Trending

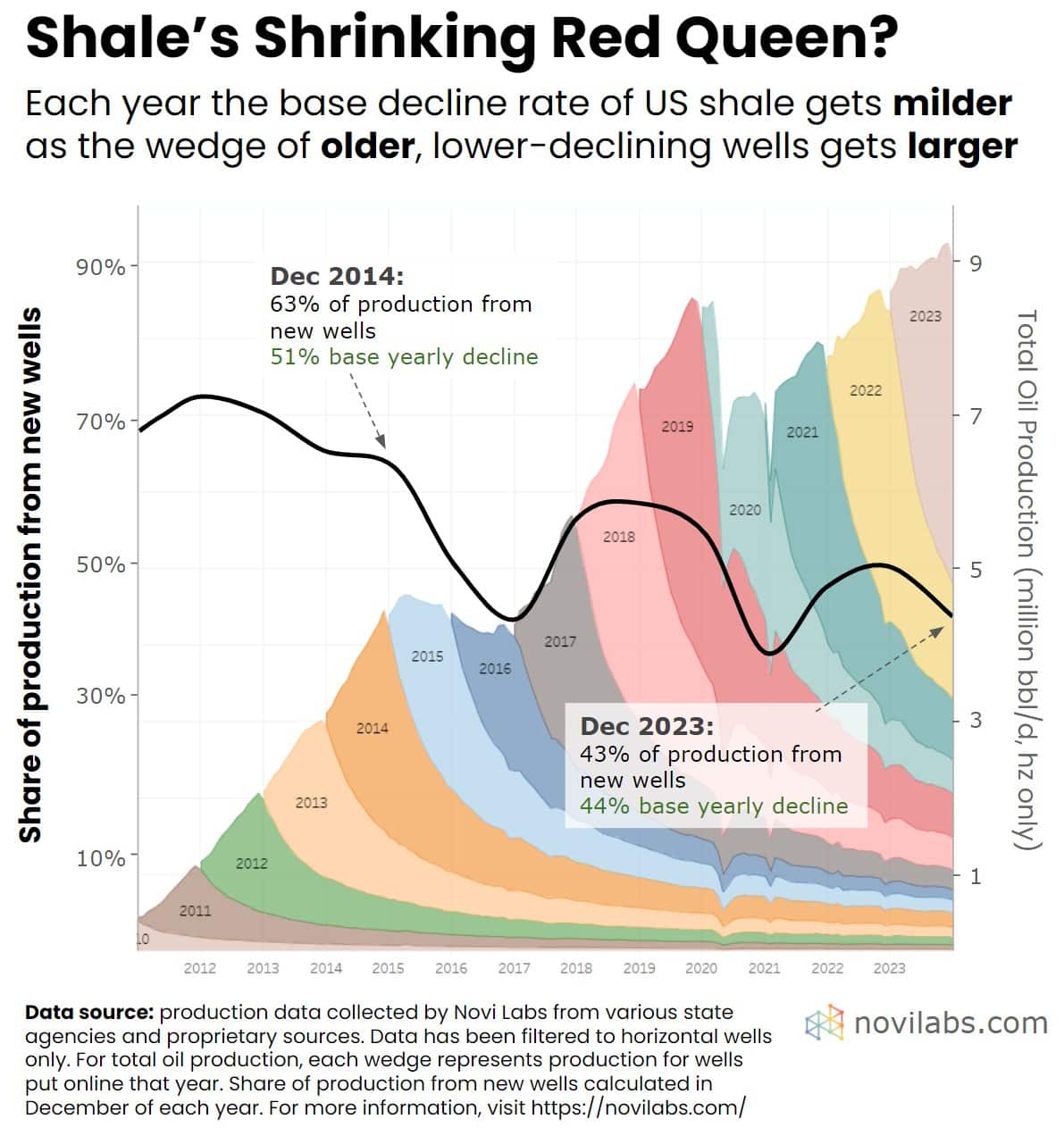

In a recent article, geologist Ted Cross of Novilabs eases investor concerns about the rapid depletion rate of shale oil wells. He claims investor fears are comparable to The “Red Queen Effect,” a concept from Alice in Wonderland: “It takes all the running you can do to keep in the same place.” Investors worry that new shale oil production will decline so quickly that new wells can’t offset the declining production of existing wells. Therefore, total production increases are evermore challenging to achieve. Ted acknowledges the sharp decline in new shale oil wells but notes:

