Trending

Written by: Jordan Jackson

As is customary, the Congressional Budget Office (CBO) regularly publishes baseline projections for federal revenues, outlays, and deficits for the current fiscal year and subsequent decade that assume current tax and spending legislation remains unchanged. While it is well-known that the U.S. government runs a chronic budget deficit, averaging roughly 3% of GDP over the past 30 years prior to the pandemic1, changes to tax and spending legislation under both the Trump and Biden Administration made accounting and forecasting the budget deficit in fiscal year (FY) 2023 particularly challenging.

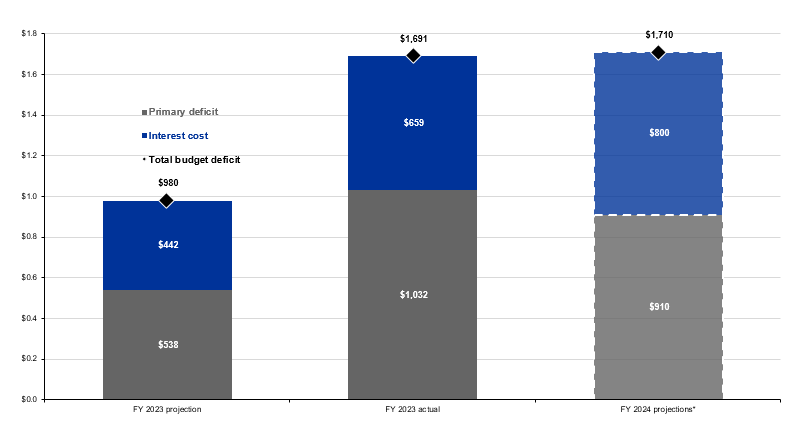

Indeed, in its May 2022 baseline budget forecast, the CBO projected the deficit for FY 2023 to be $980bn. The actual budget deficit ending September 30th (after correcting for a non-cash accounting adjustment due to the Supreme Court ruling prohibiting student loan forgiveness) came in at just under $1.7 trillion suggesting a huge underestimate of over $700 billion in financing needs for the federal government. Of course, deficits are financed through Treasury issuance, and it is likely this significant increase in Treasury bond supply relative to estimates contributed to the move higher in bond yields this year.

There were a few factors that contributed to the increase in financing needs this year:

- Revenues: CBO overestimated revenues by $480 billion largely driven by individual income, payroll and corporate income taxes. Weak capital markets and corporate earnings in 2022 impacted capital gains and corporate income tax receipts last year. Moreover, more employers claimed the Employee Retention Tax Credit (ERTC) under the CARES Act, a government credit to businesses that maintained and paid wages to employees through the pandemic, causing a net impact to the deficit of $120bn.

- Outlays: CBO underestimated outlays by roughly $560 billion due to increased higher education expense, deposit insurance, interest costs and social security estimates. Higher education was underestimated by $143 billion driven by the Department of Education’s changes to income-driven repayment plans and an extended pause in loan repayment and interest accrual2. Increased spending on deposit insurance stems from payments made by the Federal Deposit Insurance Corporation (FDIC) to facilitate the resolution of bank failures in spring 2023. Lastly, high inflation and interest rates in 2022 led to higher COLA adjustments to social security payments and greater interest expense on the debt.

To be clear, forecasts are never completely accurate, though given the CBO has historically overestimated the deficit roughly two-thirds of the time3, makes last years’ underestimate quite unusual. Importantly though, some of the accounting irregularities and economic conditions should not impact the deficit to the same degree in 2024 and we now expect the deficit for FY 2024 to be generally in line with last years at $1.7 trillion. This could potentially soften concerns of increasing Treasury supply next year. That said, the overall trajectory of federal finances remains unsustainable, and some degree of fiscal austerity will be needed in the years ahead.

1 Average is from FY 1990 to FY 2019.

2 This analysis ignores the subsequently overruled student debt forgiveness plan.

3 The Accuracy of CBO’s Budget Projections for Fiscal Year 2023, December 2023

Total deficit should be broadly unchanged next year given higher interest expense and smaller primary deficit

USD trillions, US federal budget deficit, CBO FY23 baseline projection vs. actual, JPMAM FY24 forecast

Related: What Is the Market Outlook for 2024?