Trending

Powell testimony is over, with markets rejoicing the promise of still accomodative Fed. Value keeps surging over growth, and regardless of yesterday‘s great performance, tech has a vulnerable feel to it – semiconductors lead higher, fine, but communications didn‘t confirm, and the healthcare-biotech dynamic isn‘t painting an outperformance picture either. Real estate isn‘t taking as strong a cue while consumer discretionaries recovery could also be stronger. Thus far though, no need to think about taking losses to optimize your gains elsewhere.

Just as I wrote yesterday:

(…) the financials benefiting from the greater spread, won‘t save the day, as the key chart to watch now is technology and also healthcare. … The sectoral outlook remains mixed, even as value continues greatly outperforming growth this month. … Long-term Treasuries are starting to hold greater sway over the stock market fate now, too. The dollar‘s woes thus far continue playing out largely in the background.

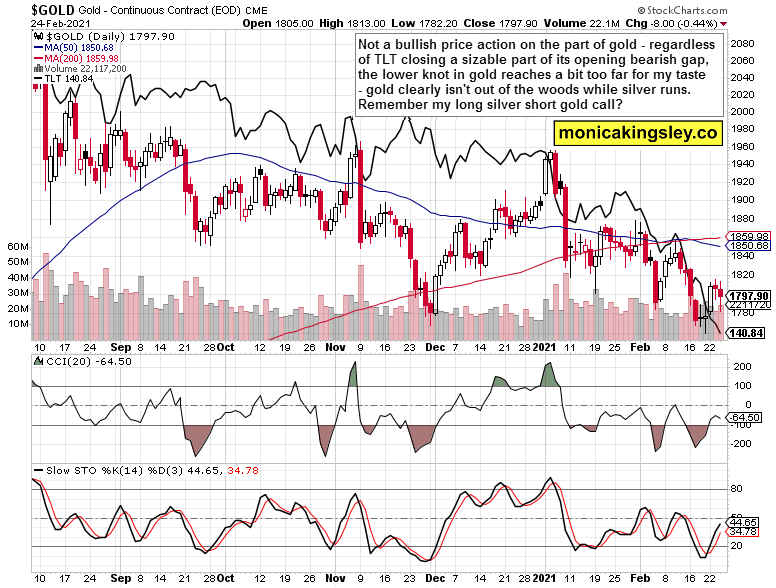

Did gold shake off the TLT shackles? I‘m getting increasing doubts that only a strong move to the upside would dispel. As long-term Treasuries were staging an intraday reversal, gold took an intraday plunge before recovering. Not a good sign of internal intraday strength. Could it be a bullish flag? Still possible, but again, gold would have to rally from here. Doing so would result in a bullish divergence in its daily indicators.

The precious metals sectoral dynamics remains positive though – silver and platinum are bullishly consolidating, and as I‘ll show you in today‘s final chart, the many mining indices are doing fine as well. The overly strong reflationary (I would call a spade a spade, and say inflationary) efforts are driving commodities higher in a supercycle just starting out.

Not to get complacent, GameStop (GME) squeeze has made a comeback yesterday. Will it coincide with broader stock market woes on par with late Jan? Way too early to say – let‘s jump right into the charts for an objective momentary view instead.

Here they are, all courtesy of www.stockcharts.com.

