Trending

Economic “reflation” is becoming the next bullish narrative as equity valuation increases continue to outpace earnings gains, at least according to Gold Sachs and Tony Pasquariello.

“If GS is correct on the big calls, the macro backdrop is set to remain friendly: the US economy should continue to grow nicely above trend — picking up speed as the year moves along — with three adjustment rates cuts along the way. to not obscure the moral of that story: the Fed is set to ease policy … into an upswing. while Fedspeak this week had a somewhat hawkish bent, the house view for 2024 remains intact.”

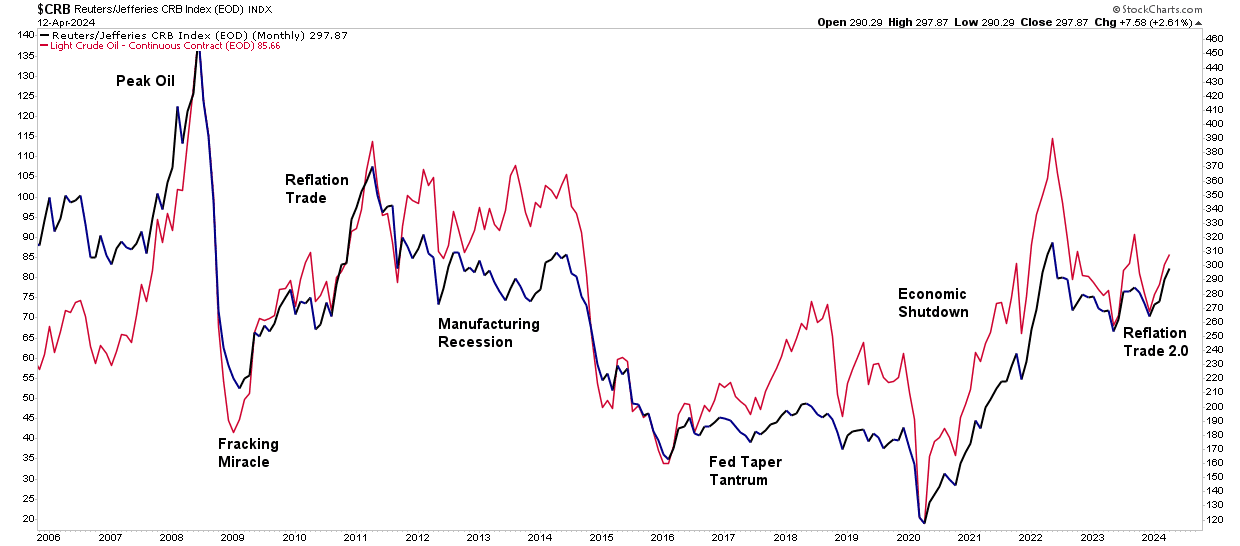

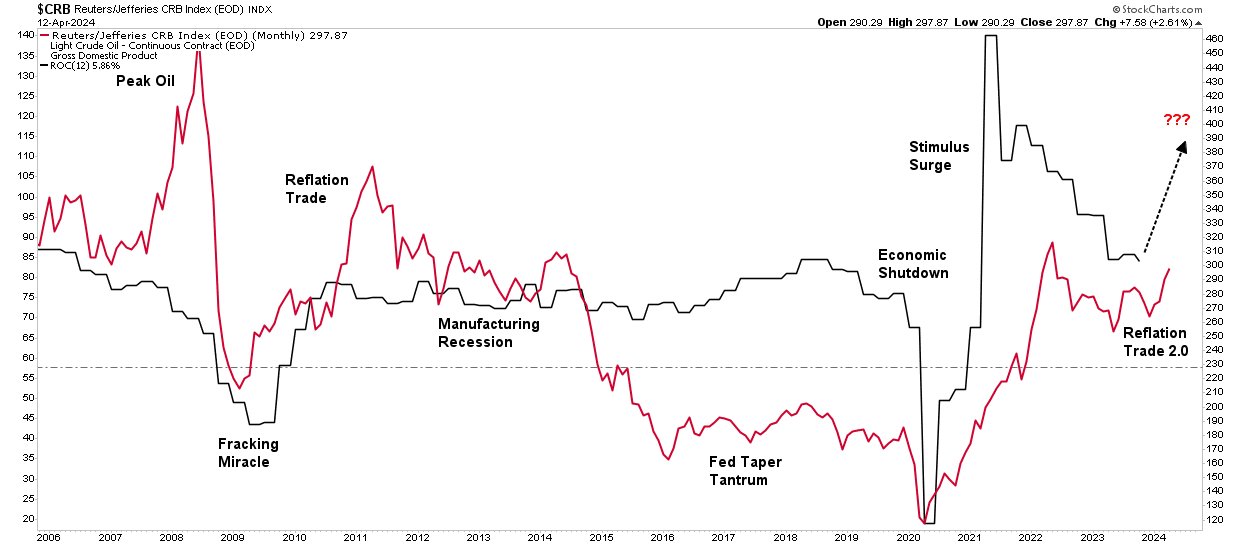

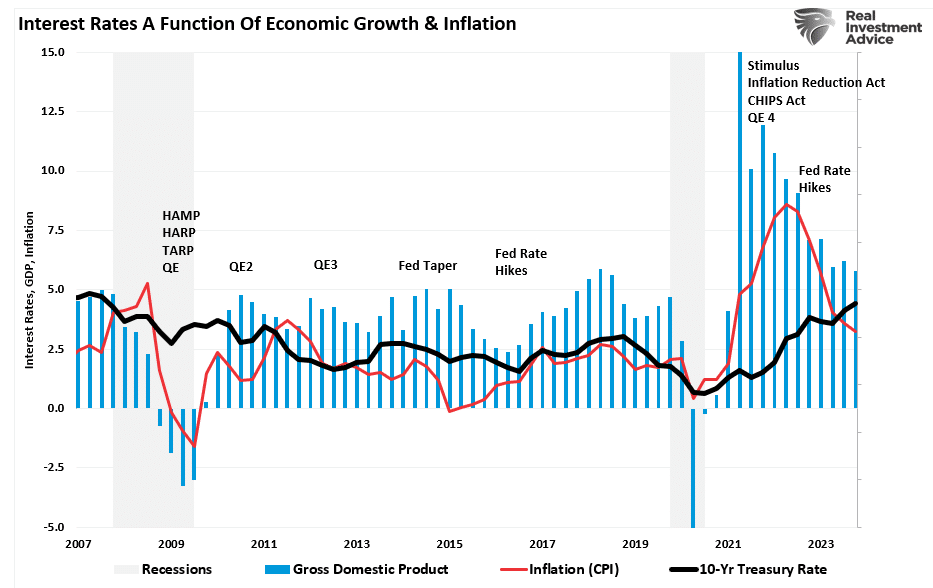

Interest rates, gold, and commodity prices have increased in the past few months. Unsurprisingly, the bullish narrative to support that rise has gained traction. Interestingly, this “reflation” narrative tends to resurface by Wall Street whenever there is a need to explain the surge in commodity prices. Notably, the last time Wall Street focused on the reflation trade was in 2009, as noted by the WSJ:

“The most talked-about investing strategy these days isn’t stuffing money in a mattress, it’s the reflation trade — the bet that the world economy will rebound, driving up interest rates and commodities prices.”

While that “reflation trade” lasted for about two years, it quickly failed as economic growth returned to 2%-ish growth along with inflation and interest rates. As shown, oil and commodity prices have a very high correlation. The critical reason is that higher oil prices reduce economic demand. As consumption falls, so does the demand for commodities in general. Therefore, if commodity prices are to “reflate,” as shown, such will depend on more robust economic activity.

