The Fed’s monetary policy has screwed Americans. Such is the basic premise of a recent Washington Times article discussing inflation. To wit:

“Do you find it odd that banks and other financial institutions provide mortgage loans to millions at an approximately 3% interest rate for 30 years, while the government reports that inflation is over 6% at an annual rate and rising? Are you frustrated that you are a responsible and prudent person who saves for a ‘rainy day’ or retirement, and your savings account only pays 1% or so interest, while inflation is many times that? Do you find it odd that the government official most responsible for inflation – Treasury Secretary and former Fed Chairman Janet Yellen – several months ago told us that inflation would be mild and transitory, neither of which has turned out to be correct? Do you suspect that she may not know what she is doing, particularly when she says that more record government spending will bring down inflation?”

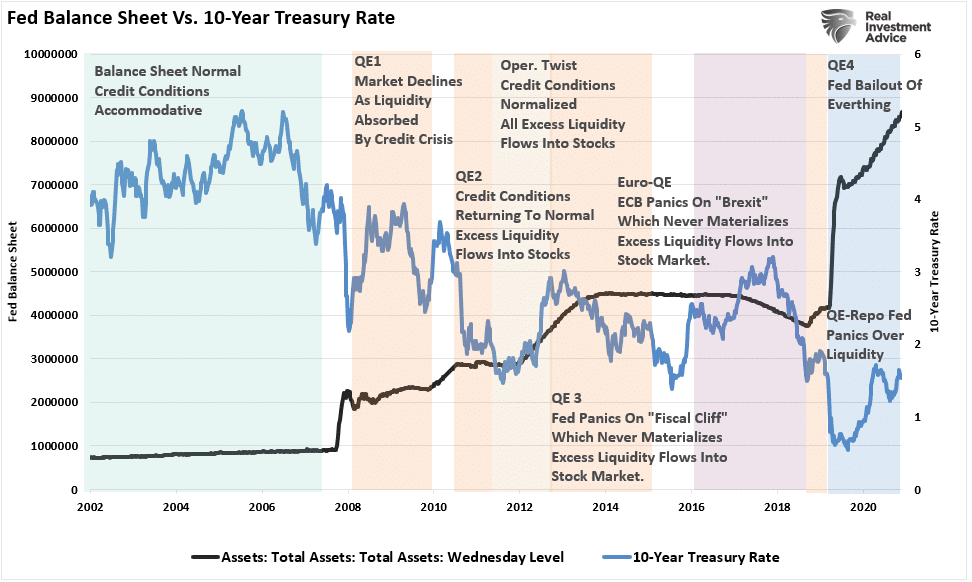

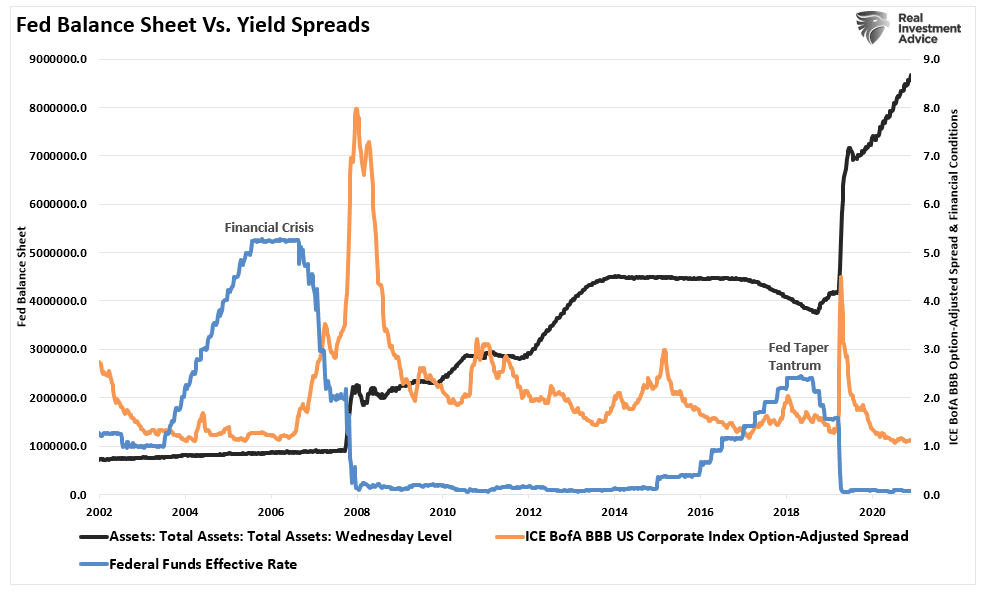

There is a lot of truth in that statement. However, it is not just Janet Yellen’s fault. The problem lies directly with the Fed’s monetary policy decisions implemented since the turn of the century, and particularly, the Financial Crisis. As each bailout of the financial system occurred, yields fell along with inflationary pressures and economic growth.

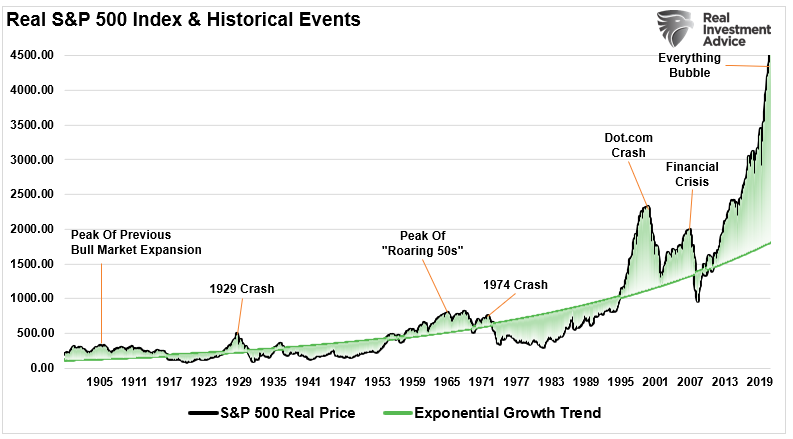

Of course, as discussed in “Fed Issues Stock Market Warning,” the only thing the Fed succeeded at was inflating a “valuation” bubble of epic proportions.

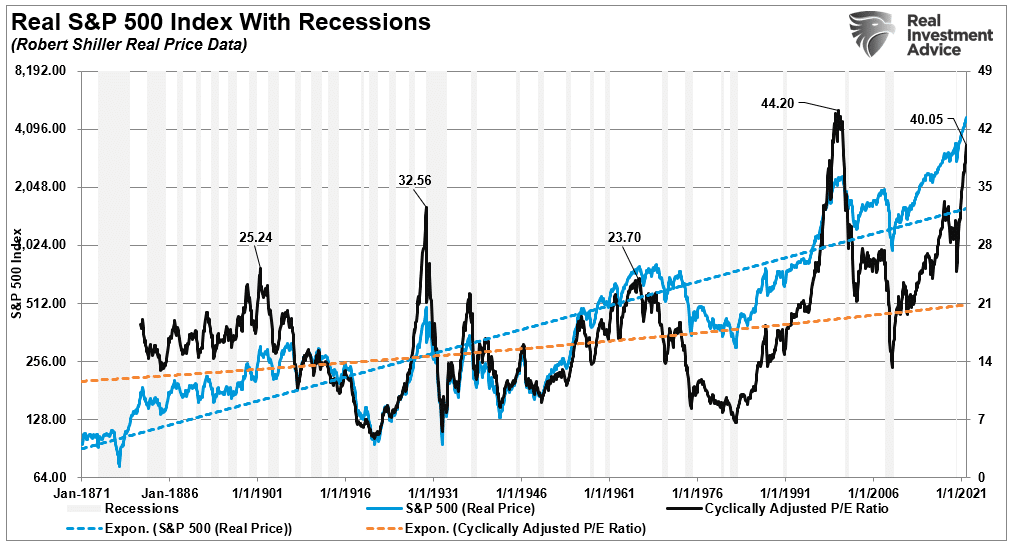

At 40x trailing earnings, current valuations are higher at the peak of the market in 1999.

