Trending

Written By: Lance Roberts J. Bradford Delong wrote a very interesting article discussing the trigger for the next recession. “Three of the last four US recessions stemmed from unforeseen shocks in financial markets. Most likely, the next downturn will be no different: the revelation of some underlying weakness will trigger a retrenchment of investment, and the government will fail to pursue counter-cyclical fiscal policy. Over the past 40 years, the US economy has experienced four recessions. Among the four, only the extended downturn of 1979-1982 had a conventional cause. The US Federal Reserve thought that inflation was too high, so it hit the economy on the head with the brick of interest-rate hikes. As a result, workers moderated their demands for wage increases, and firms cut back on planned price increases. The other three recessions were each caused by derangements in financial markets. After the savings-and-loan crisis of 1991-1992 came the bursting of the dot-com bubble in 2000-2002, followed by the collapse of the sub-prime mortgage market in 2007, which triggered the global financial crisis the following year.” While I agree with Bradford’s point, I think there is a disconnect between the crises he points out and repeated behaviors which lead to those events.

Let’s review some basic realities about the economy that seems to be lost on the mainstream media.

First, this is NOT an economic cycle: This is:

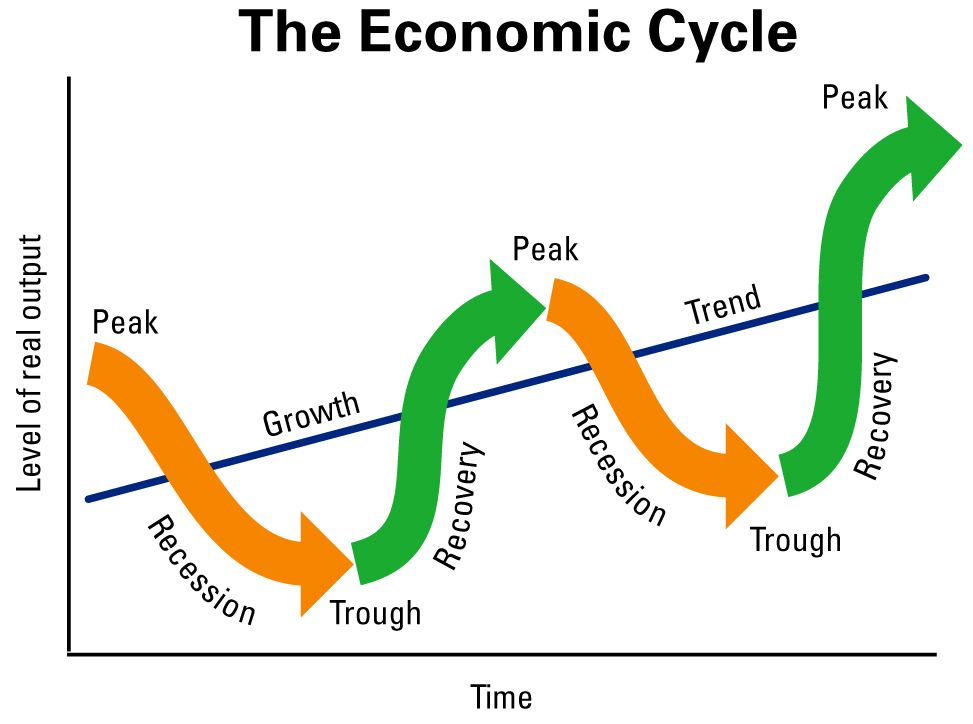

This is: Despite the hopes the economy will continue into an everlasting expansion, such has historically never been the case. The current economic expansion, which has been driven by massive infusions of liquidity, extremely accommodative interest rate policy, and a surge in debt accumulation, is just 4-months away from setting a new record.

Despite the hopes the economy will continue into an everlasting expansion, such has historically never been the case. The current economic expansion, which has been driven by massive infusions of liquidity, extremely accommodative interest rate policy, and a surge in debt accumulation, is just 4-months away from setting a new record. Secondly, while the recession prior to 1980 was driven by a super-aggressive Fed rate tightening policy, since 1950 we can find fingerprints of monetary policy in every event.

Secondly, while the recession prior to 1980 was driven by a super-aggressive Fed rate tightening policy, since 1950 we can find fingerprints of monetary policy in every event. I am not saying that just because the Fed hikes rates, that a recession, or crisis, will be triggered.What I am saying is that over the entire rate cycle, the Fed has fostered the credit driven expansion and laid the groundwork necessary for a crisis to be born.Let’s revisit Bradford’s three specific crises.

