Trending

Tail risk is the danger that asset prices move significantly more than what is considered normal. Given the lasting financial toll often caused by severe and unexpected adverse price movements, investors must appreciate potential causes of tail risk.

Today, the leading tail risk potential is increasing odds that high inflation remains stubborn, and the Fed continues to fight those odds aggressively. The Fed is trying to clarify that fighting inflation is job number one. They aggressively “whack” down dovish market narratives to get investors to believe them as part of their hawkish campaign.

Based on implied market expectations, investors are betting that inflation will quickly normalize and the Fed will promptly lower rates. The tail risk is that inflation proves sticky, and the Fed maintains a heavy foot on the financial brakes and continues to “whack” markets lower.

Volcker

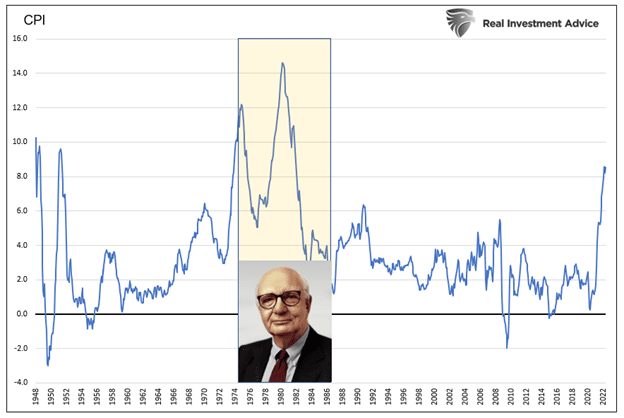

To better appreciate today’s tail risk, it’s worth reviewing the monumental burden put upon Fed Chair Paul Volcker to tackle inflation in the 1970s and early 80s.

Paul Volcker was not always a revered Fed Chair. During his watch, first as the President of the New York Fed and later as the Fed Chairman, he was tasked with crushing double-digit inflation, the likes of which hadn’t been seen in 25 years. Doing so required inflicting financial pain upon Americans. Not surprisingly, few appreciated his efforts at the time.

Everyone was really after him. There are famous stories of people even sending him their car keys because their car loans were so expensive – Volcker: The Triumph of Persistence- by William Silber

Based on comments from Volcker and others, it appears the Fed was able to limit inflation temporarily but struggled to put an end to persistent levels of high inflation. Success didn’t ultimately occur until they realized they had to change how people and companies thought about inflation.

The situation forty years ago and today are different. That said, we are growing increasingly concerned Jerome Powell and his colleagues are dealing with persistent inflation, not the brief bouts of transitory inflation seen over the last forty years.

This Time is Different

While inflation rates may be similar today to those of Volcker’s era, it is worth providing context for how today’s financial and economic environments are vastly different from Volcker’s experience and why it matters.

There is anxiety among Fed members that the low inflation era may be ending. If so, a new, high inflation regime and behaviors that accompany it will likely spell more restrictive Fed monetary policy.

