability Cushion.

Readers may recall how at RIA, we recommend households maintain an FVC. The first six months of living expenses are an adequate emergency reserve for unexpected expenditures such as fixing an air conditioner or auto repair. However, we suggest an additional six months of savings in the case of a significant life event, extended unemployment, or other outliers that can place households in financial jeopardy.

A couple of years ago, we began discussing the FVC on the radio and discovered that listeners or clients who took our advice faired well through pandemic conditions. In addition, several who reached out told us how maintaining an FVC through COVID lockdown, and job loss helped them think clearly about their next steps.

Also, we recommend savers use FDIC-insured online banks such as Marcus, Synchrony, and Ally, to hold emergency funds and FVCs. These banks have less overhead; thus, their rates will always be more attractive relative to brick and mortar brethren.

Money Tip Three: Consider A Surgical Roth Conversion.

At our Retirement Right Lane Class, we discuss the importance of the diversification of accounts. Account diversification includes pre-tax, after-tax, and tax-free investment accounts, including Roth. Multiple accounts taxed differently allow for the crafting of a tax-effective retirement income strategy.

Mainstream financial media generally casts magical pixie dust exclusively upon tax-deferred accounts. And although they have a place, there’s nothing magical about them. Eventually, investors will pay the taxman in retirement. No problem, right? The conventional wisdom is most of us will fall into the lowest tax bracket when we retire. Valid in the 1990s. Not so much today.

Retirees should focus on marginal tax rates or the tax rate on the next dollar of ordinary income. When most of a retiree’s investments are in pre-tax accounts and distributions taxed as ordinary income, they are at risk of higher marginal tax rates due to taxation of Social Security benefits and the charges that trigger Medicare Income-Related Income Adjusted Amounts or IRMAA that increase Medicare Part B and D premiums. This holistic view of taxation is beyond the purview of this blog post, but we often write specifically about this topic.

Retirees Can Still Consider Surgical Roth Conversions!

With Social Security and IRMAA as part of the mix, retirees should work with a skilled financial partner to discover if surgical Roth conversions fit into their withdrawal plan. Even retirees taking required minimum distributions may benefit from surgically converting IRA assets to Roth up to the next marginal tax rate.

Young investors benefit from funding multiple account types, especially Roth. They may look to convert IRA assets to Roth surgically, consider Roth IRAs if they meet adjusted gross income requirements, or fund Roth 401k instead of traditional 401k accounts.

Roth contributions for this year are $6,000 with a $1,000 catch-up provision if 50 or older. Unfortunately, contributions are limited depending on a household’s modified adjusted gross income. Click here to determine your contribution limits based on income. Roth 401k contribution limits are the same as traditional 401k limits. For this year, the elective deferral limit is $19,500, with an additional catch-up amount of $6,500 for participants 50 or older.

Remember, there are no income limitations for the conversion of traditional IRA assets to Roth.

Overall, funding a Roth strategy through contributions or conversions is one of the 10 smart money moves to make right now.

Tip Four: Drain Your Flexible Spending Account.

A Flexible Spending Account differs from a Health Savings Account. FSAs must be used within a specific period, usually year-end. HSAs are not subject to a similar mandate. Think of FSAs as use it or lose it, and HSAs as don’t use it and grow it.

FSA distributions are tax-free and can be utilized for a wide variety of health-related expenses. Consumers can find an extensive list at healthcare.gov.

The maximum FSA contribution will be $2,750. Often, contributors max out these benefits. Then, they get caught in a frenzy to spend down balances in the time allotted. Keep in mind that some employers grant additional time to drain FSAs, usually the first three months of the new year. However, for most plans, FSAs must be exhausted by the end of the year, or you risk losing the remaining funds.

Now is an excellent time to crystalize your health-related spending needs for 2022. The FSA is not an account to overfund. If anything, I’d look to underfund a bit to make sure I spend the FSA dollars earlier in the year. So take an accounting of your medical expenditures this year and fine-tune next year’s contributions.

