Trending

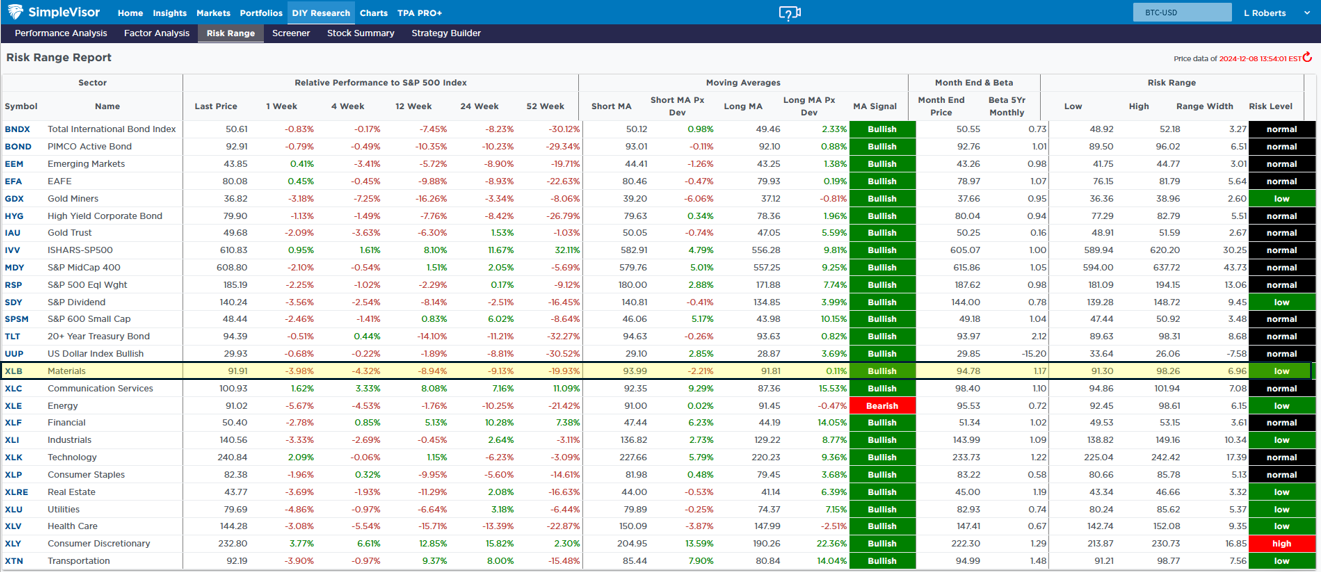

Material stocks have been one of the worst-performing sectors this year, lagging the S&P 500 by nearly 20%. Since the election, its relative performance versus the market has continued to worsen. Therefore, given the historical correlation between the economy and the materials sector, we must assess what the sector’s underlying stocks are trying to tell us.

We think the message is twofold. The easy takeaway is that Donald Trump will invoke tariffs on goods imported from China and other countries. Many of these goods that are likely to be tariffed are produced and mined abroad by companies in the materials sector.

However, the problem with blaming Trump tariffs is that the materials sector was weak well before the election. The materials sector has a strong relationship with the economy, primarily due to construction. In past Commentary, we have noted that residential and multifamily new construction projects are ebbing. Furthermore, commercial building construction has been weak. Thus far, the economy has held up well despite the slowdown in the real estate sector. Might material stocks be an early warning that the economy is weaker than the current statistics portray? Or might the economy be less reliant on construction than it has been?

What To Watch

Earnings

Economy

Market Trading Update

Yesterday, we discussed the need for portfolio rebalancing as we head into year-end, which could lead to some short-term volatility in the markets. We expect any correction process to be relatively mild and present an opportunity for traders to add exposure heading into year-end. However, over the next two weeks, the ride could get a little bumpy, and the volatility index suggests the same.

As shown, traders have become extremely complacent in the market lately, with little concern about a correction. Historically, high “complacency” is often a good time to become more “risk-conscious” from a contrarian point of view. The MACD is oversold and close to triggering a short-term “buy” signal for volatility, likely translating into lower stock and risk asset prices. Furthermore, the relative strength index (RSI) is also oversold and turning higher, also warning of a potential rise in volatility.

While such a turn in volatility does not mean the market is about to crash, it suggests that investors may see weaker asset prices over the next two weeks. Stocks, bitcoin, and more speculative trading vehicles like zero-day stock options and leveraged ETFs would likely face the most pressure. As is always the case, taking profits, hedging risk, and raising cash levels can reduce any corrective action risk.

