Trending

A Wall Street axiom states that the stock markets lead the economy by about six months. While not a perfect predictor, the stock market reacts to investor expectations about future corporate earnings, economic activity, interest rates, and inflation. When sentiment shifts due to anticipated weakness in any of these areas, equity prices often decline, reflecting a reassessment of future growth.

This makes sense, given that investors are parsing earnings data and adjusting expectations that lagging economic data may not reflect as of yet. In “Failure At The 200-DMA,“ we noted that we focus on earnings because earnings and forward estimates reflect changes in the stock market’s risk assessment of all other events. To wit:

“Investors often get lost in the media headlines about rising recession risks, debts, deficits, or valuations. While those risks are important, they are terrible for predicting where markets will likely move next. Furthermore, if or when those risks become an issue, the market will begin to reprice for a reduction in forward earnings.“

Historically, significant market downturns have preceded nearly every major U.S. recession. For instance, in early 2000, the peak in the S&P 500 was months before the official recognition in 2001. In the lead-up to the 2008 financial crisis, markets began declining in late 2007. However, even though the recession officially began in December of that year, the declaration was not until December 2008. The COVID-19 crash in early 2020 was another example, with markets collapsing in anticipation of widespread economic shutdowns—well before the economic data caught up.

“The chart below shows the S&P 500 with two dots. The blue dots are when the recession started. The yellow triangle is when the NBER dated the start of the recession. In 9 of 10 instances, the S&P 500 peaked and turned lower before the recognition of a recession.“ – Failure At The 200-DMA

However, it’s important to distinguish between normal market corrections and actual recession signals.

Not Every Correction Is A Warning

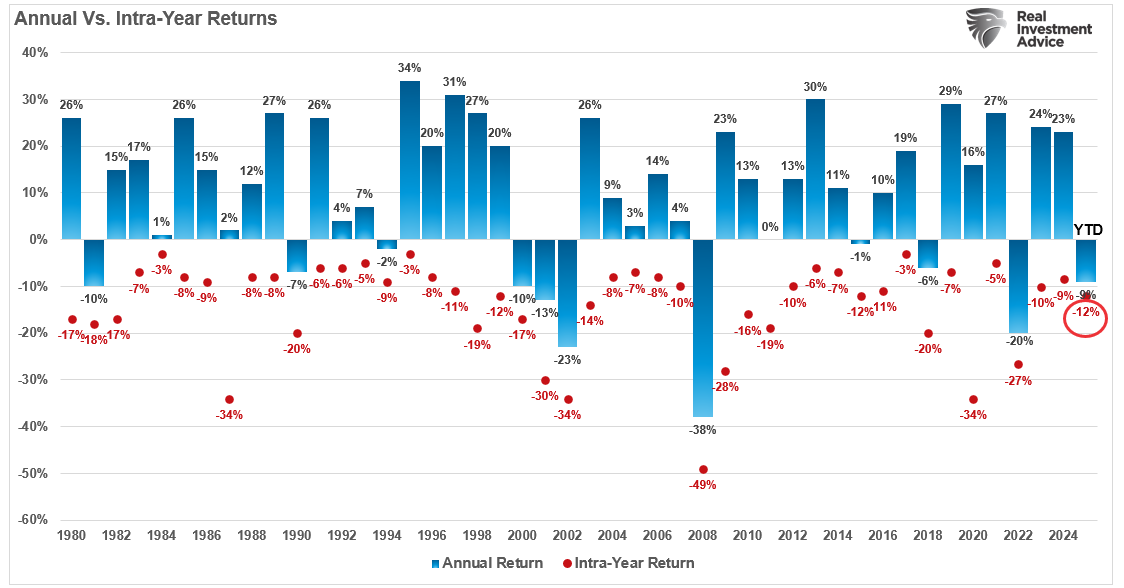

While entirely arbitrary, the market has long defined a correction as a decline of 10% or more from recent highs. Such corrections are common and occur about once a year.

During bullish years, corrections happen more often than you think. However, when corrections occur, it is not uncommon to see concerns about a “bear market” rise. However, historically speaking, the stock market increases about 73% of the time. The other 27% of the time, market corrections reverse the excesses of the previous advance.” – Bull Markets Often Have Corrections

The historical median correction is 10%, with a median gain of 13%. Given the frequency of 10% corrections, not every pullback indicated the onset of a recession. However, sometimes they are so we must not dismiss corrections entirely.