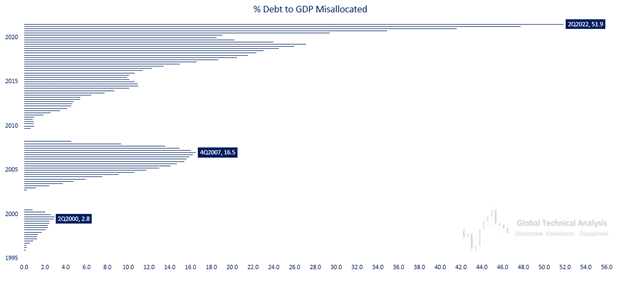

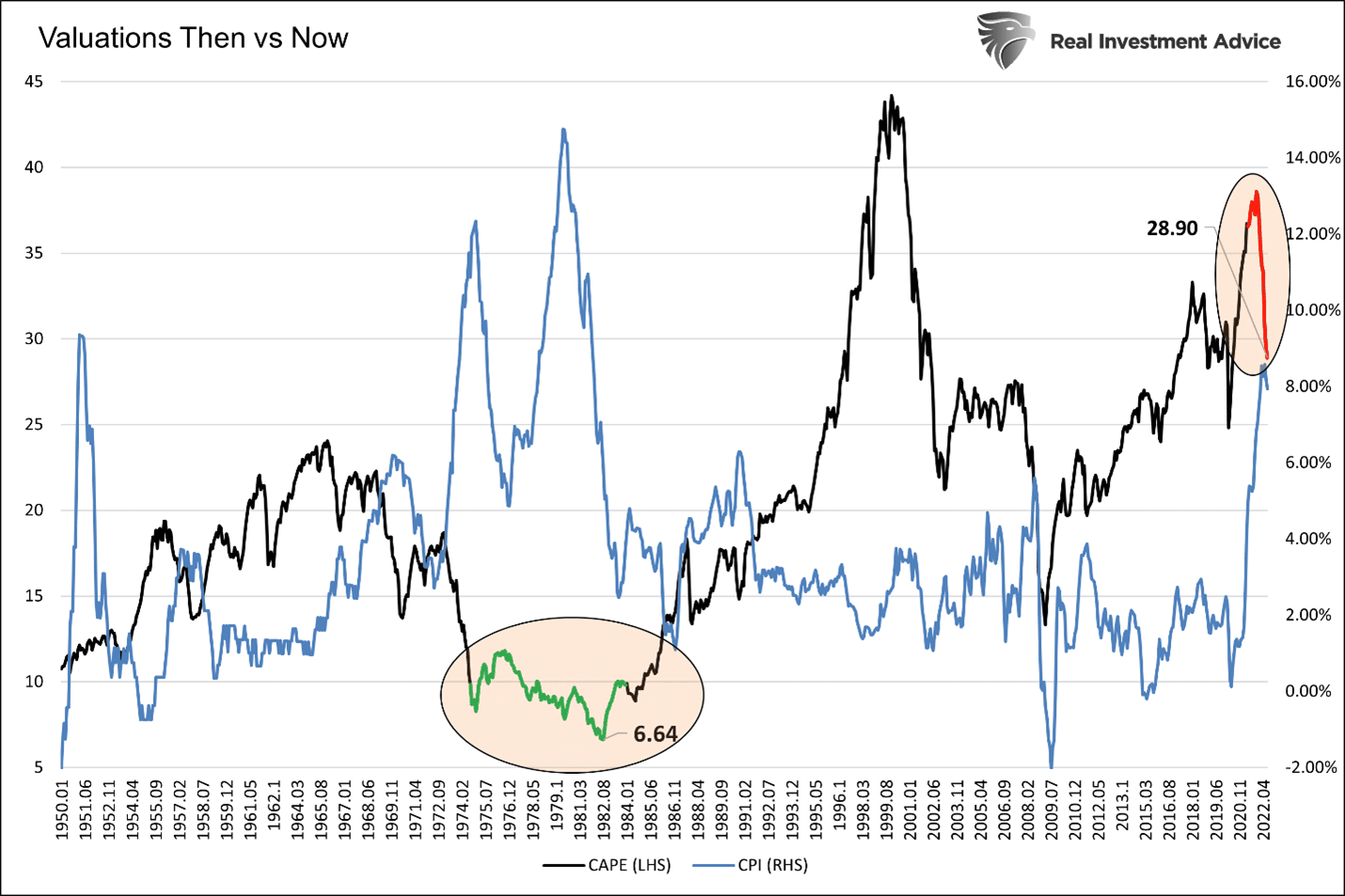

Restrictive policy, including double-digit interest rates, quelled Volcker’s high inflation regime. This time that anecdote is not feasible. Unlike the 70s and early 80s, when debt levels were low and equity valuations cheap, today’s economic and financial environments are the opposite.

Today’s economy relies heavily on debt for consumption and to roll over maturing debt and avoid bankruptcy. High-interest rates will be exponentially more damaging than they were forty years ago.

As the graph below from Brett Freeze shows, an increasing amount of debt has been misallocated. The only way to pay interest and principal on such unproductive debt is to issue new debt to replace it.

The following graph shows the CAPE valuation hit a ‘dirt cheap’ level of 6.64 in the early 80s. Today, CAPE stands at 28.90, about 50% above the historical average. The risk to investors of just a normalization of valuations is palpable.

As we share, there is significantly more financial market and economic risk today than in the 70s and early 80s if high inflation becomes entrenched.

Crushing high inflation immediately before it becomes persistent will take harsh measures, but it may be the best action given the nation’s financial vulnerability. If they fail at the task and let high inflation persist, there will be much bigger problems.

Persistent Inflation- The Fed’s Nightmare Scenario

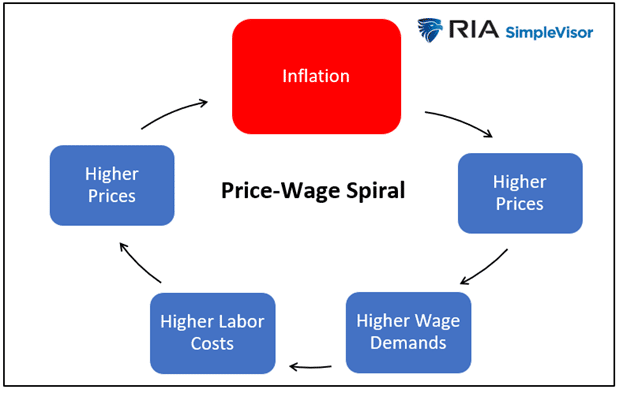

In Persistent Inflation Scares the Fed, we discussed one of the Fed’s greatest fears, a price-wage spiral. To wit:

The BIS argues that inflation drives consumer and corporate spending decisions in a high inflation regime. This results in behavioral changes, which cause individual prices of goods and services to become more correlated. Inflation begets inflation and therefore becomes persistent.