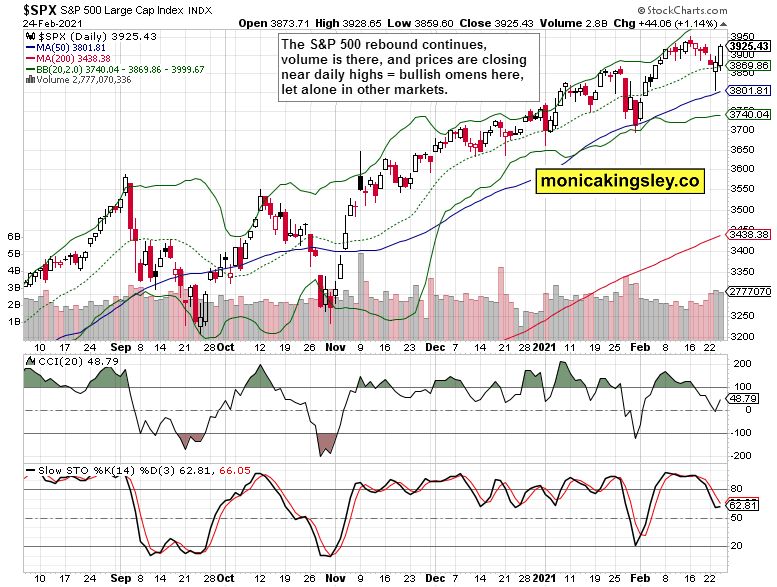

S&P 500 and Its Internals

Strong S&P 500, everything looks fine on the surface – just as should be, befitting buy the dip mentality. Strong volume, no meaningful intraday setback, so far so good.

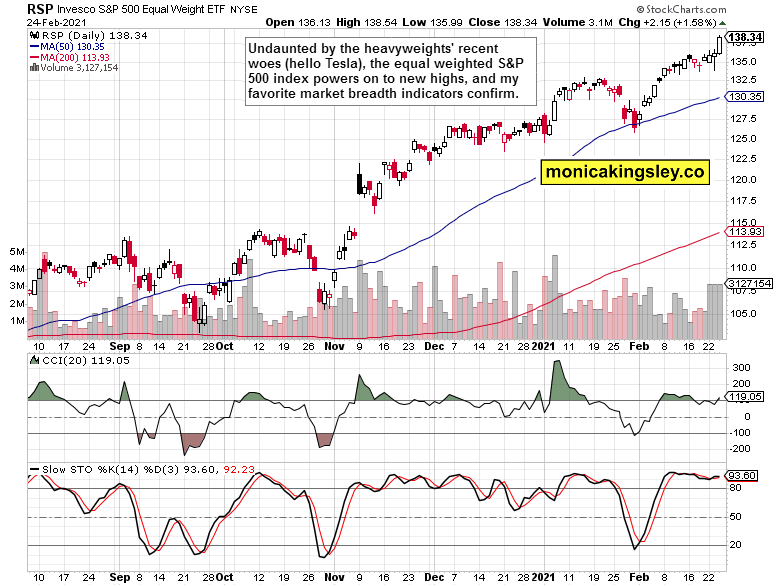

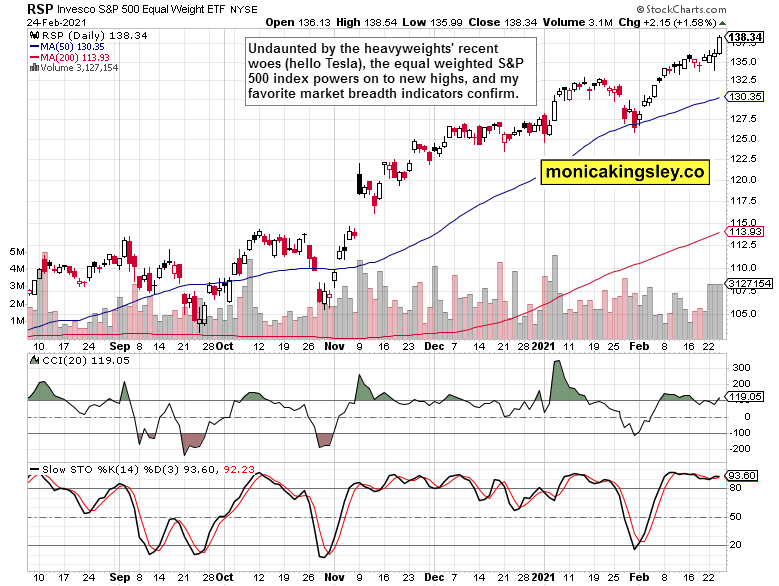

The equal weight S&P 500 chart is looking better and better day by day. New highs, strong uptrend, broadening leadership. It‘s a mirror reflection of the big names‘ woes, and a testament to value outperforming growth. This bull run is far from making a top.