Tip Five: Rebalance Your Portfolios.

If you haven’t taken profits this year, now is the time. This tip may be one of the most important 10 smart money moves to make right now. When markets consistently move higher, investors get complacent. Now that we’ve hit a patch of volatility on the investment road, investors are taking notice, and that’s a good thing.

An astute investor rebalances by trimming profits from best-producing investments and reallocating to lesser performers as a method to manage risk. It sounds so counterintuitive, and an old market adage is to let stock winners run. However, taking profits from hot investments to reallocate to cooler ones places investors in command of their fate. In other words, eventually, the market will cool down the winners, so why not be the one to do it first and from a position of strength and control?

At RIA, we let winning investments do what they do best; but our team places what I call ‘rebalancing reins’ or tolerance bands around each position that alert us when to trim outperformers (not sell them altogether). In addition, we monitor underperforming positions to either add to them or ultimately sell them.

Let Us Help With Your Rebalancing Decisions.

I don’t expect you to be as intricate. And transaction costs along with your risk tolerance must be part of the equation. So, naturally, our team is happy to take the rebalancing decision off your busy plate. However, if you decide to do it yourself, I recommend checking out Lance’s 401k Plan Manager. If you’re self-managing non-retirement assets, spend some time with Lance’s newsletter or sign up for our monthly subscriber service RIA Pro.

Last, I understand rebalancing doesn’t feel good, especially during bull markets. Think about it. It’s normal to get greedy, especially today. Frankly, rebalancing may be one of the most challenging 10 smart moves to make right now.

It feels wrong, but it’s oh so right if managing risk is a priority. And risk management should be at the top of every investor’s priority list when it comes to 10 smart money moves to make right now.

Tip Six: Check Your Beneficiaries.

I know. Why am I so gloomy during the merriest quarter of the year? Hey, it’s what I do. Recently, even I checked the beneficiaries on my IRA and realized they required updating. Life insurance, retirement accounts, payable on death accounts require proper beneficiary designations and periodic review.

Beneficiaries allow for easy and fast transfer of assets upon death, free of probate. It’s the most common method of inheritance. However, it does have its pitfalls which makes checking and updating even more critical.

In almost all cases, beneficiary designations override a will. So imagine the dilemma this easily fixed issue can create. For example, I have witnessed ex-spouses collect life insurance benefits not intended for them!

Examine account and insurance beneficiary designations online or call providers to receive copies of your choices. Also, don’t discount contingent or secondary beneficiary designations. What if you and your spouse exit the planet at the same time? Would you want assets needlessly transferred through the probate process or left to your estate? Be thorough with designations and check them every three years or when a life change warrants.

One of the easiest of the 10 smart money moves to make right now!

Tip Seven: Establish a Preliminary Household Spending Budget For 2022.

I know. Budget is a four-letter word, and it’s not l-o-v-e.

Household spending is easier than ever to track. Personal spending habits are always at our fingertips, whether through year-end credit card spending reports, Mint, or various smartphone applications. Budgeting is an intimate engagement with not only how you spend your money, but if you dig a little deeper, you’ll understand the why behind spending too. A budget is a fiscal smack in the head, a live example of your relationship with money.

On Sundays, for fun, I assess my budget to make sure spending is within the parameters I establish. And there’s personal satisfaction going old school using pen and paper to review and revise.

So for all the excellent budgeting represents, here are realities you should understand:

First, I observe financial planners treat budgeting as a solution for those who exhibit chronic poor savings habits; when clients fail to improve their financial situation, it frustrates all parties.

Also, I have yet to witness budgeting lead directly to increased savings. People who budget or are thinking of budgeting are already passionate savers. Instead, I see people use budgeting to reinforce good behaviors and pat themselves financially on the back. Stand out.

They’ve been “paying themselves first” since grade school. They were the kids who got visibly excited over new deposit entries in savings accounts passbooks. Note – I still have my frayed Lincoln Savings Bank passbook from 1972.

