Trending

Written by: Gabriela Santos and Mary Park Durham

Last week, the Federal Reserve confirmed their next move is an interest rate cut, as they did not seem overly concerned about strong economic data and a bumpier path for disinflation. Afterwards, the S&P 500 hit its 20th all-time high this year, but the risk-on move has not been exclusive to U.S. equities. International equities have moved up 0.8% since the March FOMC meeting and 9.3% since the December one. Emerging Market (EM) equities kept pace last week, but have lagged since December, up a more muted 6.5%. Investors are now wondering: are Fed rate cuts good for EM? Historically, EM has done well in the 24-month period after the last Fed rate hike, as risk appetite improves. As a gradual Fed rate cutting cycle comes into view (in the context of a still strong global economy), EM in particular stands to benefit. Investors should focus on EM regions and sectors that benefit from structural, as well cyclical, tailwinds.

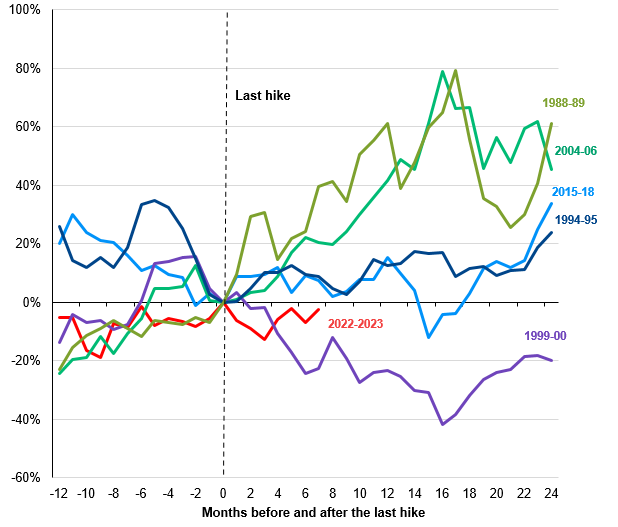

Since 1988, EM equities have delivered positive performance 24 months after the last Fed rate hike in four of the past five Fed rate cycles. On average, returns have been solid at 29%, representing an average outperformance over developed markets of 17 percentage points. Certainly, the broader fundamental backdrop matters, but U.S. rates do play a disproportionate role in driving flows in and out of EM. As a higher risk asset class, EM assets tend to benefit when U.S. interest rate hikes are complete, global economic sentiment is improving, and risk appetite is high. Rather than the specific timing and amount of U.S. rate cuts, taking the risk of further rate hikes off the table is already beneficial, especially as it builds confidence in the resilience of the U.S. economy and helps risk appetite improve.

In fact, when looking beneath the surface, this time has been less of an exception than meets the eye. Since the pandemic, it has been key to differentiate China from the rest of EM, as China has been experiencing challenges unique to its market. Since the Fed’s December meeting (when the end of the rate hiking cycle was confirmed), EM excluding China has moved up 9.7% rather than 6.8% for the broad EM index. Going forward, investors should continue to hone in on the pockets of EM where positive structural tailwinds also exist. As we have argued previously, these include: supply chain shifts, semiconductor and AI enthusiasm, growing commodity demand, and the rise of the EM middle class. These themes stand to benefit consumer, industrial, technology, financial and commodity companies in EM ex-China.

The end of Fed hiking cycles tends to be positive for EM

EM equities, USD, price return, indexed to zero at the last Fed hike

Source: FactSet, Federal Reserve, MSCI, J.P. Morgan Asset Management. The 2022-2023 cycle assumes that the last hike of the cycle was in July 2023. Past performance is not a reliable indicator of current and future results. Data are as of March 26, 2024.

Related: Consumer Confidence: Impact on Subsequent S&P Returns