Further: Once the general price level becomes a focus of attention, workers and firms will initially try to make up for the erosion of purchasing power or profit margins they have already incurred.

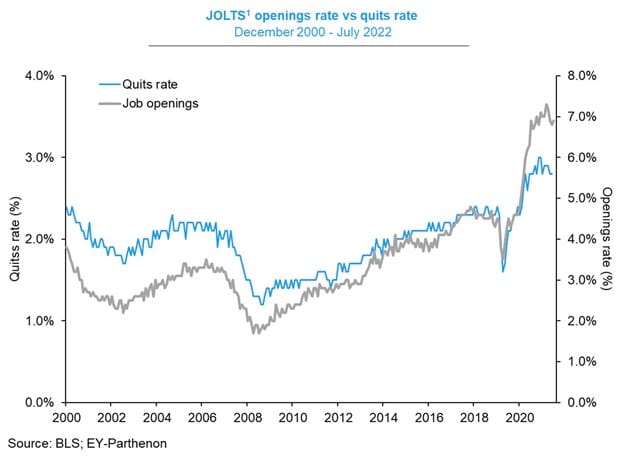

Essentially once people think that high inflation is permanent, their behaviors change. As prices rise, workers demand higher wages, companies raise prices to compensate, and on and on in a circular motion. Wages are already rising as employees and unions have new-found leverage. Thus far, companies are raising prices to offset higher wages.

The graphs below point to a very tight labor market. Based on corporate margin data, companies are thus far able to raise prices to help offset higher wages. The first revolution of a potential price-wage spiral has already begun.

The Fed must be forceful in changing the inflation expectations of employees and employers. They must be willing to take action to increase the unemployment rate, thereby reducing employees’ leverage over employers. Doing so involves weakening the economy and punishing asset prices. Their ability to eliminate the odds of a new inflation regime rests on their ability to convince employees, corporations, and the markets that high inflation will not be lasting.

Unlike prior monetary policy, the goal is not just about changing our consumption habits but, more importantly, changing our inflation outlook.

Is The Fed Up For The Task?

In his unexpectedly hawkish Jackson Hole speech, Jerome Powell made it clear that fighting inflation is vital to longer-term economic health. He also seems very aware of the dangers of changing attitudes about high inflation. To wit:

If the public expects that inflation will remain low and stable over time, then absent major shocks, it likely will. Unfortunately, the same is true of expectations of high and volatile inflation. During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decision-making of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions. As former Chairman Paul Volcker put it at the height of the Great Inflation in 1979, “Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations.”

On the heels of Powell’s speech Neel Kashkari, President of the Minneapolis Fed, stated, “I was actually happy to see how Chair Powell’s Jackson hole speech was received. People now understand the seriousness of our commitment to getting inflation back down to 2%.” The market’s reception of the Chairman’s speech was a 3%+ decline in the S&P 500.

Yes, the Fed seems to get it. But will the Fed have the nerve to do whatever it takes to crush inflation?

Will Investors Get Caught Offsides?

Even after Powell’s speech, investors continued to underestimate what the Fed may have to do. If inflation drops quickly back to 2% and a price-wage spiral fails to materialize, investors will be correct.

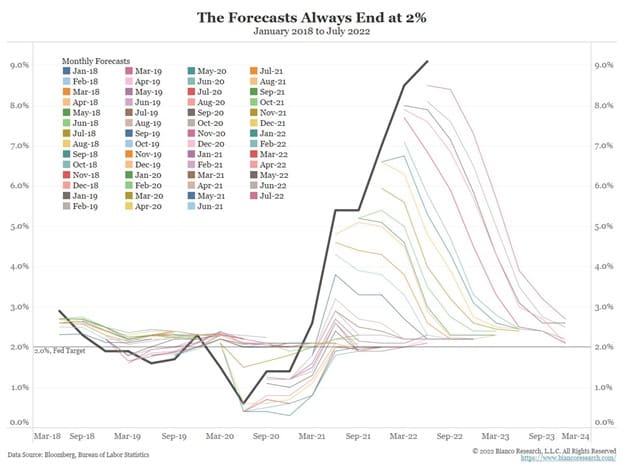

Might they be wrong? The graph below shows economists have grossly underestimated the persistence and amount of inflation for almost two years.