“Yes, shale wells decline rapidly early in life, but those declines moderate as they age, settling in somewhere between 5% and 10% per year. As the collective population of shale wells gets older and older, the “base decline” gets lower and lower.“

The graph below shows total oil production keeps rising with less production, as a percentage, attributed to new shale oil wells. In 2014, shale oil production hit about four million barrels per day, with almost two-thirds coming from new wells. Ten years later, total production is more than double that rate. However, only 43% is from the output of new wells. He also adds that the rate of decline of older shale oil wells moderates even further. To wit: “The Bakken was able to post impressive growth in 2023 in part because wells in the play from 2022 and prior only declined 33% in aggregate.” The bottom line is that shale oil production declines much quicker than traditional wells, but the rate of decline is less than investors fear.

What To Watch

Earnings

Economy

Market Trading Update

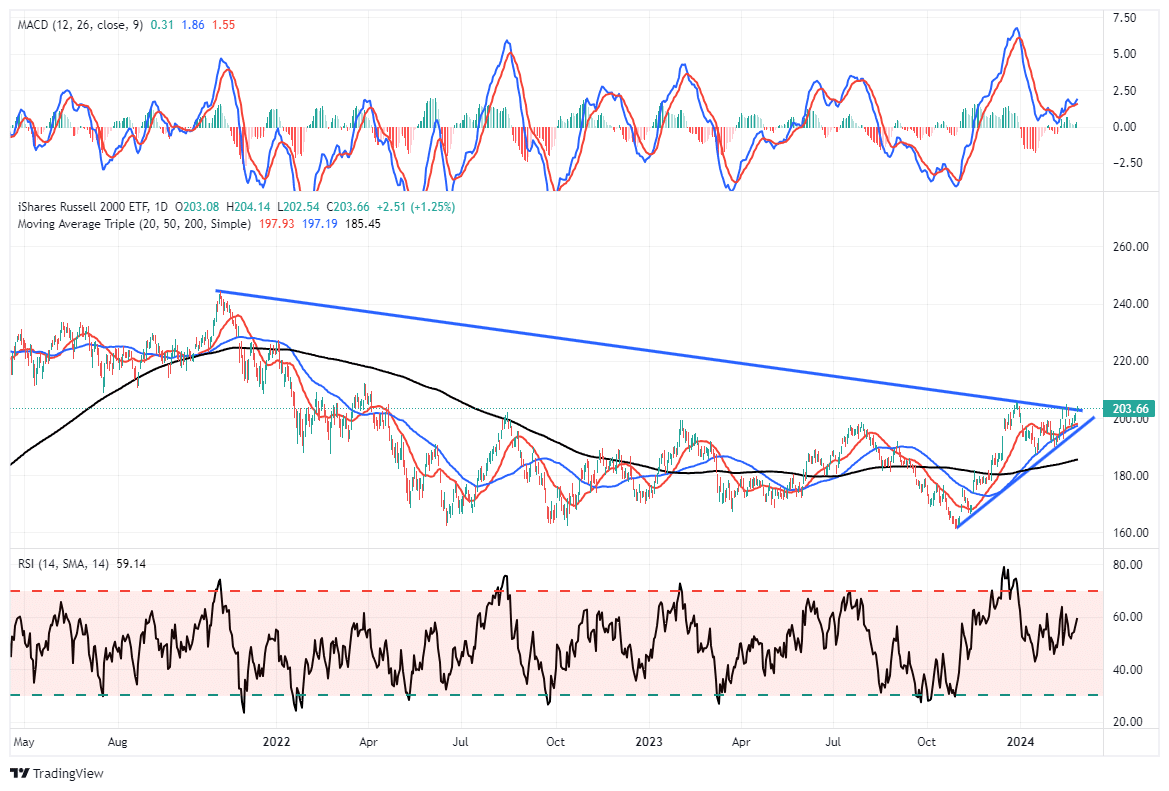

The Russell 2000 jumped in yesterday’s trading again, revving up the speculative crowd. As noted on Tuesday, retail investors have been chasing small-cap stocks for a potential “catch-up” trade with the rest of the market. As shown below, the Russell 2000 still trades well below its all-time highs and is lagging the performance of the large-cap index by a significant margin. As shown, the Russell 2000 is now at a critical juncture, a break out of the downtrend could set the index up for a push higher. However, this has also been the point of previous failures over the last year.