However, as noted, whatever corrective action is taken before Christmas should be used to prepare portfolios for a year-end rally as managers “window dress” for their annual reporting.

Trade accordingly.

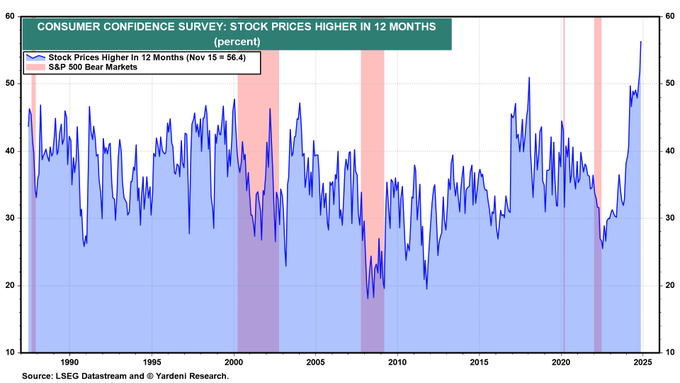

Confidence In Stocks Soars

The Conference Board’s November Consumer Confidence Index survey shows that 56.4% of consumers expect stocks to be higher in the next 12 months, as shown below. Investors’ optimism over future returns is not shocking because the stock market has logged two +20% annual performances in a row. However, it’s noteworthy that optimism for 2025 returns is now higher than in 1999 and all prior periods going back at least 35 years.