Corrections in the stock market can occur due to many short-term factors, such as geopolitical tensions, overvaluation, or shifts in investor sentiment. We are in no short supply of those factors. Today, investors focus on the impact of tariffs, sticky inflation, and elevated valuations. As expected, the stock market correction has already led to a reversal in both sentiment and valuations since valuations are a function of sentiment.

However, those factors are temporary and not necessarily linked to deeper economic issues. In contrast, if a correction deepens into a bear market, as the media defines it, a decline of 20% or more, and is accompanied by deteriorating economic fundamentals, the risk of a recession becomes more pronounced.

A Reversion To Reality

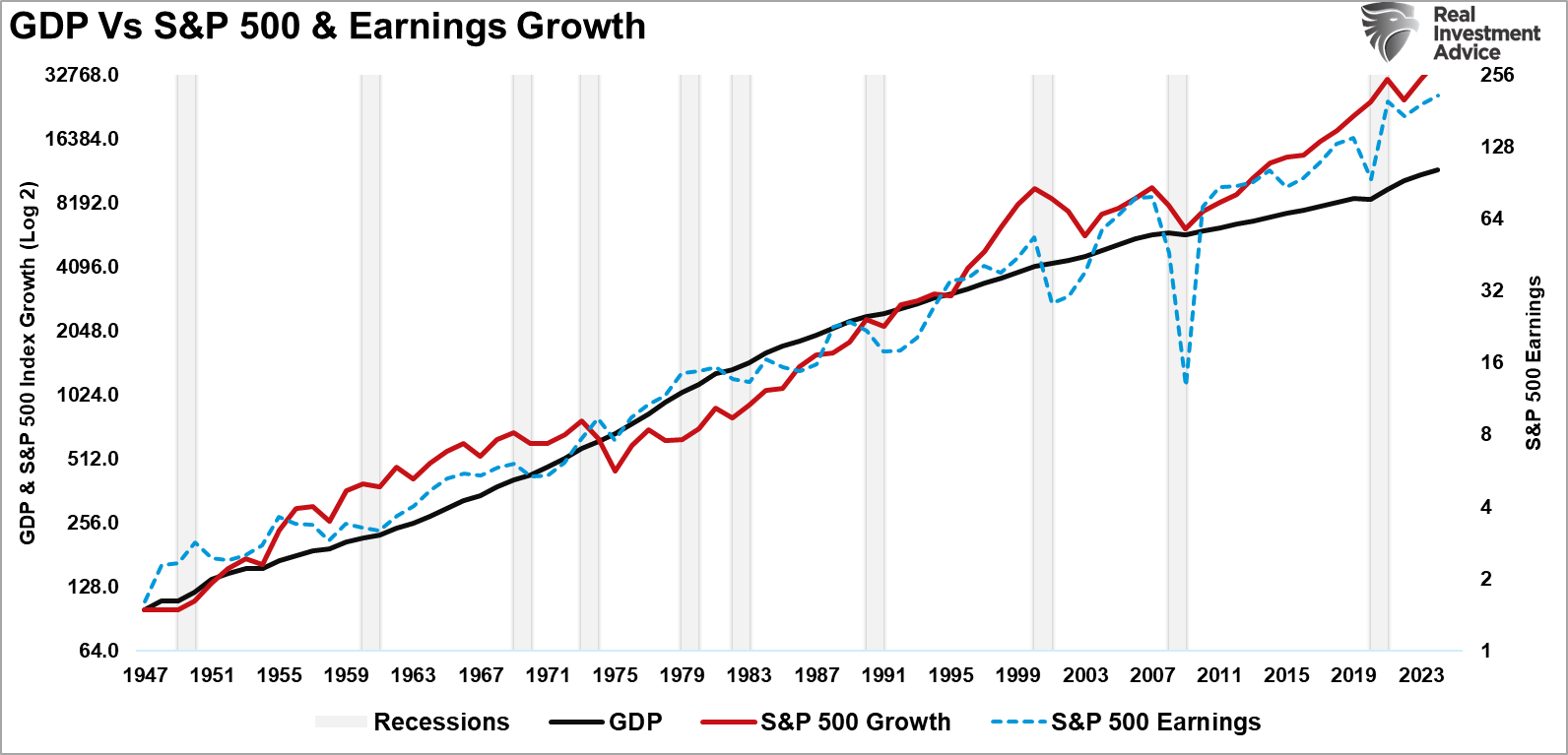

As discussed in “Stock Markets Are Detached From Everything,” market corrections eventually revert prices to underlying economic fundamentals.