I am not saying that just because the Fed hikes rates, that a recession, or crisis, will be triggered.What I am saying is that over the entire rate cycle, the Fed has fostered the credit driven expansion and laid the groundwork necessary for a crisis to be born.Let’s revisit Bradford’s three specific crises.The S&L Crisis

The savings and loan crisis of the 1980s and 1990s (commonly dubbed the S&L crisis) was the failure of 1,043 out of the 3,234 savings and loan associations in the United States from 1986 to 1995.However, just looking at the event we miss the bigger picture.If we go back in time before the crisis began, we find an environment where the Federal Reserve had drastically lowered the overnight lending rates in order to spur more borrowing and economic activity coming out of the back-to-back recessions of the late ’70s and early ’80s.Of course, in a capitalist-driven economy, as demand for loans for cars, housing, businesses, etc. rose; bankers figured out ways to continue to extend credit in order to maximize their profitability. As is always the case, greed over took prudence and many bankers relaxed risk management protocols which would ultimately cost them their jobs and in many cases the bank.Of course, in 1979, when the Federal Reserve hiked the discount rate from 9.5% to 12%, ostensibly to quell inflation pressures, it also slowed the economy. Since the S&L’s had issued long-term loans at fixed rates lower than the now higher rate at which they could borrow the rise in rates combined with rising default rates, led to insolvency.Probably the most famous example from the S&L Crisis period wasthat of financier Charles Keating, who paid $51 million financed through Michael Milken’s “junk bond”operation, for his Lincoln Savings and Loan Association which at the time had a negative net worth exceeding $100 million.The Dot.com Bubble

While the “dot.com” bubble is often thought of as a one-off event caused by speculative excess, there was actually much more going on at the time.Many have forgotten the names of Enron, WorldCom, Global Crossing, and other booming tech companies which were riff with financial shenanigans at the time which ultimately led to the passage of the Sarbanes-Oxley Act.However, again, we can’t look at just the event itself but need to go back prior to the event to understand the groundwork that was laid.Following the recession of 1991, the Federal Reserve drastically lowered interest rates to spur economic growth. However, the two events which laid the foundation for the “dot.com” crisis was the rule-change which allowed the nations pension funds to own equities and the repeal of Glass-Steagall which unleashed Wall Street upon a nation of unsuspecting investors.The major banks could now use their massive balance sheet to engage in investment-banking, market-making, and proprietary trading. The markets exploded as money flooded the financial markets. Of course, since there were not enough “legitimate” deals to fill demand and Wall Street bankers are paid to produce deals, Wall Street floated any offering it could despite the risk to investors.Of course, it wasn’t long until the Federal Reserve, again concerned about the prospect of rising inflation and an overheating economy, started hiking rates. As monetary policy became more restrictive, the cost of capital rose, and the economy slowed.It wasn’t long before the system came unglued.Related: 3 High-Flying Stocks to Sell Before a Bear MarketThe Great Financial Crisis

In response to the “Dot.com” crisis, the Federal Reserve once again drastically lowered interest rates to spur economic growth.This was also the point where the Bush Administration, along with the Alan Greenspan headed Federal Reserve, decided that “everyone” should own a home. Lending standards were relaxed and a variety of new mortgage structures were introduced by Wall Street in the quest to make money.Over the next several years, as lending rates declined, and everyone wanted to buy into the surging housing market, Wall Street packaged mortgages into exotic instruments allowing them to sell the mortgages to investors. The cycle continued with ever increasing demand from home buyers and demand from investors.As the housing market boomed, the stock market fully recovered from the “dot.com” crash, and with the economy booming, the Federal Reserve, now under the leadership of Ben Bernanke, decided to start tightening monetary policy in the belief that inflation was an imminent threat from an overheating economy.But there were no pressing concerns as it was believed that “subprime mortgage loans were contained”and the ongoing “Goldilocks economy” would continue uninterrupted.They weren’t and it didn’t.If you are interested in this crisis we urge you to read or watch The Big Short by Michael LewisThe Common Threads