In yesterday’s commentary, we suggested remaining a bit more cautious as the current speculative push is getting rather long in terms of duration. The S&P 500 index has been positive in 13 of the last 15 weeks, the longest stretch of gains since 1989. While retail investors are turning their attention to the more speculative names in the market, it is worth noting that hedge funds and institutions have started selling positions. As we will discuss on Friday, it is worth noting that “dumb money” is currently very allocated to risk assets. Such is usually a point where forward returns weaken significantly.

Personal Interest Rates Are Rising Rapidly

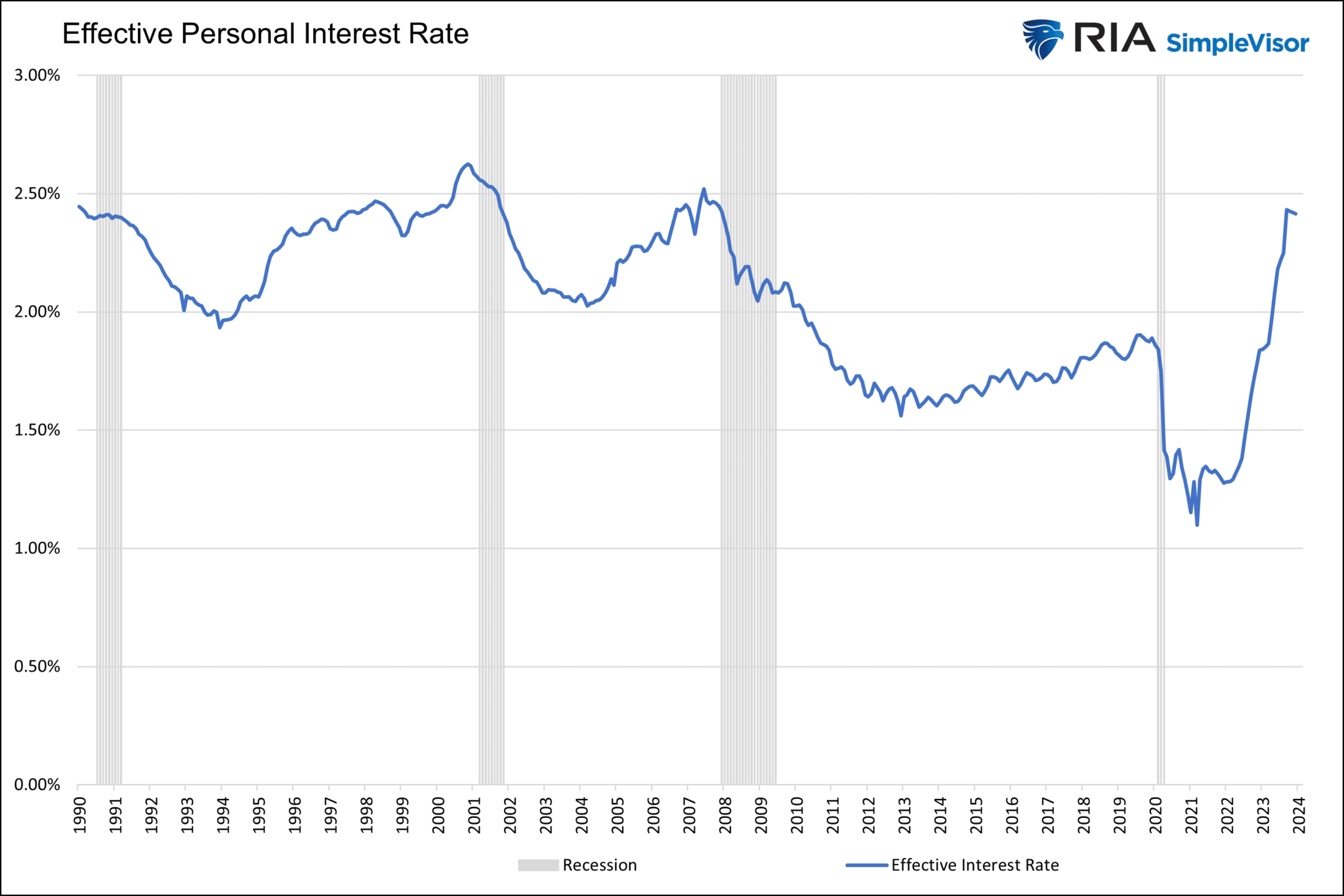

The graph below shows total personal interest payments as a percentage of total income. In the post-financial crisis era, the effective personal interest rate ranged between 1.50% and 2.00%. It is now following bond yields higher and approaching 2.50%. The rate itself is now higher than most consumers are accustomed to. However, more importantly, note that prior peaks preceded recessions. Given that personal consumption accounts for about two-thirds of GDP, the ability to borrow and borrowing terms are essential to the economy. The graph also explains the lag effect. It has taken two years since the Fed started raising rates for the effective personal rates to near prior peaks.