“While stock prices can deviate from immediate activity, reversions to actual economic growth eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports. The market disconnect from underlying economic activity is due to psychology. Such is particularly the case over the last decade, as successive rounds of monetary interventions led investors to believe ‘this time is different.’”

While not precise, a correlation between the stock market and economic activity does remain. For example, in 2000 and again in 2008, corporate earnings contracted by 54% and 88%, respectively, as economic growth declined. Such was despite calls for never-ending earnings growth before both previous contractions. As earnings disappointed, stock prices adjusted by nearly 50% to realign valuations with weaker-than-expected current earnings and slower future earnings growth. However, both events were tied to other exogenous factors (Enron and Lehman failures) that exacerbated the decline.

Why is this important? The chart below notes that when markets and earnings significantly deviate from the long-term growth trend of the economy, they revert to the economy—not the other way around. However, not every reversion is linked to a recession.

As investors, it is crucial to understand that not every stock market correction is a recession warning. However, sometimes they are. The question is what indicators can warn us if the current market correction is “just a correction or a recession warning.”

What To Watch

There is no guaranteed method of determining whether a correction is just a correction or a warning of a recession. Much like Sherlock Holmes, we must follow a trail of clues and make assessments based on the data at hand. Several economic and technical indicators can help confirm whether a market downturn signals a recession.