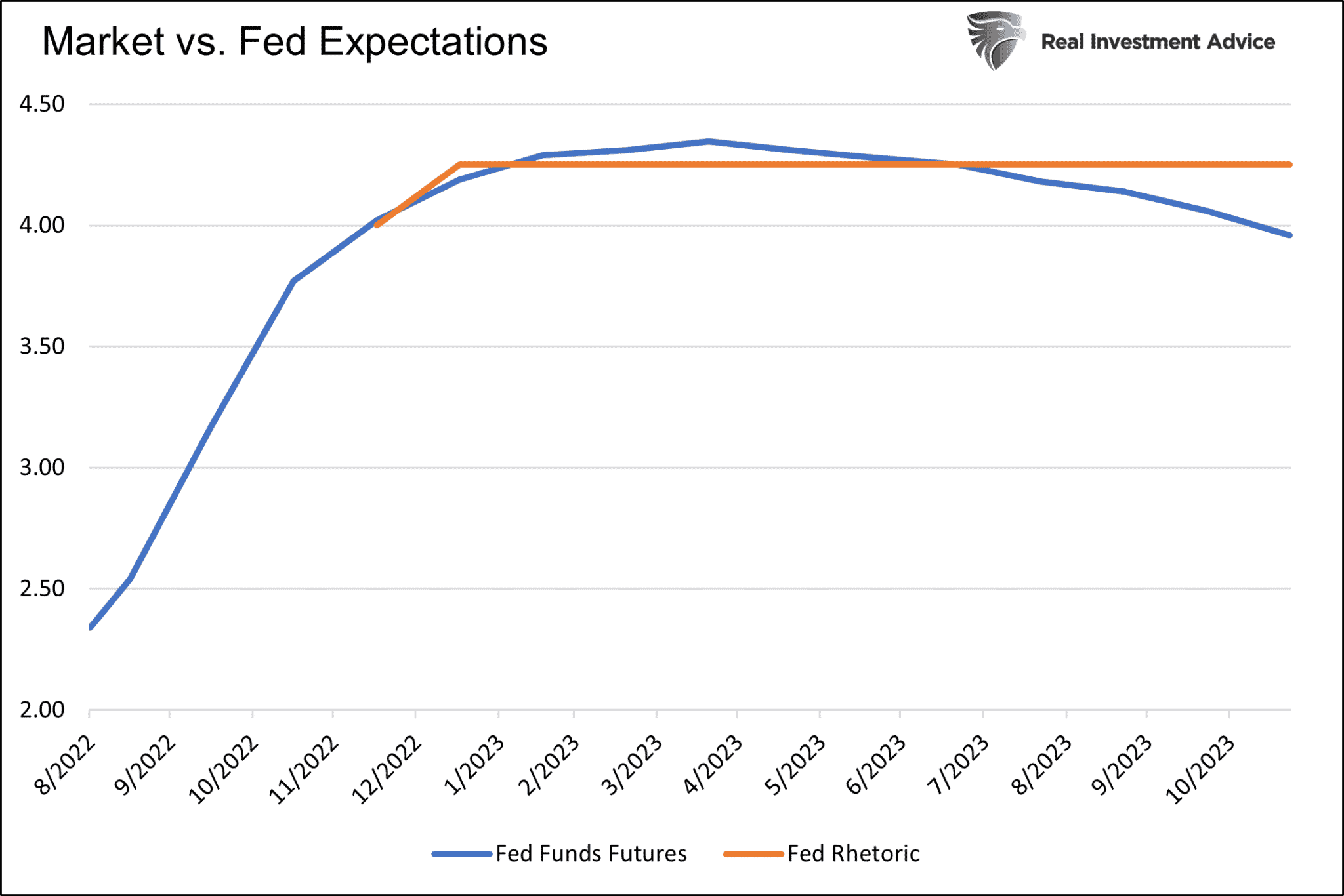

The market is now aligned with recent Fed speak of a 4.00-4.50% Fed Funds rate. However, as shown below, it starts leaning toward a Fed easing by the spring of 2023. Most recent Fed members have been clear that Fed Funds will likely stay above 4.00% for 2023. To wit:

We’re going to have to get interest rates up probably a little above 4% by sometime early next year, and hold them there. – Cleveland Fed President Mester

We’re going to stick at this until the job is done, until the job is done. I don’t think markets are pricing in the fact that not only could rates get up to 4-4.5%, they could stay there for all of 2023. -Jerome Powell

Summary

Persistently high inflation is the tail risk that few investors seem to appreciate.

Dovish market narratives and investors betting on them are like the moles in the arcade classic Whac-A-Mole. Any bit of dovish inflation news and the market narrative shifts to a less aggressive Fed and soon-to-be lower interest rates. Once such sentiment gains momentum, Fed members pull out the mallet and whack the dovish narrative down.

If inflation remains persistent, even in the 4-6% range, investors will appreciate that the Fed’s job is not easy. In this case, the tail risk is the market’s realization that the Fed needs to take a page from Volcker’s book and raise rates beyond 4.50% and possibly keep them there well beyond 2023.

Related: Yields are Defying Yesterday’s Logic