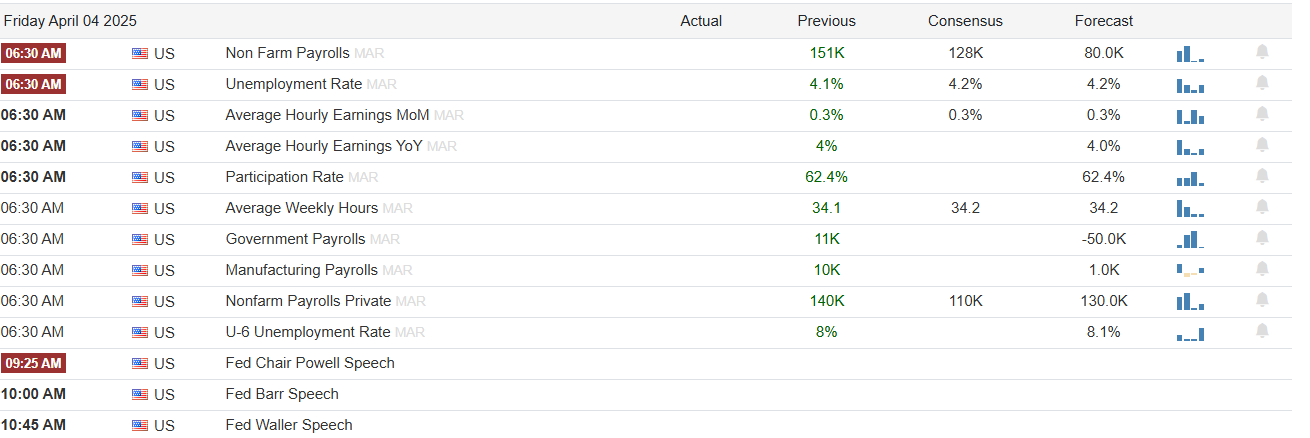

Trending

Heading into April 2nd, investors were under the impression that Trump’s goal was to set tariff rates that allow for fair trade with other nations. Trade impediments like tariffs, taxes, VATs, currency manipulation, and other methods that don’t allow for fair trade would be offset with tariffs. More simply, Trump would level the playing field. Instead, as we detail in a section below, the tariffs are based on trade deficits, which are partly due to unfair trade practices but also the result of many other factors. Based solely on Wednesday’s actions, it appears Trump is aiming for equal trade. Fair and equal trade may sound alike, but they aren’t. Equal trade seeks to end trade deficits and surpluses as nations buy and sell equally to each other. This goes against the economic theory of Comparative Advantage.

Economist David Ricardo developed the theory of Comparative Advantage in the early 1800s. Ricardo states that countries should specialize in producing and exporting goods and services they can make most efficiently (i.e., at a lower relative opportunity cost) compared to other countries. Doing so maximizes economic efficiency and global welfare, as resources are put to their most productive uses.

The tariffs announced on Wednesday are likely worst-case scenarios. We think negotiations will result in lower tariffs in many cases. Accordingly, we hope the ultimate result is fair trade, not equal trade.