More On Buffett And Market Excuberrance

Lance Roberts’s latest article, This Is Nuts- An Entire Market Chasing One Stock, discusses the poor breadth of the market and the leadership role that Nvidia plays. Per the article:

In momentum-driven markets, exuberance and greed can take speculative actions to increasingly further extremes. As markets continue to ratchet new all-time highs, the media drives additional hype by producing commentary like the following.

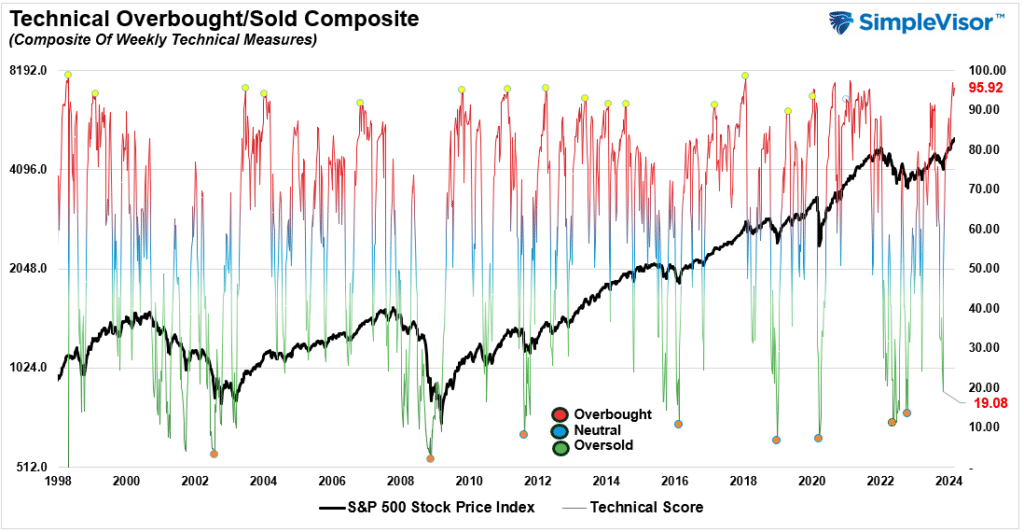

He supports his statement with the following graph. It shows that markets are “exceedingly overbought.” He continues:

The composite index below comprises nine indicators measured using weekly data. That index is now at levels that have denoted short-term market peaks.

Along the same lines, yesterday’s Commentary informed us that Warren Buffett’s Berkshire Hathaway portfolio is sitting on record amounts of cash. He does not see value and is not willing to chase the market. Today, we share another bit of advice from his speech last weekend.

“One fact of financial life should never be forgotten. Wall Street – to use the term in its figurative sense – would like its customers to make money, but what truly causes its denizens’ juices to flow is feverish activity. At such times, whatever foolishness can be marketed will be vigorously marketed – not by everyone but always by someone.”

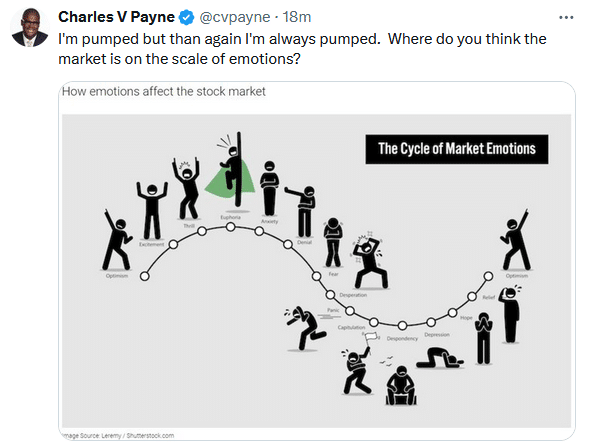

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”