Trending

The CNN fear greed index of investor sentiment has fallen to “extreme fear” at 18 on a scale of 0 to 100. Moreover, those expressing bearish sentiment in the AAII individual investor survey are above 60%, which is only the sixth time since 1987 that it has been that high. Watching CNBC or Bloomberg might make you think the stock market is crashing or, at a minimum, extremely volatile. Statistically speaking, neither is the case.

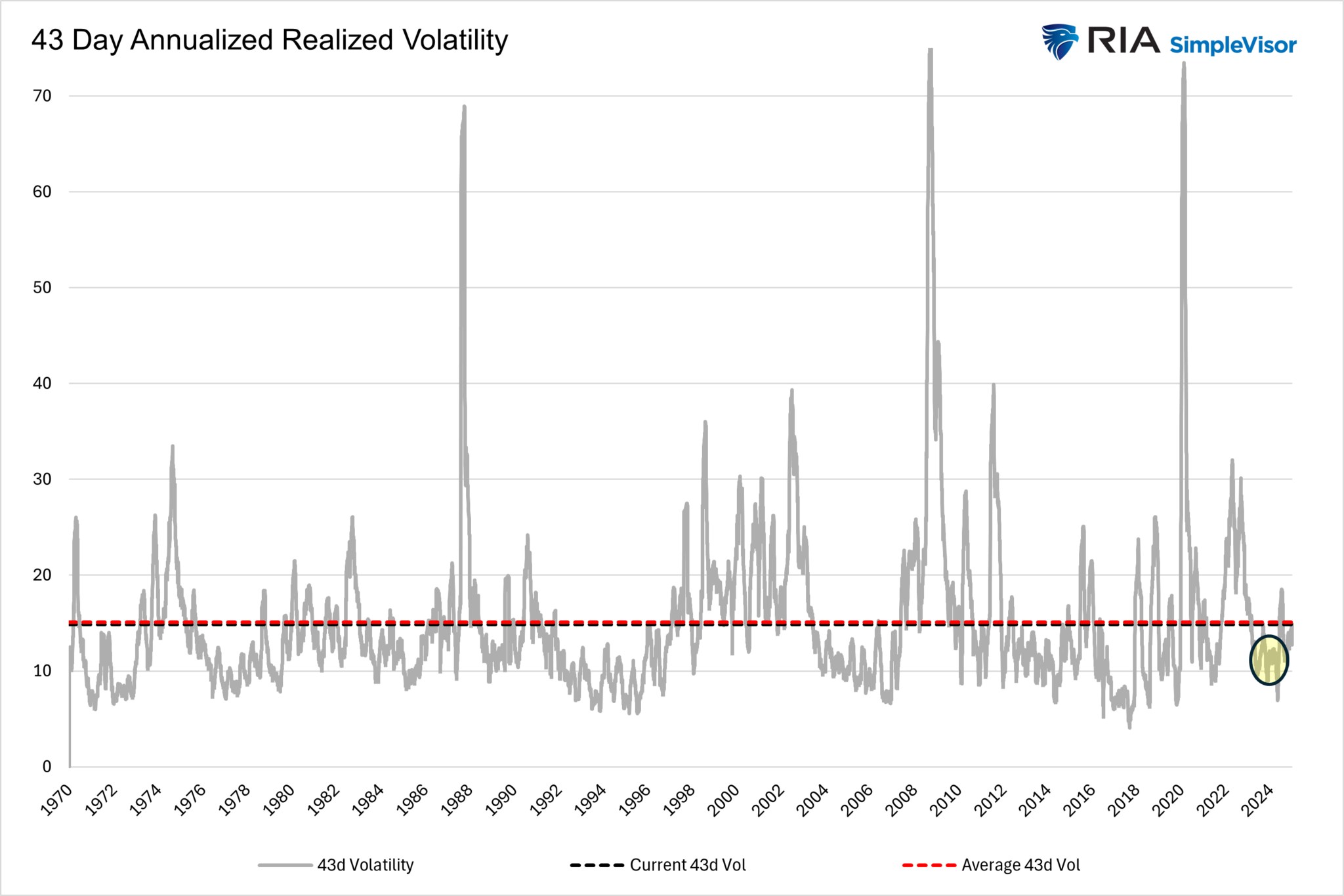

The following analysis compares the S&P 500’s most recent 43-day activity (2025 YTD) to every other 43-day period since 1970 and to those over the last two years (2023-2024). Through Thursday, March 6th, the S&P 500 is down about 2.5%, hardly a crash. The 43-day annualized realized volatility during this period is 14.8, which is actually a hair below the average of 15.07 since 1970. However, it is decently elevated from the 12.95 average over the last two years.