What To Watch

Economy

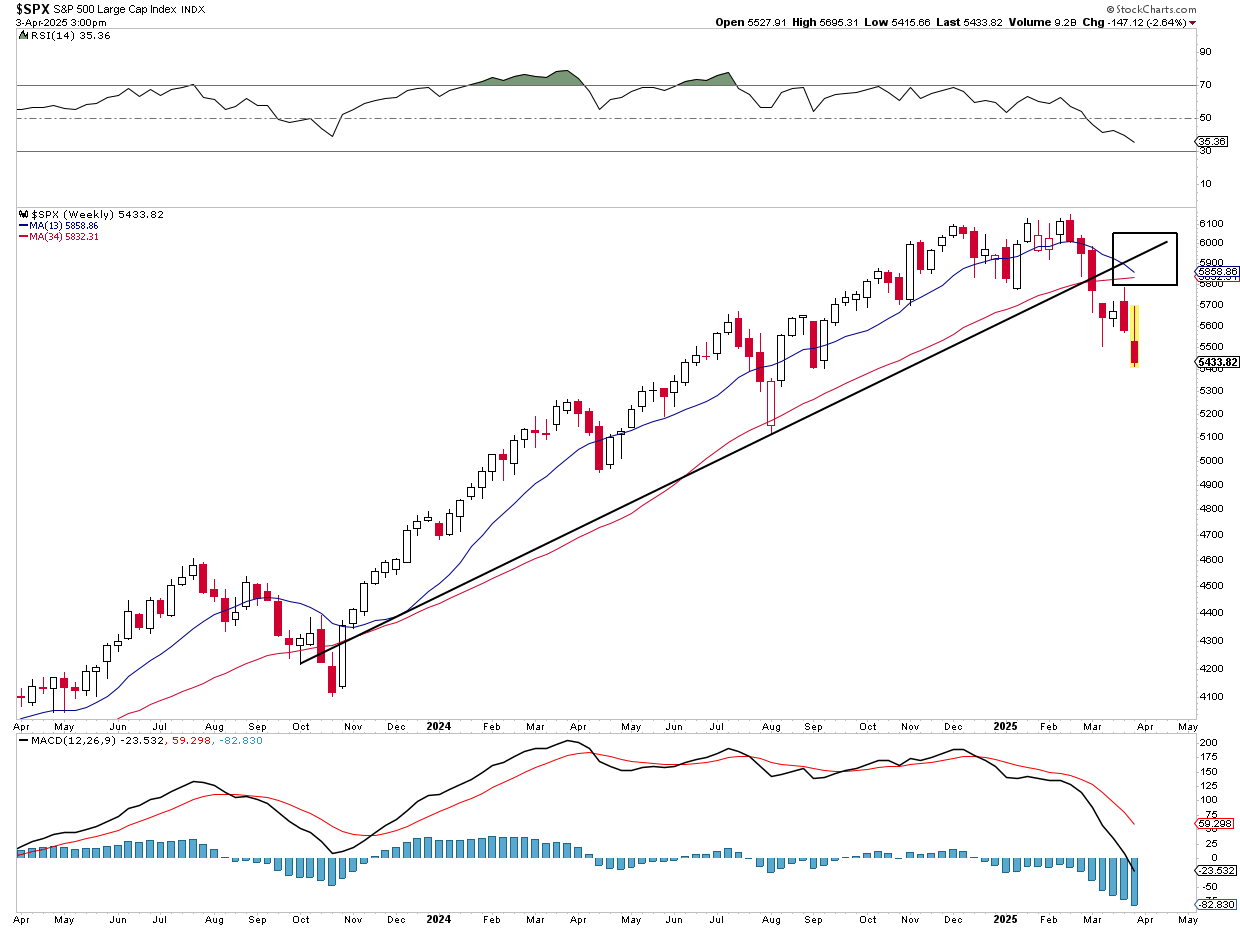

Market Trading Update

Yesterday, we discussed the weekly sell signal, which would suggest that a larger corrective cycle is underway. Yesterday, the “worse-than-anticipated” tariff announcement from the White House sent stocks sharply lower as analysts scrambled to reprice the risk to earnings and valuations. While the decline was meaningful, it has not triggered a “sell signal” as of yet. However, with that said, it is almost inevitable that the signal will trigger by the end of next week. However, this signal suggests that we should cut the risk to equities when these signals are triggered, but markets will generally be oversold enough for a short-term rally. Given the deeper oversold conditions that currently exist, that rally could be fairly substantial but I would not expect more than a retracement to the longer-term moving average at 5800. While a 400-point rally in the market will increase bullish sentiment, we must remain disciplined and reduce exposure accordingly.

Notably, while the volatility indexed spiked on the tariff news, it did not rise higher than we saw during the initial 10% decline in the market. Given the magnitude of the tariff surprise, I would have expected to see a volatility spike similar to what we saw during the “Yen Carry Trade” blowup in August of last year. With the market oversold on various measures short-term, a reversal of volatility would help lift markets higher. Again, I would not expect more than a retracement to the 200-DMA around 5750ish.

