Trending

S&P 500 closed Friday on a strong note, and as the holiday-shortened week is usually accompanied by positive seasonality, it would be reasonable to expect extension of gains. Is therre any show stopper at the moment? Credit markets are strong and in a risk-on mode – but what about the odd strength in long-dated Treasuries? Are the stock traders getting it right – or the bond ones? Remember that such divergencies can take a long time to resolve, and don‘t require immediate action. It‘s the same with the Industrials and Transports in the Dow theory. So, don‘t jump to S&P 500 bearish conclusions just yet.

The stock market advance is characterized by improving market breadth, and a fresh push of reflationary trades. It would have been all too easy to lose one‘s cool post the June FOMC, and declare value to have topped – while tech amply helped by heavyweights powers the S&P 500 advance, value performance ain‘t too shabby. Even financials are weathering relatively well the retreating yields pressure, counterbalanced by the Fed relaxing share buybacks and dividend rules. Real assets including energy are surging again, and the Fed‘s bluff is being called.

Little wonder when all the central bank did, was influence inflation expectations, and precisely nothing about current inflation – let alone pressures in the pipeline. I‘ve discussed the cost-push pressures building up, leading to inflation becoming unanchored. Add job market pressures beyond the difficulties in hiring, and the issue grows more persistent. While it‘s not biting overly noticeably for the financial markets to take notice the way they did in Mar and early May, left unattended, inflation would come to bite in the not so distant future. The takeaway is that with the constant redefinitions of what transitory should mean now, the concept of Fed as inflation fighter is subject to well deserved mockery.

Look for the lull in Treasury market to continue, it‘s almost goldilocks economy as the monetary and fiscal support rivals wartime footing circumstances. Makes you wonder what would be on the table if we were faced with a recession. Thankfully, that‘s not on the horizon – we‘re in a multi-year economic expansion that won‘t end with the tapering or tightening games this year or next, not in the least.

As I wrote on Friday, thinking also about the value strength:

(…) accompanied by the Treasury yields‘ inability to retreat further. Near the top of its recent range, the 10-year Treasury yield is trading within the summer bond market calm atmosphere, and so are the beaten down inflation expectations at a time when the dollar is catching a strong bid.

Notably, commodities haven‘t been derailed in the least, so pay no attention to lumber – the real assets‘ world is much richer and profitable.

Remember the big picture – fiscal stimulus very much on, monetary accomodation aggressive, no worries about the economic expansion slowing down. Pickup in economic activity associated with inventories replenishment is sure to be kicking reliably on. Open long profits in the S&P 500 and Nasdaq can keep growing!

Precious metals are duly reacting today to the pressures to go higher, building up for weeks. Look for miners to confirm the upswing that isn‘t going unnoticed in the commodities arena either.

Crude oil took off on the absence of OPEC+ deal, but I am looking for it to base in the $70s before we see triple digit crude prices next week. The Brent crude lag looks a bit suspicious to me, so a little breather might be in order here.

Crypto bears are getting a beating, with the odds favoring upswing to continue – the Ethereum outperformance of Bitcoin is conducive to the accumulation thesis I had been mentioning for weeks.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

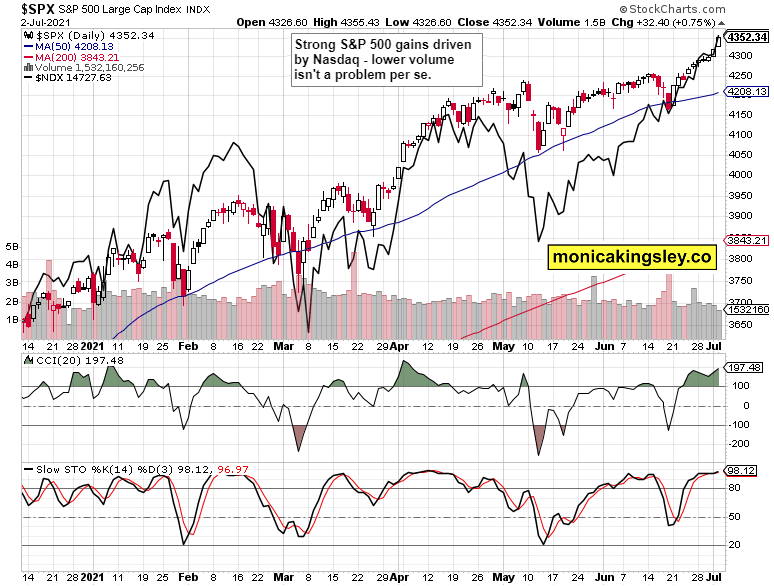

S&P 500 and Nasdaq Outlook

S&P 500 is going higher, and so is Nasdaq. The decreasing volume might usher in a little consolidation over time but there is no imminent reason to call for one today.

