Trending

When the word “crisis” is frequently and accurately applied to the state of retirement planning and savings in this country, it goes without saying that something needs to be done. That’s a call to action for advisors, client and those in the workforce.

It also pays to understand why the state of retirement affairs in the U.S. is at crisis levels. One of the contributing factors is procrastination. As in some people are putting off to tomorrow what they should be doing today.

Yes, there are valid reasons for delaying saving for retirement, including contending with debt loan debt, lack of access to employer-sponsored plans and familial financial obligations, among others. Those are credible reasons to be mindful of money, particularly discretionary spending, but those factors should also be viewed as reasons to work with advisors. After all, advisors can help those that view themselves as unable to save for retirement and see the light. That light includes the advantages of putting even modest sums of money away at an early age for retirement.

The Sooner the Better

Many retirement procrastinators think they have reasons – valid ones – for not saving for retirement right now. In reality, they’ve got excuses because there are no good reasons for delaying building retirement savings, but all the reasons to get going on that today are positive.

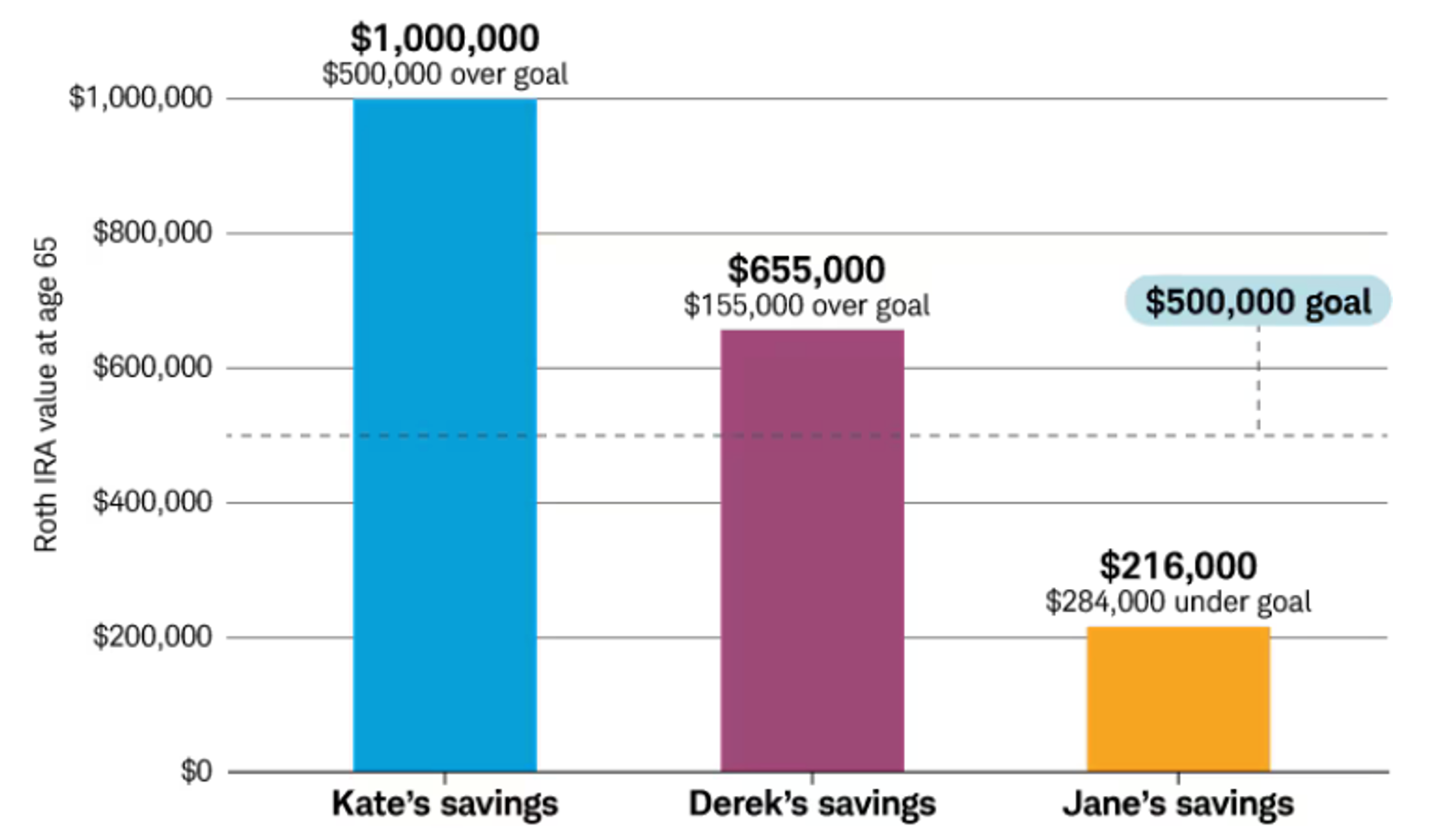

Charles Schwab illustrates as much using the examples of three mythical investors : Kate, 28; Derek, 35; and Jane, 50. Kate starts saving for retirement at 28 to the tune of $7,000 annually while Derek gets in the game at 35 for the same yearly amount. Jane is the procrastinator. She starts saving for retirement at 50, socking away $8,000 per year. By age 65, those three investors will have materially different retirement pictures, as highlighted in the chart below.

(Chart courtesy: Charles Schwab)

“If you start saving in your 20s, contributing 10% to 15% of your paycheck (including any savings match from your employer), you'll be more likely to meet your retirement savings goal. With every decade you delay, however, you'll need to save a larger percentage of your paycheck,” notes Schwab.

Tips for Kickstarting Retirement Savings

For those wanting to jumpstart retirement savings here and now, consider ideas such as investing unexpected income, such as a work bonus or inheritance, into retirement accounts. For those that have access to employer-sponsored plans, contribute as much as is practical as soon as possible.

“For 2025, the maximum 401(k) contribution for employees under age 50 is $23,500, up from $23,000 in 2024. Employees aged 50 or older can make additional catch-up contribution— $7,500 if you’re age 50 to 59 or over 64,” adds Schwab. “For those between age 60 to 63, employees can contribute an additional $11,250. Be sure to take advantage of any match your company offers.”

Point is it’s much better to be a Kate than a Jane and the math proves as much.

Related: Avoid These Critical Pitfalls in the Retirement Red Zone