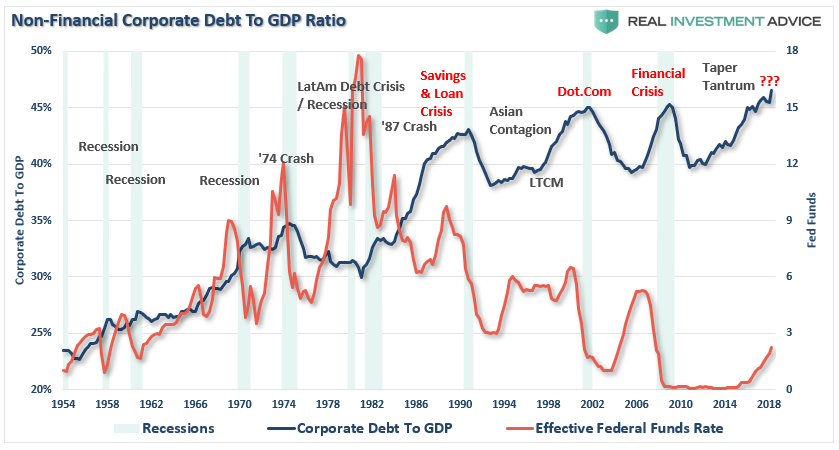

While each of these events were much more complex than what I have outlined here, there were many others along the way like the Russian Debt Default, The Asian Contagion, and Long-Term Capital Management, which all shared important commonalities between them.In each case we find that prior to the event the Federal Reserve was loosening monetary policy to spur economic growth following a preceding economic downturn. They did this to halt the downturn but in doing so failed to allow the system to clear itself over time.Looser monetary policy, and continuing relaxation of regulations led to excessive greed by the primary players in the market which was supported by a rising level of speculative frenzy and easy access to capital by investors.In other words, instead allowing the system to clear the previous build up of excesses, the Federal Reserve intervened to keep that process from happening. As a result, each crisis has been worse than the one before it because the debt and leverage in the system continues to mount.As shown in the chart below, whenever the Federal Reserve previously loosened monetary policy, debt as a percentage of the economy surged. Naturally, when monetary policy was reversed, things tended to go bad…and generally very quickly. Since 1980, the eventual and inevitable unwind of an overly levered system was met by a drastic drop in the Fed Funds rate to stimulate debt induced consumption and spur economic activity. The problem, is that each effort by the Fed to limit the impact to the system has required a lower interest rate than the one that preceded.With rates near the lowest level on record still, the next event will once again require dramatic measures to stem the unwinding of a decade long, debt supported, economic cycle.But this is where Bradford gets it absolutely right about the cause of the next recession. “Specifically, the culprit will probably be a sudden, sharp ‘flight to safety’ following the revelation of a fundamental weakness in financial markets. “Of course, such has always been the case when it comes to the financial markets.However, the risk of a recession has continued to rise in recent months with plenty of warnings already showing up from a near-inverted yield curve, declining economic momentum, low nominal and real bond yields, and struggling stock prices.The problem, as Bradford notes, is the next financial cataclysm may well fall outside of the capability of the Federal Reserve and Government to neutralize. “If a recession comes anytime soon, the US government will not have the tools to fight it. The White House and Congress will once again prove inept at deploying fiscal policy as a counter-cyclical stabilizer; and the Fed will not have enough room to provide adequate stimulus through interest-rate cuts. As for more unconventional policies, the Fed most likely will not have the nerve, let alone the power, to pursue such measures.”"As a result, for the first time in a decade, Americans and investors cannot rule out a downturn. At a minimum, they must prepare for the possibility of a deep and prolonged recession, which could arrive whenever the next financial shock comes.”He is absolutely correct in his assessment of the impact of the next fiscal problem. When it comes, it will be totally unexpected, unanticipated, and unprepared for by investors. Such has always been the case through out history.But there is one thing that all these crises have in common."A belief by the Federal Reserve that inflation is going to be problem and that they can control inflation through monetary policy."This time will be no different.

Since 1980, the eventual and inevitable unwind of an overly levered system was met by a drastic drop in the Fed Funds rate to stimulate debt induced consumption and spur economic activity. The problem, is that each effort by the Fed to limit the impact to the system has required a lower interest rate than the one that preceded.With rates near the lowest level on record still, the next event will once again require dramatic measures to stem the unwinding of a decade long, debt supported, economic cycle.But this is where Bradford gets it absolutely right about the cause of the next recession. “Specifically, the culprit will probably be a sudden, sharp ‘flight to safety’ following the revelation of a fundamental weakness in financial markets. “Of course, such has always been the case when it comes to the financial markets.However, the risk of a recession has continued to rise in recent months with plenty of warnings already showing up from a near-inverted yield curve, declining economic momentum, low nominal and real bond yields, and struggling stock prices.The problem, as Bradford notes, is the next financial cataclysm may well fall outside of the capability of the Federal Reserve and Government to neutralize. “If a recession comes anytime soon, the US government will not have the tools to fight it. The White House and Congress will once again prove inept at deploying fiscal policy as a counter-cyclical stabilizer; and the Fed will not have enough room to provide adequate stimulus through interest-rate cuts. As for more unconventional policies, the Fed most likely will not have the nerve, let alone the power, to pursue such measures.”"As a result, for the first time in a decade, Americans and investors cannot rule out a downturn. At a minimum, they must prepare for the possibility of a deep and prolonged recession, which could arrive whenever the next financial shock comes.”He is absolutely correct in his assessment of the impact of the next fiscal problem. When it comes, it will be totally unexpected, unanticipated, and unprepared for by investors. Such has always been the case through out history.But there is one thing that all these crises have in common."A belief by the Federal Reserve that inflation is going to be problem and that they can control inflation through monetary policy."This time will be no different.