Trending

A Super-Efficient Portfolio as a Foundation for the Disciplined, Purpose-Focused Investor

A once-in-a-lifetime pandemic has unleashed economic chaos about the globe. Economic success in one country seems to elude another. Weak economic indicators don’t seem to affect stock markets meaningfully one day until they do the next. As a result, financial professionals, economists, and investment experts, who have never seen anything like it, are grasping at straws to predict what comes next.

Tactical moves to protect a nonprofit’s endowment or one’s personal investments could give peace of mind in the short-term but be disastrous in the long-term. Instead, employing a strategy based on the fundamental principles of investing is a more effective approach.

Enter the Global Market Portfolio

The Global Market Portfolio represents all assets—stocks, bonds, real estate, commodities, and other investments issued by governments and corporations—weighted in proportion to their relative market values. The beauty of the Global Market Portfolio is that can be used as a starting point for any investor, regardless of risk appetite. Dial down risk by holding more cash; dial up risk by holding less. And while it won’t be the best performing portfolio on the block or even the most consistent, that’s the whole point. Whether for a nonprofit endowment or personal retirement, of all possible portfolios the Global Market Portfolio delivers the most return for the lowest risk as theorized by three renowned Nobel laureates.

A Tale of Three Nobel Laureates

Three prominent Nobel Prize winners, instrumental in the study of investing, are also credited with understanding the benefits of the Global Market Portfolio.

It all started in 1952 with a young economist named Harry Markowitz [1], who theorized that a portfolio of uncorrelated assets—in other words, assets whose prices react differently under similar environments—could be optimized such that:

- return is maximized and

- risk is minimized.

Return is defined as increases in value and risk as the unpredictability of prices usually represented by standard deviation. His work is the basis of Modern Portfolio Theory or MPT.

Then in 1958, a Yale professor named James Tobin [2] explored the concept of economic utility, or financial usefulness. Based on Markowitz’s MPT concepts of maximizing expected return based on a given level of market risk, Tobin suggested that there exists only one super-efficient portfolio in which a reasonable level of return can be achieved at a reasonable level of risk. Portfolios with more risk and less return would be rejected by investors, no matter their risk tolerance.

The economist William Sharpe, in his 1964 paper [3] on the Capital Asset Pricing Model and the analysis of market risk, revisited this super-efficient, optimal portfolio. He suggested there was a market equilibrium where return and risk were optimized and this could be achieved by holding all the stocks and bonds in the world in proportion to their relative values.

Global Market Portfolio in Theory

If you were actually able to invest in every investable asset in the world, what would the portfolio look like?

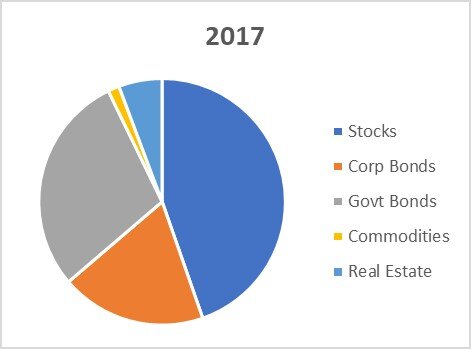

Ronald Doeswijk, Trevin Lam and Laurens Swinkels [4] have focused their research on estimating the Global Market Portfolio’s asset proportions as well as its average return over time. According to their most recent estimates of the value of outstanding shares, or in other words market capitalizations, the portfolio consisted of approximately 45% stocks, 48% bonds, 6% real estate and 1% commodities (Table 1).

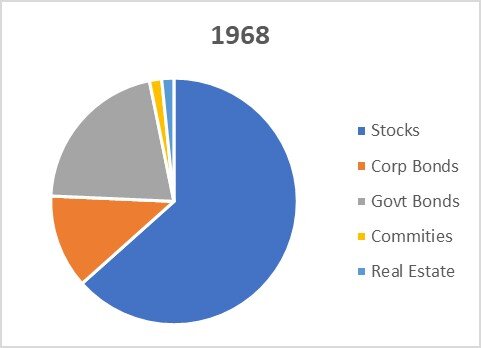

The Global Market Portfolio’s market capitalizations are not static and instead move with changes in the market. For example, over the timeframe analyzed (1960 – 2017), the stock percentage was at a high in 1968 with an allocation of 63% (Table 2).

The compounded average nominal return for the Global Market Portfolio over the period 1960 – 2017 was 8.36% with a standard deviation of 11.2%. Compare these results to the global broad market of stocks, which returned 9.76% in the same period with a standard deviation of 17.3%. To understand the relative risk between the two, the worst performance for the Global Market Portfolio in the timeframe was -24.2%, while for broad market of stocks it was -43.4%.

The Global Market Portfolio in Practice

While there is no practical way to buy the whole universe of investments, an investor can approximate it by using index funds. An investment index is a statistical tool that measures asset prices over time for a particular subset of the market. The Dow Jones Industrial Average and S&P 500 Index are major stock indices, while the Barclays Bloomberg Aggregate Index is a major bond index. An index fund is constructed to reference and track a particular index in order to replicate its return as closely as possible. The proliferation of index funds over the last fifteen years has given investors access to almost all corners of public capital markets in order to construct a close approximation of the Global Market Portfolio.

The Global Market Portfolio may not be right for everyone. Investment portfolios with a very short time horizon may need something more liquid. The active speculator looking for a moonshot will not be satisfied. Investors looking for a long-term strategy suitable through thick and thin, however, should give it a serious look.

Related: Redefining Electable: Nonprofits Building a Better Political Candidate Pipeline