Trending

Written by: Ivan Martchev

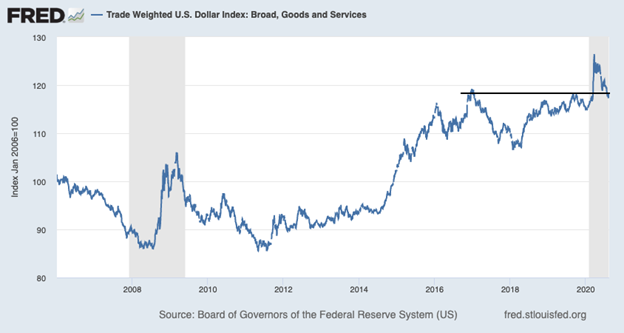

While I am convinced that the Fed wants the U.S. dollar to be weaker, and is actively trying to nudge it lower, I think we are headed for a rebound in the next month or two. One reason is that there is an election coming, which increases uncertainty in financial markets, making the dollar a safe-haven trade.

I do not believe that the dollar rally will be much more than a rebound in an ongoing weakening trend – as the Fed wants the dollar to go lower – but it can be a pretty big rebound.

Why would the Fed want the dollar to be weaker?

This coronavirus recession has caused a deflationary shock, so any factor that can help push the U.S. inflation rate higher, like a weaker dollar, is welcomed by the Fed. A weak dollar is positive for commodity prices and for emerging markets, which had been borrowing way too many dollars over the past 10 years. (A weak dollar helps emerging borrowers service those record-high U.S. dollar debts.)

A lot of emerging economies with record dollar borrowing – like those in Argentina and Turkey – already have rapidly depreciating currencies, which the Fed can do little to address, but the Fed can do a lot to weaken the dollar against currencies with sounder fundamentals.

However, if any currency’s fundamentals are weaker than the fundamentals of the U.S. dollar, the dollar will still appreciate relative to the currency with weaker fundamentals.

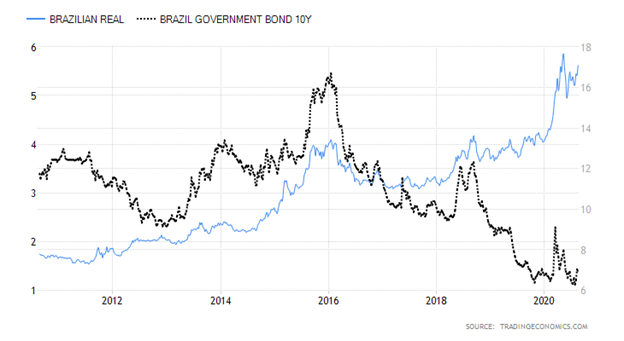

A case in point is the Brazilian real, which is again weakening. It fell from 4 to 6 (to the dollar) in the initial pandemic economic shock and it closed Friday at 5.63 against the dollar. If the real closes above 6 and stays there, it would be a sign that the Brazilian economy is not coping well with the pandemic-caused recession and it could spark a renewed outflow of capital that pressures the Brazilian real further.

Emerging economies do not have the ability to incur as much deficit spending as the U.S. or Europe and their healthcare systems are not as advanced, so one could say that the pandemic is doing more economic damage there. As a result, it won’t be as easy to rebound without a vaccine or a treatment. This calculus probably caused the Russians to jump the gun on a quick vaccine approval, as such a move is literally worth tens of billions of dollars to the Russian Treasury – if not more.

Whenever other vaccines become available, I suspect the Russians will price theirs very aggressively, the same way they undercut weapons sales of Western manufacturers. Where it is not politically necessary to buy from one’s allies, as with NATO members, Russians typically price comparable equipment 30-50% below most Western manufacturers so a vaccine is a potent weapon in a brave new world of viral warfare.

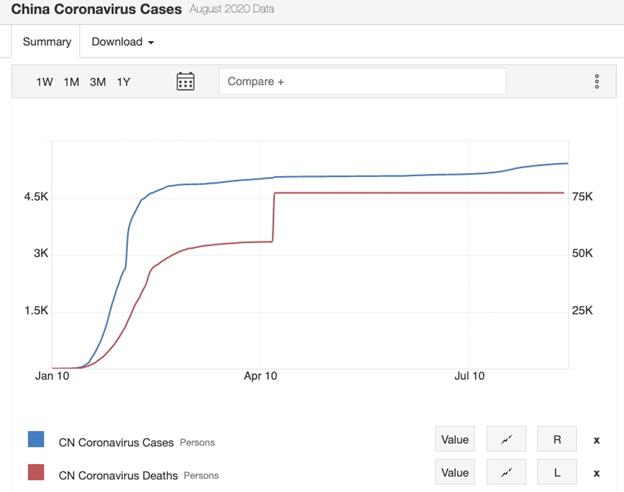

Do China’s Coronavirus Statistics Add Up?

There was infection emanating from Wuhan as early as November 2019 and there was no centralized response until January (other than silencing poor doctors that tried to speak out), so if the infection spread all the way to Europe and the U.S. because of the Chinese Lunar New Year and other holiday travel plans, somehow it did not spread inside China despite there being no centralized response until mid-January?

There are a lot of cooked up economic statistics in China, and coronavirus data is certainly one category.

Does anyone really believe these suddenly flat Chinese numbers?

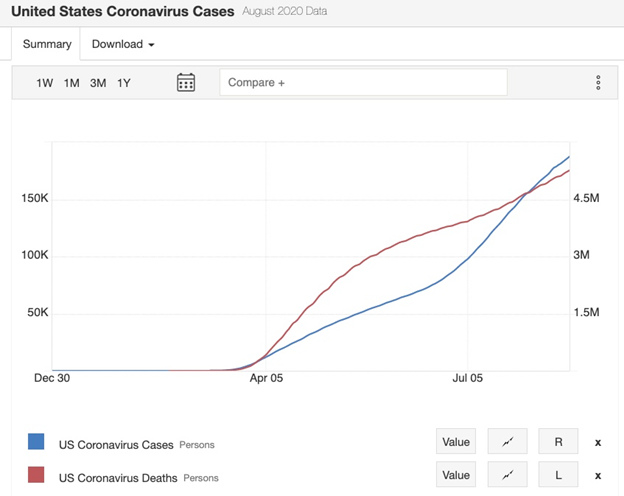

I believe that the U.S. response to the pandemic was mishandled, in the sense that if the response were more centralized, like in many European countries, infections and deaths would have been much lower.

The U.S. federal government would say that it does not have the authority to tell each of the 50 states exactly how to handle the pandemic. If that’s the case, they better get the authority pronto as Germany is also a federal republic, but it sure did a much better job of handling the pandemic. Even early disasters, like Italy and Spain, are doing much better than the U.S. now.

Related: =Fed’s Announcement Will Fuel Stocks, but There’s a Warning for Investors