Our takeaway from this analysis is that recent market behavior is historically typical. However, we were lulled to sleep with low volatility over the last two years, so the recent trading patterns seem more extreme than they are.

What To Watch

Earnings

![]()

Economy

![]()

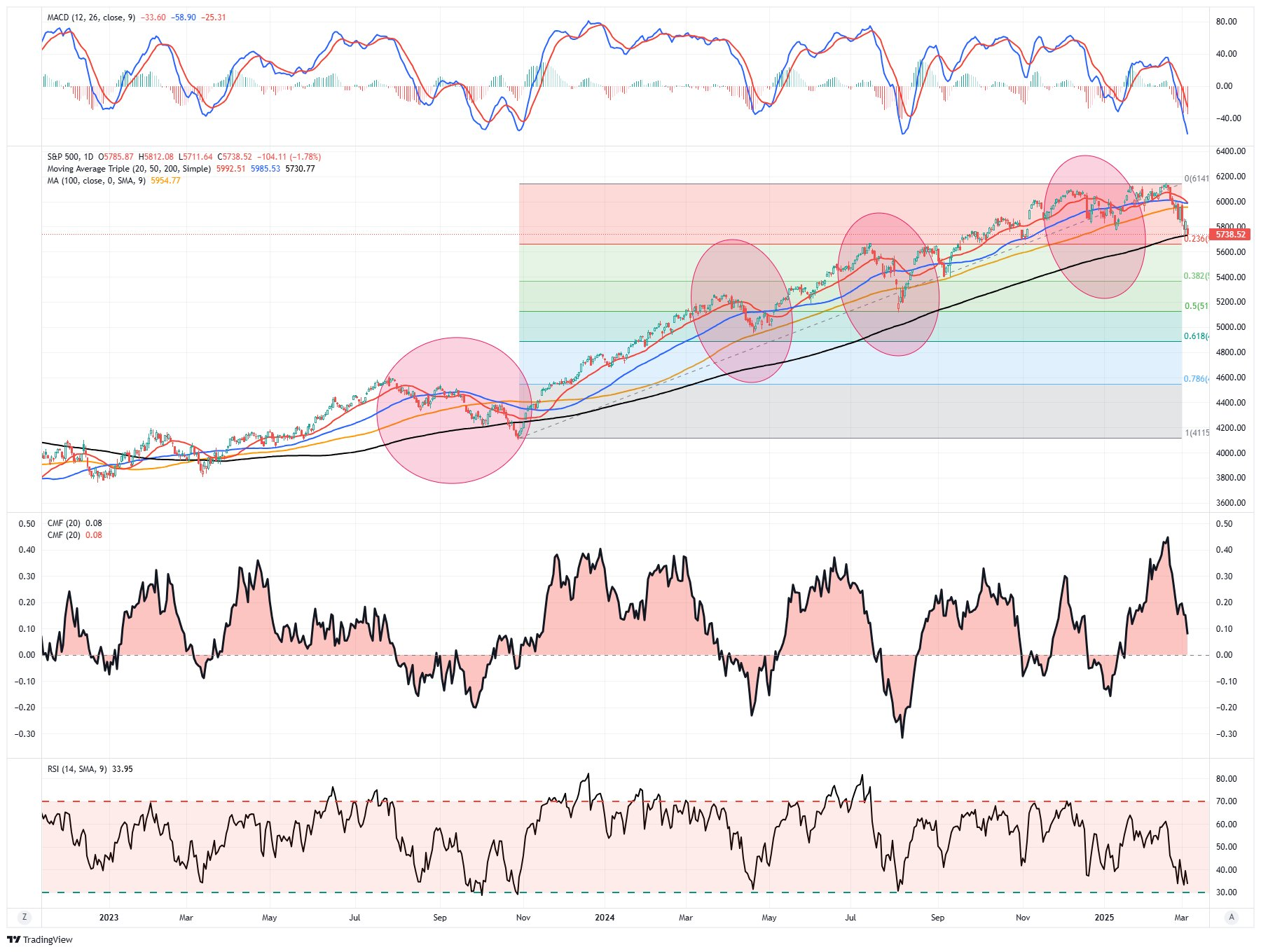

Market Trading Update

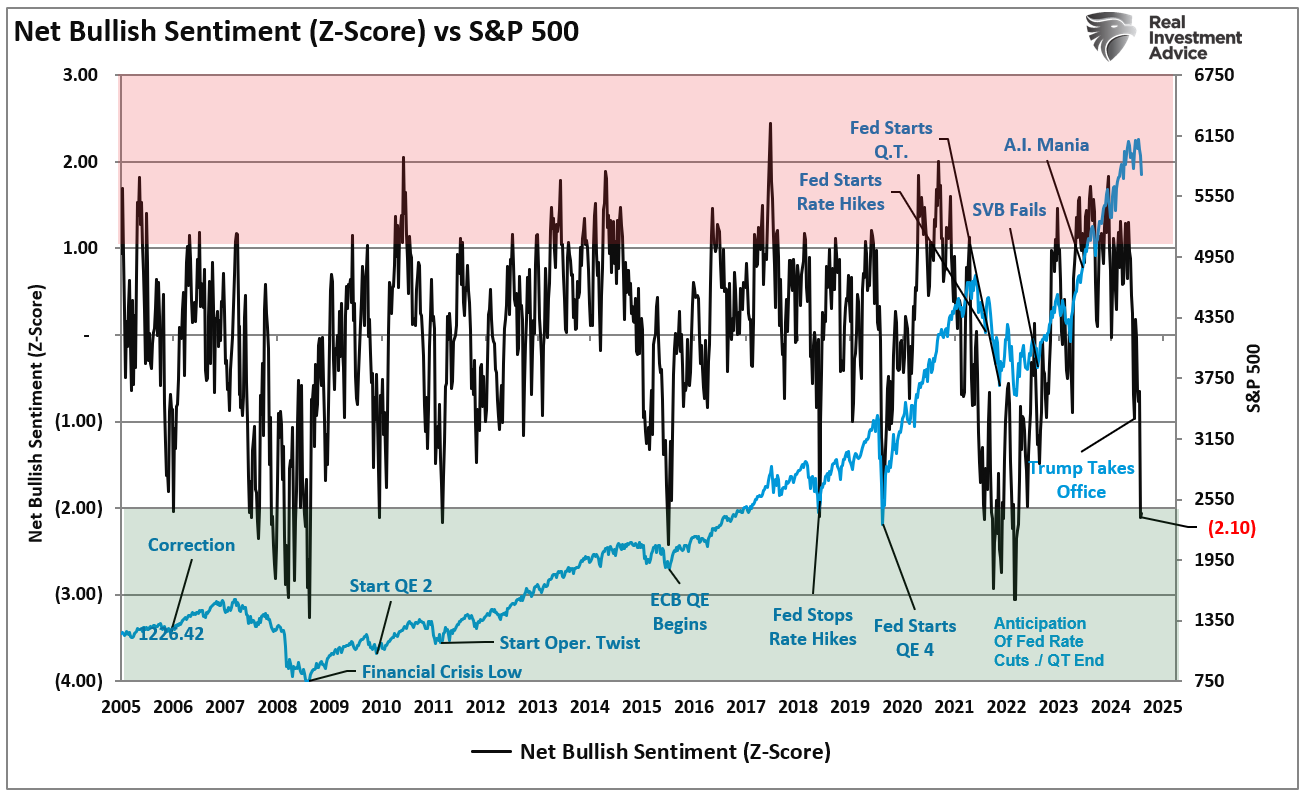

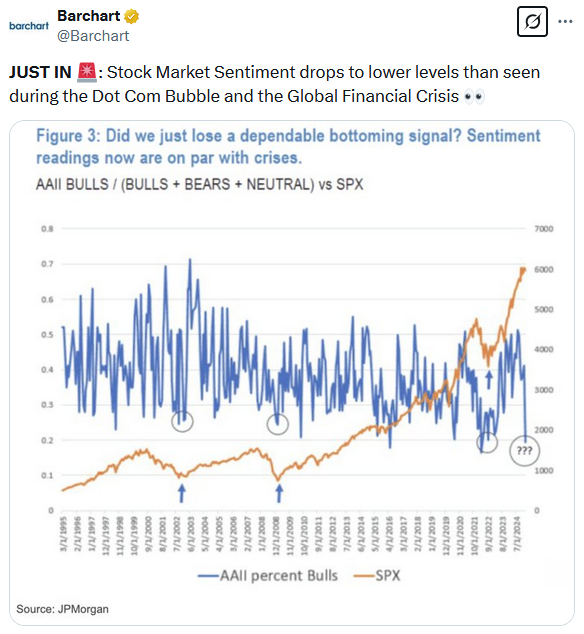

Last week, we discussed the more extreme levels of bearishness that have gripped the markets as of late.