Credit Markets

High yield corporate bonds (HYG ETF) had a good day yesterday, and so did the high yield corporate bonds to short-dated Treasuries (HYG:SHY) ratio. Yet it‘s the daily stock market outperformance that is noticeable here – optimistic sign of an all clear signal. I‘m not taking it totally at face value given tech performance – in a short few days, I can easily become more convinced though.

Technology

Strong daily tech (XLK ETF) upswing, yet only half the prior downside erased so far, and the volume could be higher compared to the preceding downswing. Semiconductors (XSD ETF) are leading again, fine. Yet it‘s the heavyweight names that matter the most to me right now – check out yesterday‘s observations:

(…) The tech jury is still out, and this heavyweight sector remains vulnerable, with consequences to the S&P 500 if it doesn‘t keep on the muddle through recovery path at the very least

Dollar

Look how little the Powell tremors achieved – the dollar bulls are still on the run. Upswings are being sold as the greenback remains on the defensive, targeting much lower lows this year. The technical rebound is over, and not even higher yields can help the greenback much.

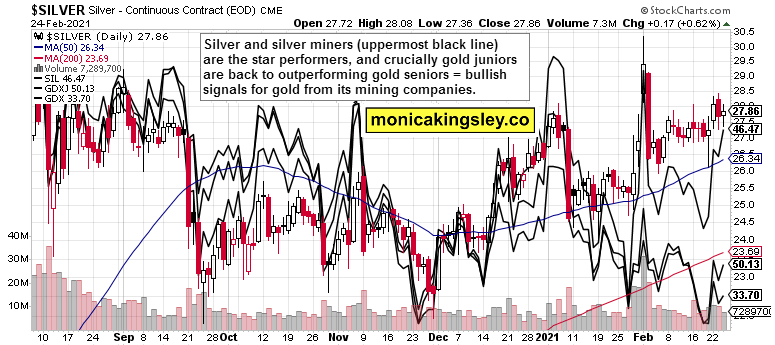

Gold, Silver and Miners

For a second day in a row, gold‘s performance isn‘t convincing – the willingness to clearly and directionally decouple from rising yields, is being questioned. On the other hand, e.g. the 10-year UST yield is approaching the summer 2019 lows – it‘s at 1.38% now. I‘m looking for the rising rates to slow down and possibly even pull back a little from here over the coming weeks. Or would the market just like to slice through that resistance? Inflation isn‘t universally that strong right now yet I think – just look at the velocity of money.

Everything silver related is doing fine, silver miners (SIL ETF) rebounded strongly, First Majestic Silver Corp (AG) and Hecla (HL) are in clearly bullish patterns. The white metal‘s every dip is being bought, the silver-to-gold ratio keeps improving, and even gold juniors (GDXJ) started once again outperforming the seniors (GDX). The bullish signals under the surface keep increadingly more coming to the fore, and the miners to gold ratio‘s ($HUI:$GOLD and GDX:GLD) is the final ingredient missing.

Summary

Stock bulls did great yesterday, but everything isn‘t fine yet in the tech realm. Due to its sheer weight in the S&P 500 index, pulling the cart a bit more enthusiastically is what the 500-strong index needs to take on new highs, because value stocks can‘t do it all.

Gold and silver fared mostly well during the Powell testimony part II, yet gold didn‘t convince me really again. I look for the yellow metal bulls to get tested soon. The wildcard is reaction to the rising Treasury yields as they‘re in a key resistance zone of summer 2019 lows overall (10-year approaching it, and as regards 30-year, it‘s been overcome already). Plunging dollar and short-term gold-dollar correlation moving to positive figures, isn‘t a pleasant sight for coming days.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Related: Technology Holds the Key To S&P 500