Economic Warnings

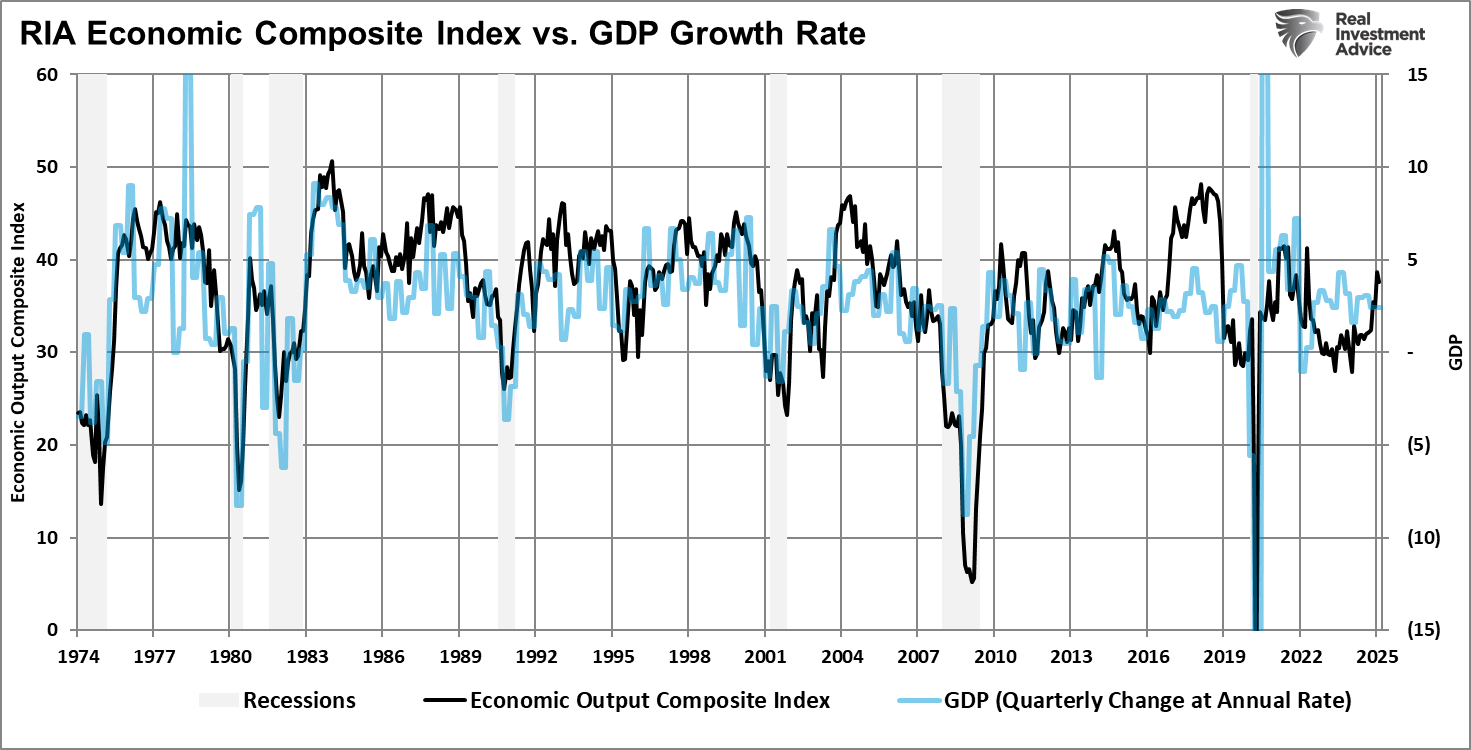

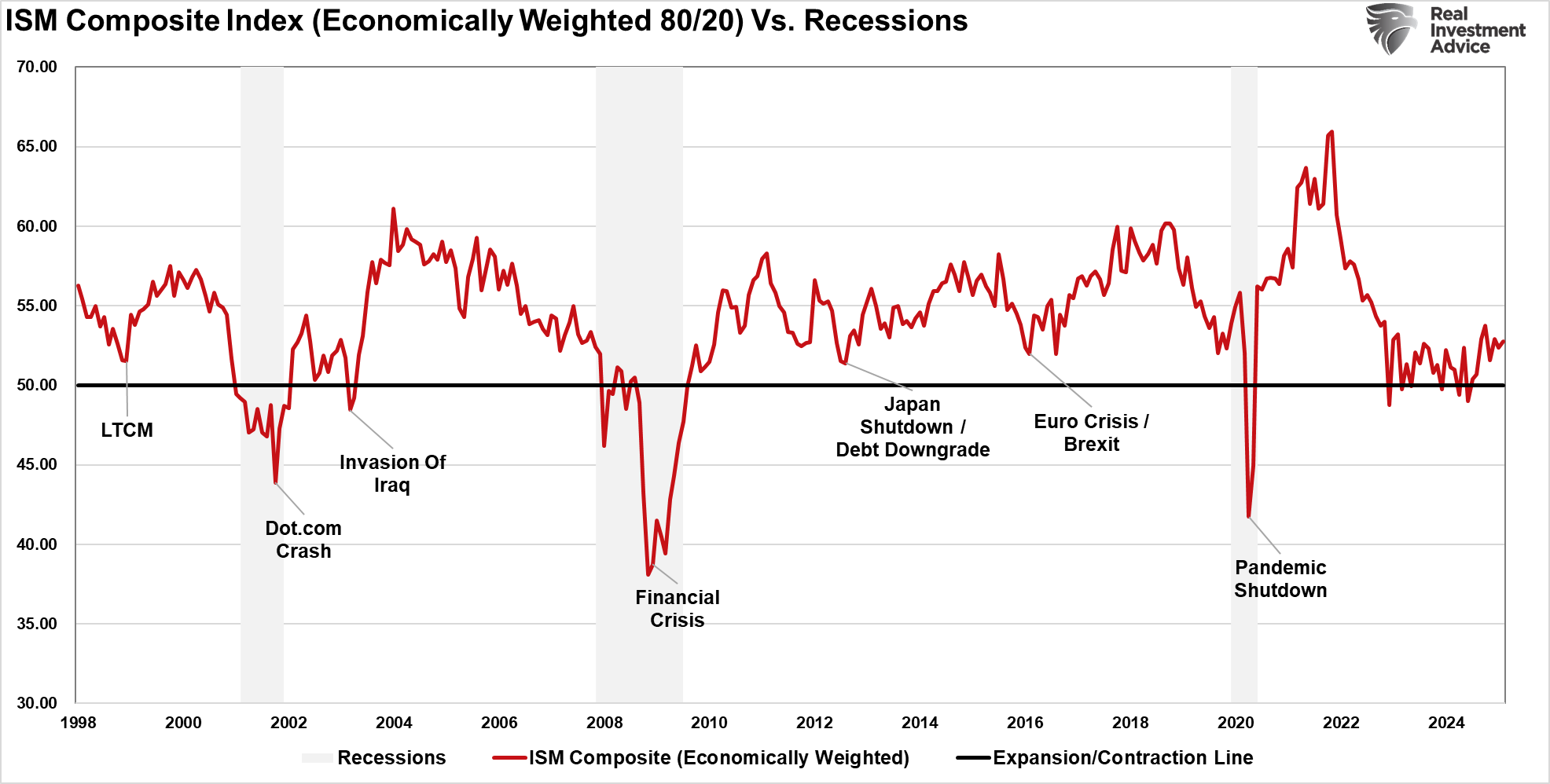

When it comes to economic data, investors must realize that much of the data runs with a significant lag, but some have a high correlation to economic outcomes. For example, inverted yield curves, falling leading economic indicators (LEI), weakening manufacturing and service-sector PMIs, declining corporate earnings guidance, and widening credit spreads are some of the best. When these factors align with a significant market decline, it often points to an economy on the verge of contraction.

There are currently very few economic signals warning of an economic contraction. For example, our Economic Output Composite Index, which comprises more than 100 different data points, including the ISM surveys and Leading Economic Indicators (LEI), is currently in expansionary territory.