“In other words, while the media scrambled to align reasons with the sell-off, the correction was very much in line with seasonal tendencies. Crucially, that sell-off has pushed investor sentiment to levels typically equating to much deeper corrections. From a contrarian view, that extreme negative sentiment, now combined with oversold conditions, provides a good base for a rally in March.”

“Sentiment is approaching two standard deviations below its average level. Such levels are more coincident with market bottoms than the beginning of a corrective cycle. I have labeled some events along the way. The lesson is that headlines drive sentiment, and when sentiment becomes too negative, as may be the case today, such allows for rallies to form.”

The sentiment chart has been updated, showing that bearish sentiment reached even more profound levels of negativity and is more than two standard deviations below the norms.

However, despite the deep levels of negativity, the current correction is well within the context of the volatility seen during Trump’s first term as he engaged in a trade with China. We will discuss this more momentarily.

While Trump’s tariffs and bearish headlines currently dominate investors’ psychology, we must remember that corrections are a normal market function. Yes, the market is down roughly 7% from the peak, but we have seen these corrections repeatedly in the past. That does NOT mean a more extensive corrective process is not potentially in process. It only implies that markets are likely in a position for a technical rally to reverse the more extreme oversold conditions.

The point is to remember how you felt during those corrections and what actions you took. Were they the correct actions? If they weren’t, then why are you potentially repeating past mistakes?

Volatility is the price we pay to invest. The hard part is avoiding volatility’s behavioral impacts on our investing outcomes.

Employment & The Week Ahead

The BLS jobs report was good on the surface but problematic once you dig into it. Most concerning to us is the broader measure of the unemployment rate, the U6 and the household survey. Per the BLS, the U6 includes all those in the unemployment rate, plus:

All Persons Marginally Attached to the Labor Force, Plus Total Employed Part Time for Economic Reasons, as a Percent of the Civilian Labor Force Plus All Persons Marginally Attached to the Labor Force

The U6, shown below, rose from 7.5% to 8%, despite the unemployment rate (U3) only rising .1% to 4.1%. Bear in mind, the Fed focuses on U3, not U6, so this job report is unlikely to overly concern the Fed. However, most federal employee and contractor layoffs occurred after the BLS reference week, so the initial impact of DOGE cuts has yet to be seen. Consequently, the March report will be more important. Also of concern is that the household employment survey fell by 588k jobs in February, the largest drop since December 2023.

We will get one more piece of job data with the JOLTs report on Tuesday. CPI and PPI, on Wednesday and Thursday, respectively, will be the key data points this week. The market expects CPI to increase by 0.3% after rising by 0.4% last month. Also of note this week is the NFIB Small Business Optimism Index on Tuesday. The Fed will be quiet as they enter their media blackout in advance of their March 19th FOMC meeting.

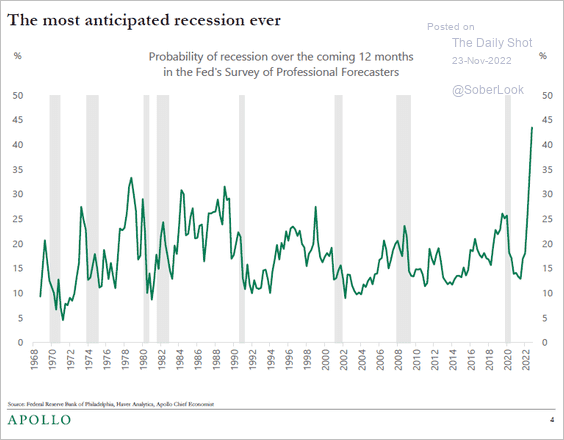

The Risk Of A Recession Isn’t Zero

The risk of a recession in the U.S. is not zero. This is particularly true as the current Administration tackles Government bloat and implements tariffs. However, before we discuss why the risk of a recession could increase, it is crucial to remember the 2022 experience. At that time, most economists were convinced a “recession was imminent.” As discussed in early 2023, it was the most anticipated recession ever.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Why Tesla Shareholders Are Betting Beyond Car Production