A Budget Won’t Improve Bad Behavior But It Will Bring Poor Fiscal Habits To The Surface.

Those who budget tend to sock away some portion of their gross income and limit credit card and auto loan debt. Yet, after 30 years in financial services, I have never observed budgeting jolt or motivate anybody into living within their means, establish an emergency reserve fund or save for retirement unless they were coached consistently to do so by a partner or financial professional.

Finally, treat budgeting for what it is and recognize it isn’t some magical fix. Don’t be frustrated as budgeting is like dieting – it won’t work unless you commit to a lifestyle or behavior change that goes deeper than cutting calories and tracking expenses.

Consider a budget as a tool to sharpen the direction of positive actions, not alter the path you’ve been traveling for years.

Tip Eight: Fine Tune Or Create a Tax Strategy For Next Year.

This tip may be one of the most important tips out of the 10 smart money moves to make right now.

I understand we’re in the throes of tax turbulence. It’s exceedingly difficult to plan for the dramatic unknown. But, ultimately, taxes are going higher, and there are still several steps to take to prepare adequately for 2022.

For example, have you had a life change? I catch many single parents filing single when they should be claiming head of household, which is a favorable filing status compared to single.

Also, are you withholding enough or too much from each paycheck? I speak with taxpayers consistently who receive massive refunds (withholding too much) or scramble because they owe thousands. Listen, there’s a happy medium here. Sit down and fine-tune your tax withholding for next year. The IRS website has a decent tax withholding estimator. Please spend some time with it, then go into your employer’s payroll website and modify your W2.

Tip Nine: Review Your Homeowner, Auto And Liability Insurance Coverages.

Due to erratic weather, homeowner insurance premiums have been increasing. In addition, flood insurance coverage premiums are due to skyrocket. Overall, it’s an excellent opportunity to increase deductibles, save on premiums, and undertake an overall review of current coverage with a qualified insurance professional.

Are you overpaying for automobile insurance coverage? Can you fine-tune it based on your needs?

Umbrella liability insurance coverage shouldn’t be overlooked. This coverage is an affordable method to purchase protection in the case of a lawsuit.

Per Investopedia:

- Umbrella insurance is a type of personal liability insurance that covers claims in excess of regular homeowners, auto, or watercraft policy coverage.

- It covers not just the policyholder, but also other members of their family or household.

- Umbrella insurance coverage covers injury to others or damage to their possessions; it doesn’t protect the policyholder’s property.

- Umbrella insurance is quite cheap compared to other types of insurance.

Chris Liebum on our team is an expert in these areas and is happy to assess your needs and review your coverage. E-mail him at Chrise@riaadvisors.com.

Tip Ten: Take Stock Of Your Wellness.

Create a household financial wellness evolution in 2022 and come up with a strategy before the year-end.

At RIA, we define financial wellness as consistent monetary success and pathos, leading to security and generating inner peace. The flow is uneven as stages of wellness ebb and flows along channels of human existence. It’s rarely perfect. However, a strong center or stasis always exists that an individual returns to after a deviation from self-defined financial norms, like a rubber band. For example, the creation of a Financial Vulnerability Cushion is a step toward financial wellness.

Keep in mind, wellness isn’t pretty, but there’s beauty in its consistency. It represents a tumultuous soup of philosophies, experiences, ego, habits, perceptions, and attitudes. The challenge is assessing and maintaining alignment over time and defining what financial security means to you and your family.

More than almost anything else that defines you, financial choices made over a lifetime forge not only the path you travel today but also the ongoing integrity (or lack thereof) of that road you take into the future.

Your overall financial health may flow through to multiple generations long after you’re gone, so it’s worth understanding that money – your actions, how you treat it, is much bigger than any one individual.

Overall, there’s plenty of time to work through these 10 Smart money moves before 2021 concludes.

I wish you tremendous success on the journey, and RIA’s professionals are here to make the process easier for you.