Savers Have No Choice

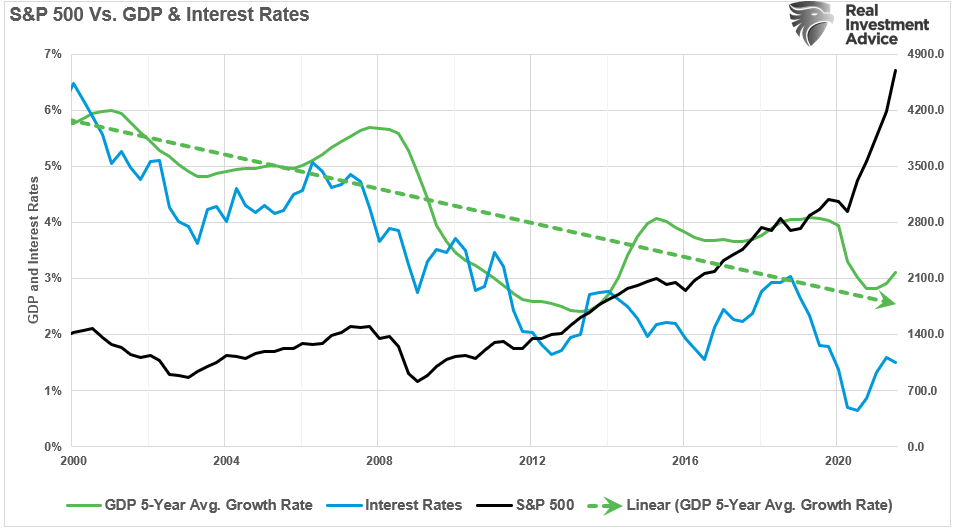

The Fed’s monetary policy was designed to force “savers” out of cash, into “risk” assets. Such, the Fed believed, would increase confidence and support economic growth. However, as shown, while stock prices surged, economic growth and interest rates fell.

Such is a critical point.

Most individuals are attempting to “save” money in order to reach their financial objectives. As “savers” we have three primary responsibilities:

- Have an appropriate savings rate for our goals,

- Ensure those savings adjust for inflation over time, and;

- Don’t lose it.

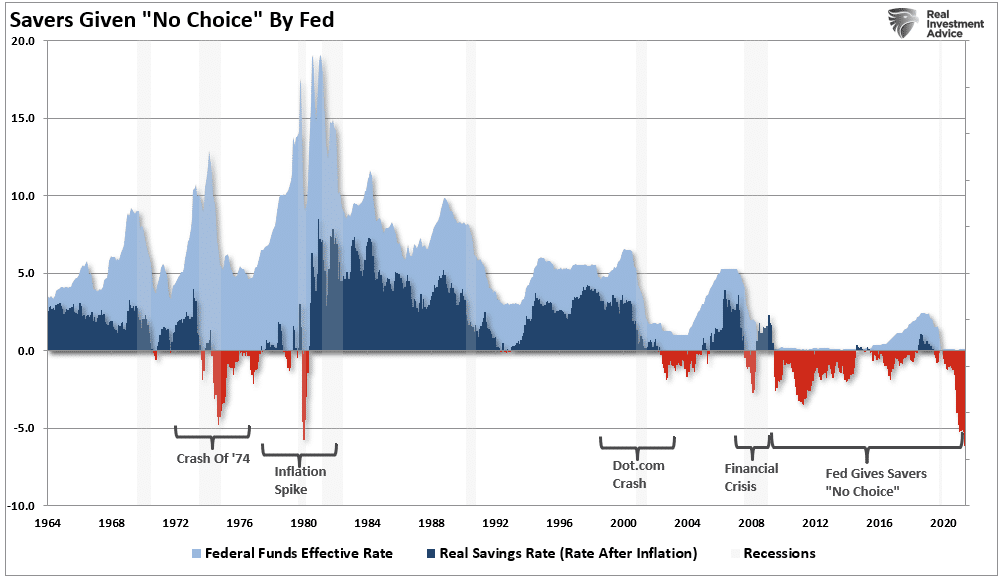

There have been plenty of times in history where you literally could stick your money in a “savings” account and earn enough, “risk-free,” to “save” your way to retirement. The chart below shows the savings rate on short-term deposits adjusted for inflation.