Furthermore, if we weigh the ISM Manufacturing and Services Indices to the compensation of the economy, there is no current recessionary warning.

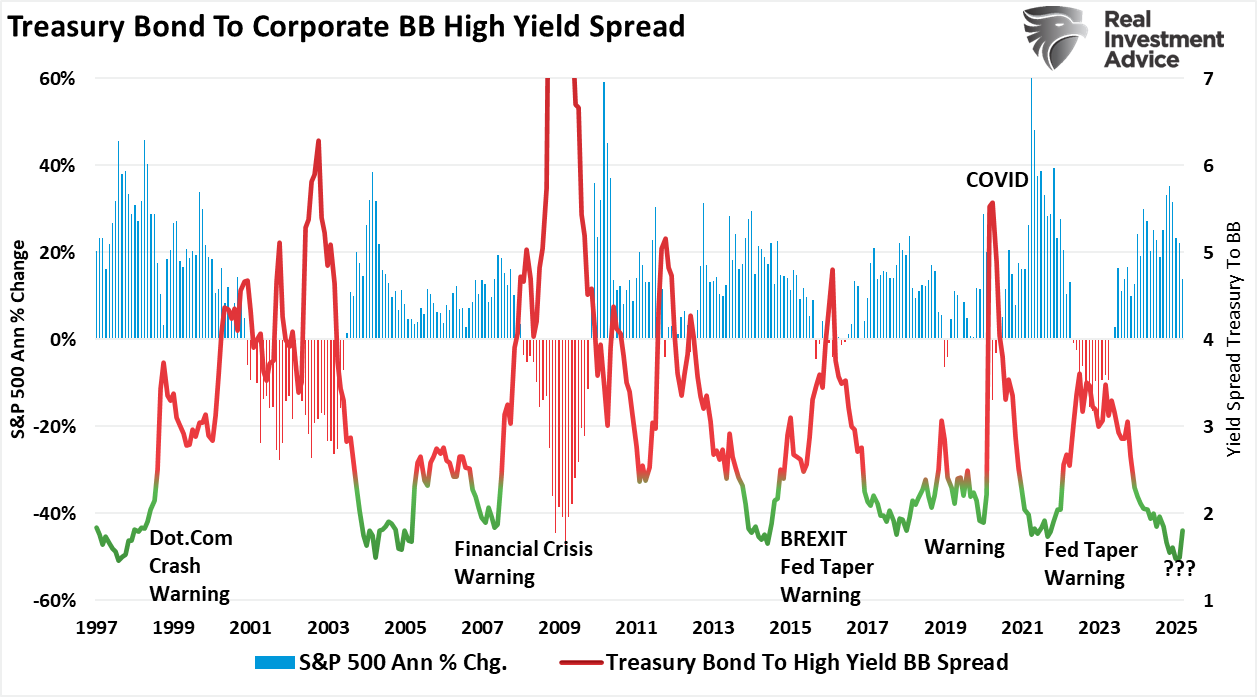

However, the most crucial indicator we watch is credit spreads. Credit spreads are the market’s early warning indicators if a correction will morph into a recessionary bear market. To wit:

“Credit spreads are critical to understanding market sentiment and predicting potential stock market downturns. A credit spread refers to the difference in yield between two bonds of similar maturity but different credit quality. This comparison often involves Treasury bonds (considered risk-free) and corporate bonds (which carry default risk). By observing these spreads, investors can gauge risk appetite in financial markets. Such helps investors identify stress points that often precede stock market corrections.”