Our recommendation is to use any rally to reduce portfolio risk as needed. Consider a shift towards value, increase bond exposure, and hedge as needed. Critically, this is not about getting back to precisely 5750-5800 to take action. There is increasing risk to the market in the near term, so take action as the market rises. Otherwise, you might be caught in a situation where the exit was in hindsight.

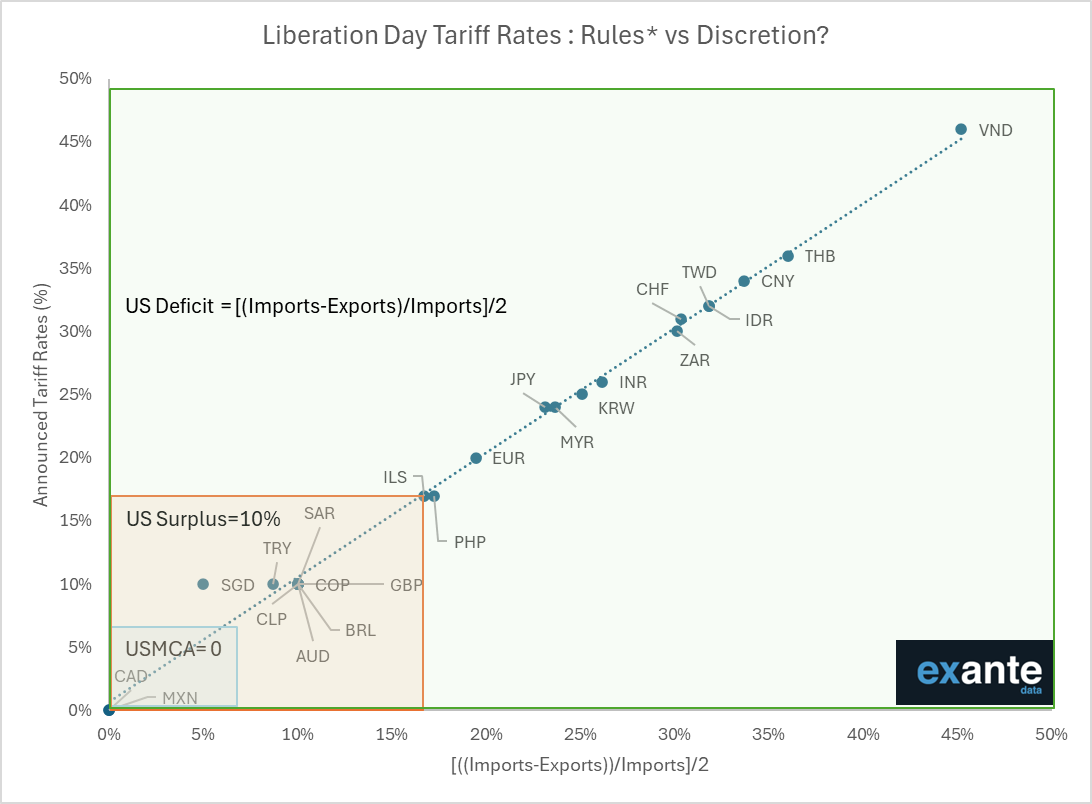

Tariff Rate Calculations

Shortly after the tariff rates were announced, the math behind the calculations was revealed. Thus, we have learned that the administration took the US trade deficit with each country and divided it by our imports from that country. The chart below shows predictions based on the formula plotted against the new tariff rates.

This calculation divides the deficit by two to get the tariff rate. Consequently, the goal is not necessarily zero trade imbalances but reduced trade deficits. We reiterate that this is the first volley of what is likely to be a series of negotiations.

Fed Easing Odds Increase

The Fed is in a bind. The tariffs are likely to result in slower growth. Hence, the Fed would be more likely to cut rates. However, the immediate consequence could be higher prices, thus they may be apprehensive about cutting rates. While the market is still digesting the tariffs, the initial market vote is that rate cuts are more likely.

The graph below shows the futures contract for December Fed Funds. The expected rate is calculated by subtracting the price from 100.00. As shown, the expected rate of Fed Funds in December fell by .14% (96.40 to 94.54) on Thursday morning. Accordingly, the market is now expecting another half of a rate cut by year end. The odds of rate cuts are likely to be volatile.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: The Tariff Impact in One Graph