There are two notable points to be made.

- Real savings rates have remained primarily negative since the Financial Crisis. Such was due to the Fed’s massive interventions and artificially pushing interest rates towards zero.

- Based on current inflation rates, the “real savings rate” is now as negative as it was in the late 70’s during the the “Arab Oil Embargo.”

With “real savings rates” pushing a negative 6%, the Fed’s monetary policy has given individuals little choice.

Nothing But Risk

For investors who have money invested in the financial markets, the Fed’s actions had one very predictable outcome. By keeping interest rates pegged at zero for nearly a decade, the Fed forced “savers” to take on more “risk” for even a marginal rate of return to pace inflation.

An article by The American Institute noted this point:

“In fact, risk tolerances are up across the board. There are anecdotes, of course, but the evidence is clear in trends of some of the most historically risky markets. The stock market, once a fairly mid-range option for risk and return, has gone from a complement to a substitute for the role that bank accounts or Treasury bonds once filled.“

For example, investors are now taking on far more risk in “credit” than they get compensated for. Such has been the legacy of the Federal Reserve interventions since the turn of the century. When those rates did reverse, it was not a favorable outcome for investors

Given a decade of monetary interventions, investors came to believe “risk” was permanently mitigated by the Fed. For that reason, investors piled into both “credit and equity risk” with extreme exuberance. The deviation from the long-term exponential growth trend shows this.

What you should take away from the chart above is apparent. Investing capital when prices are exceedingly above the underlying growth trend repeatedly had poor outcomes. For “savers,” putting capital into “equity risk” at peak deviations repeatedly led to long periods of ZERO returns. Not exactly the savings goal most are needing.

However, the “chase for yield,” is entirely understandable. When money market yields, bond yields, and equity yields are near zero, “There Is No Alternative.”

It’s A Lose-Lose Game

Investors are currently playing a “Lose-Lose” game.

- If they fail to chase “risk,” they suffer the loss of return, not to mention the psychological beating from the financial media, to adjust their savings for inflation.

- If they do chase risk, the odds are high that at some point, a reversion will occur that will take away a large chunk of their assets.

Such was the conclusion from the American Institute:

“The Federal Reserve has done more in the past 25 years than its founding legislators ever conceived. With that in mind, one wonders what the end game is, especially in light of two facts.

- First, the inclination of monetary authorities the world over is toward lower and lower thresholds for intervention.

- Second, fiscal and monetary policies have a way of suddenly finding limits when the tax-payers are on the receiving end.

If there is a component of the growing disposition for risk inspired by the idea that the Fed will swoop in to save retail investors from failed ETFs, collapsed SPAC prices, a wave of microcap stock delistings, or any other consequence of their understandable but reluctant march up the risk curve, it is ill-advised.

Any lasting solution is far more likely to come from markets themselves.”

I would carefully consider the last sentence.

So What Do You Do?

It’s a tough question that few have an answer for.

The financial media suggests, regardless of your age, that investing in equities is your only option. Bonds have historically provided some yield with a return of principal function in the future, but with inflation those yields are negative.

We don’t have a good answer for you.

The Fed has given “savers” no “risk-free” choice for saving for their future.

The problem with “savers’ taking on excessive levels of equity risk, as we see today, is the eventual outcome is far worse than most expect.

Will this time be different?

Maybe. But I wouldn’t bet my retirement on it.

Related: Inflation vs. Deflation: Which Is the Bigger Threat in 2022?