The chart below shows the spread between corporate “junk” bonds (BB), often referred to as “high yield,” and the “risk-free” rate of U.S. Treasury bonds. While the yield spreads have ticked up modestly, this is commensurate with a market correction, not a recessionary warning.

However, as noted, all this data runs with a lag, and today’s readings can change tomorrow. This is why investors also need to pay attention to the technical warnings.

Technical Warnings

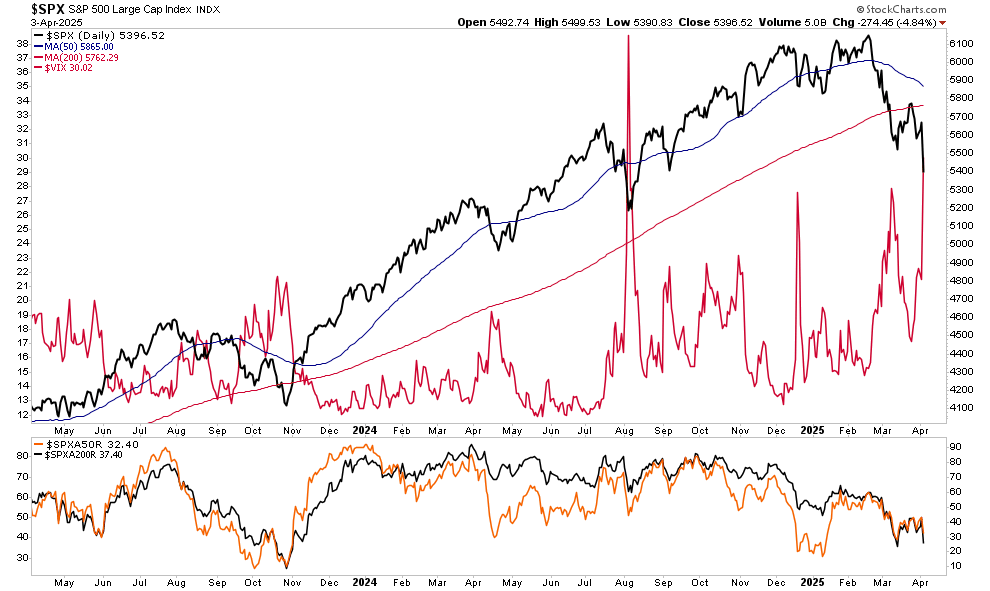

Several technical indicators warn that the current correction has the potential for something more. As shown, the market has broken below long-term moving averages, reduced market breadth (fewer stocks participating in rallies), and spikes in volatility (as measured by the VIX) often appear before recessions. Those conditions have been met technically, but the economic data does not confirm them —at least not yet.