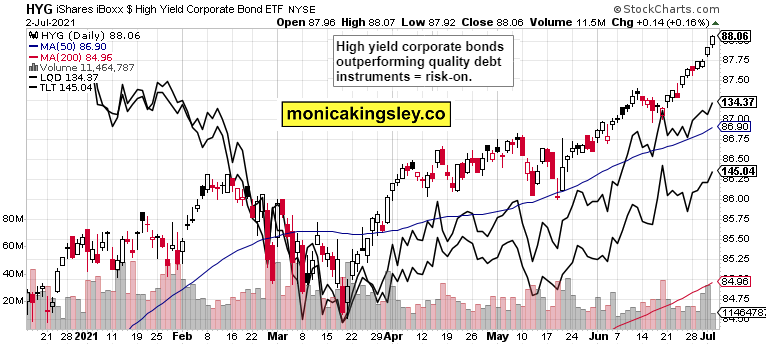

Credit Markets

Credit markets performance remains strong across the board, but I am looking for TLT to face headwinds soon.

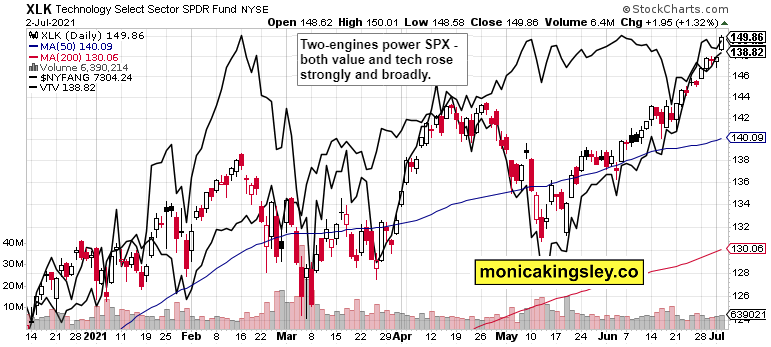

Technology and Value

Tech is up, value is up – what else to wish for? Defending the gained ground, that is.

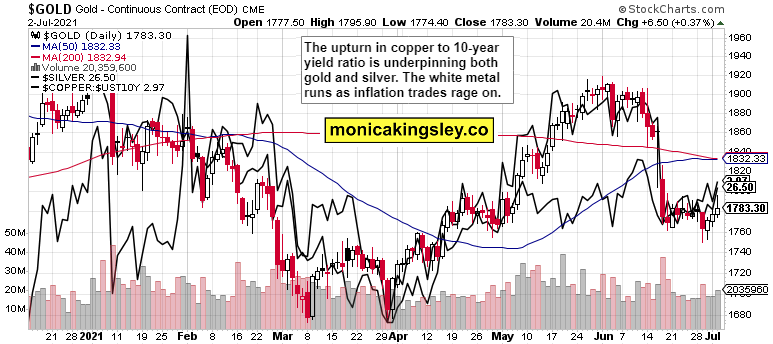

Gold, Silver and Miners

Gold is attempting to go higher, and based on the yield-inflation spread getting ever more compressed and a tad off inflation expectations, I‘m looking for miners to confirm the upcoming gold advance.

Silver and copper are also building energy to go higher, and it‘s my view they would surge to recapture a good portion of the post FOMC decline before taking a breather.

Bitcoin and Ethereum

Strong base building in the cryptos continues, and the bulls have the tactical advange at the moment.

Summary

S&P 500 keeps trading near its highs, with a bullish bias, characterized by sectoral rotations and improving market breadth including in Nasdaq. A little sideways consolidation appears looming, but I am looking for a positive week.

Gold and silver bulls are getting ever more strongly on the move, and Friday‘s upper knot is a preview of things to come – the depressed nominal yields with unrelenting inflation are helping attract buying interest.

Crude oil enjoyed more than its fair share of good news, but remains bullish today‘s tremors notwithstanding. Great future ahead for black gold, the Saudi Arabia – UAE spat regardless.

Bitcoin and Ethereum bulls are the favored side these days as the weekly charts posture isn‘t yet in jeopardy. The basing pattern looks to be one of accumulation rather than distribution.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for all the four publications: Stock Trading Signals, Gold Trading Signals, Oil Trading Signals and Bitcoin Trading Signals.

Related: Roaring Comeback of Reflation and Commodities

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.