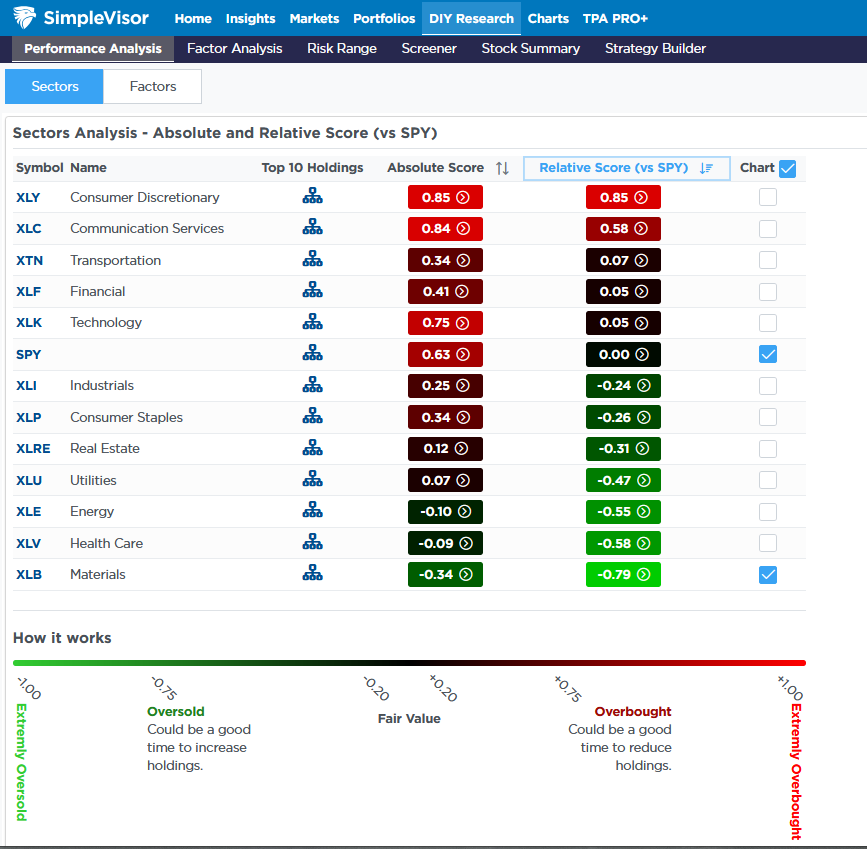

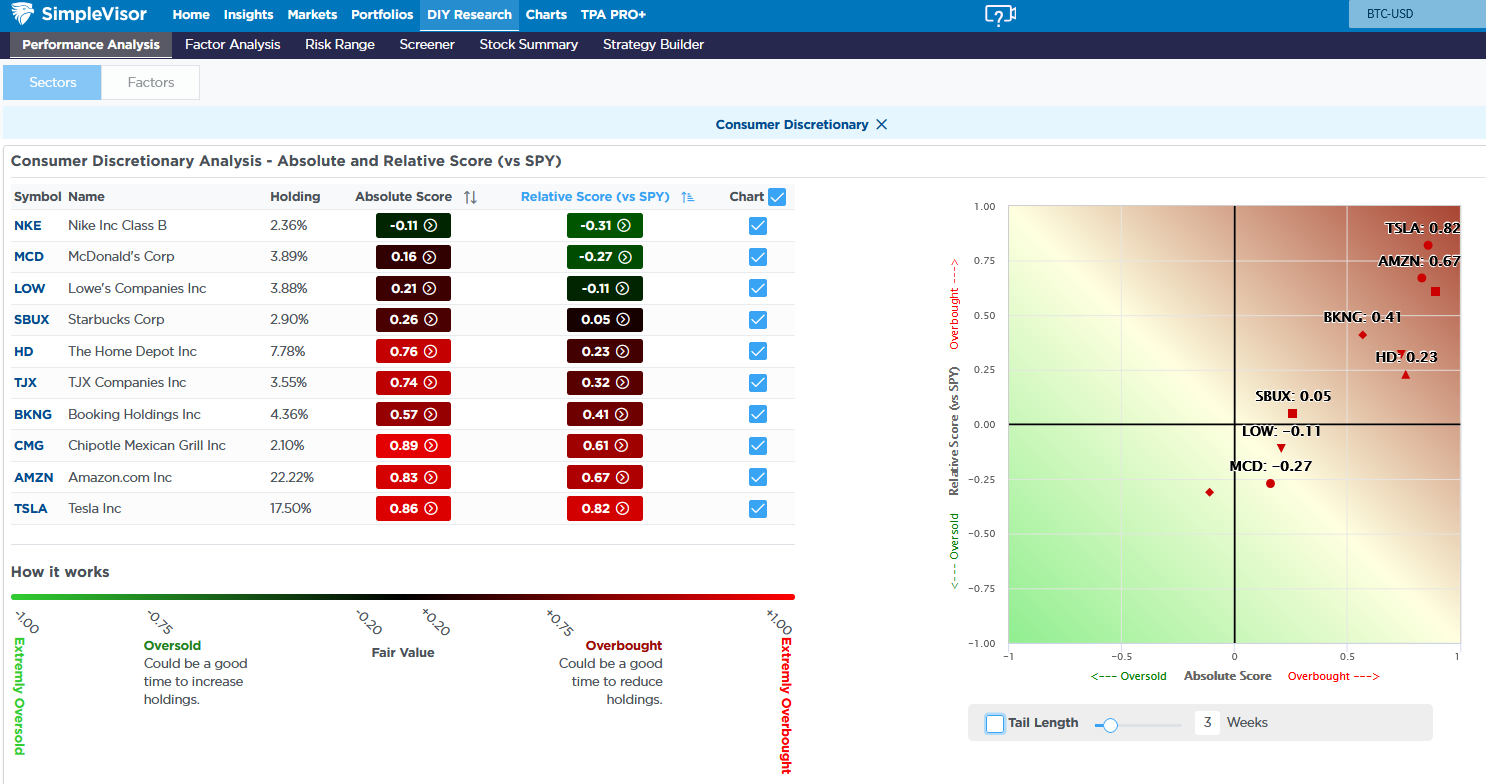

Tesla Fuels Discretionary Stocks

The first SimpleVisor table below shows that discretionary stocks are very overbought, both absolute and relative to the market. The culprits are Tesla and Amazon. The second table highlights the top ten holdings of the discretionary ETF XLY. Those two stocks account for nearly 40% of the ETF.

One can interpret the data in many ways. Here is our take:

We believe Tesla is riding Trump’s coattails. Given that Elon Musk is cozying up with the future president, investors must believe that the regulatory and political environment will be friendly to Tesla. Over the last month, Tesla’s shares have been up 11%, while competitors Ford and GM are each down about 7%.

Amazon, the internet retailer, is also very overbought. However, as shown in the second graphic, other retailers like Nike, McDonalds, and Lowes are trading poorly. This is likely linked to prospects for growing digital holiday sales versus less foot traffic at traditional brick-and-mortar establishments. Furthermore, Trump’s regulatory policies focus less on monopolistic enforcement than those of the Biden administration.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Housing Affordability Brings Market to a Standstill