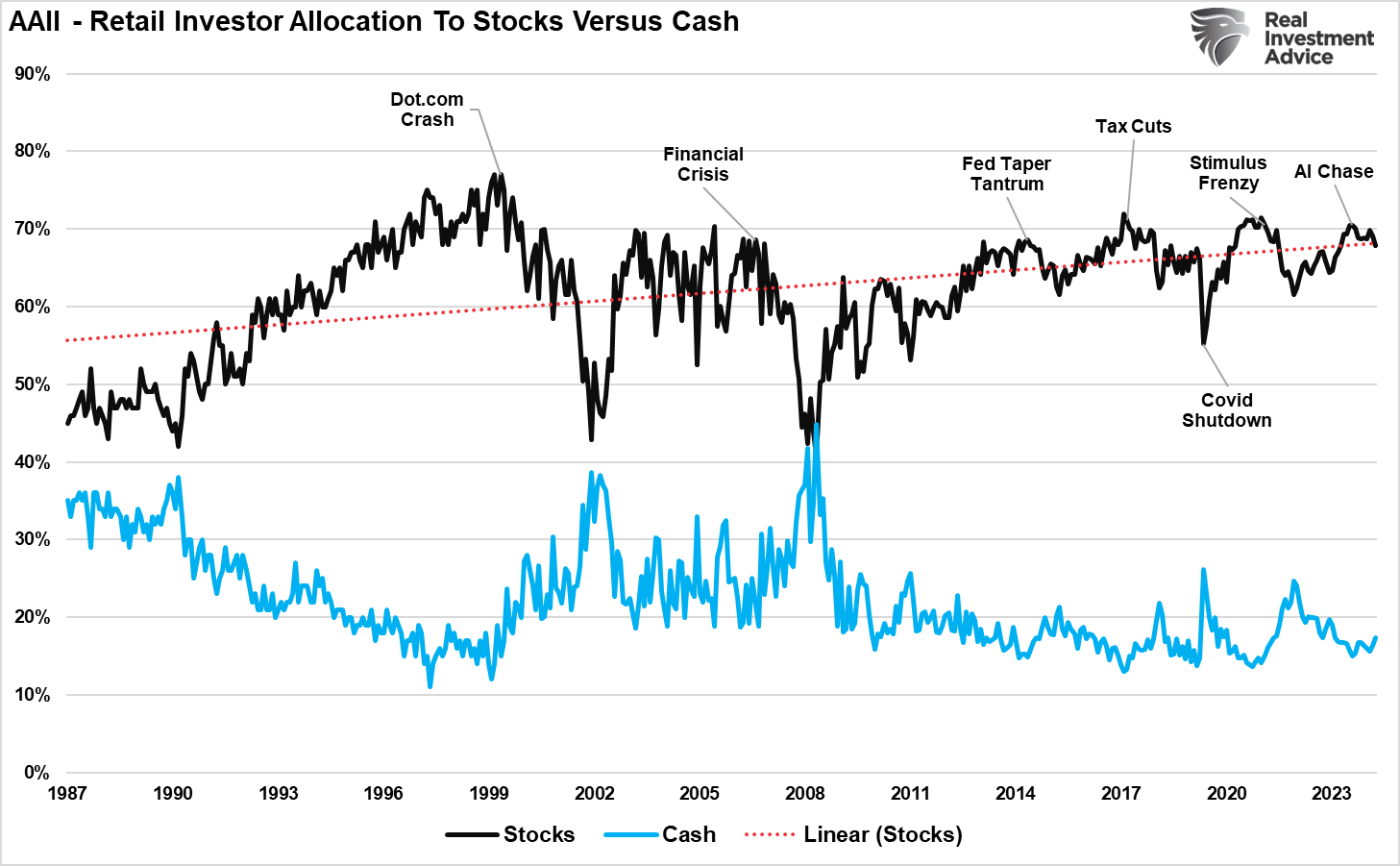

However, while investor sentiment has declined sharply, cash holdings remain very low. This would likely not be the case if market participants braced for tougher economic times, as we saw in 2000 and 2008.

Conclusion

The stock market’s value as a recession indicator lies in its ability to reflect future expectations. Those future expectations will be reflected in Wall Street’s expectations of future earnings, which are derived from economic activity.

“Looking at forward estimates, while there has been a minor cooling in the previous exuberance, analysts still expect a 16% annualized growth rate in earnings into next year. Unless those estimates begin to reverse sharply, it is unlikely that the current correction will devolve into a deeper corrective cycle.”

Yes, the markets are occasionally prone to false alarms or overreactions. However, the stock market does respond faster than lagging economic data, which is often revised long after the fact. Investors who understand the relationship between market movements and broader economic trends are better positioned to manage risk and make informed decisions.

Rather than react emotionally to every market dip, investors should evaluate whether the sell-off is driven by fundamental weakness or short-term noise. When a broad market decline is accompanied by deteriorating earnings, slowing growth, and weakening economic indicators, the likelihood of a recession increases. In such cases, adopting a more defensive investment strategy, diversifying across asset classes, and maintaining a long-term perspective can help weather economic downturns and preserve capital.

Related: Solving Trump's Economic Crossword: Inflation Clues and Rate Cut Answer