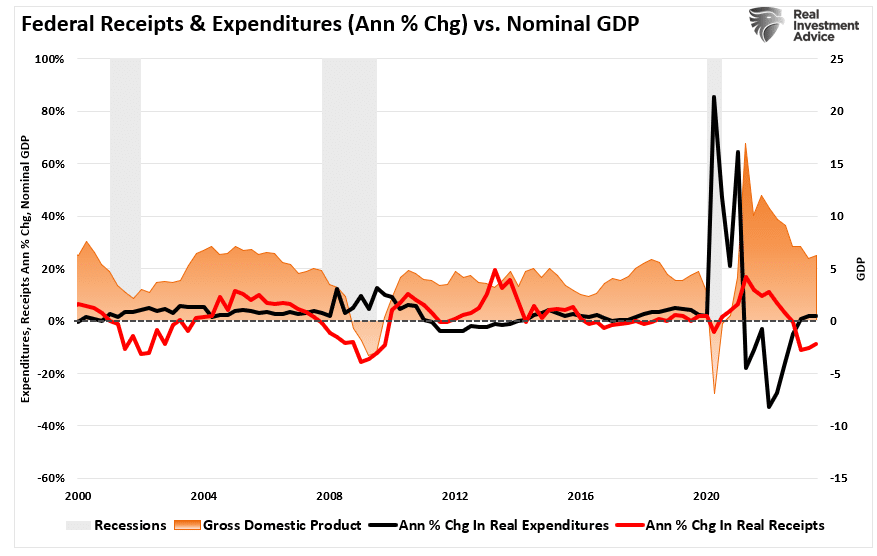

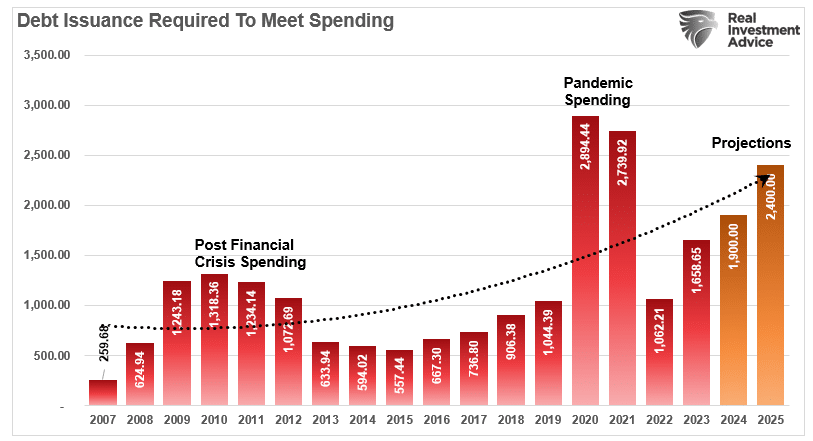

As such. The reflation trade hinges on a global resurgence of economic activity, usually associated with economies recovering from a recessionary period. However, the U.S. never experienced a recession. As discussed in “Deficit Spending,” despite numerous recessionary signals, like the inverted yield curve, manufacturing data, and leading economic indicators, the economy avoided recession due to massive governmental spending. To wit:

“One explanation for this has been the surge in Federal expenditures since the end of 2022 stemming from the Inflation Reduction and CHIPs Acts. The second reason is that GDP was so grossly elevated from the $5 Trillion in previous fiscal policies that the lag effect is taking longer than historical norms to resolve.”

While economists focus on the “reflation trade,” we must answer whether the support for more substantial economic growth exists. This is the sole determining factor in whether the “reflation trade” can continue.

Is Reflation Already Behind Us?

Interest rates and inflation have ticked up recently, driving investors into gold and commodities. However, the surge in precious metals and commodities is more of a function of speculative exuberance rather than an economic resurgence. As discussed in “Speculative Warnings,”

“In other words, the stock market frenzy to “buy anything that is going up” has spread from just a handful of stocks related to artificial intelligence to gold and digital currencies.“

Notably, the gold, commodities, and interest rate surge corresponded with more robust economic growth beginning in the third quarter of last year. That uptick in economic growth defied economists’ expectations of a recession. Such was because of the massive flood of monetary support from Government spending programs. However, that monetary impulse is now reversing.

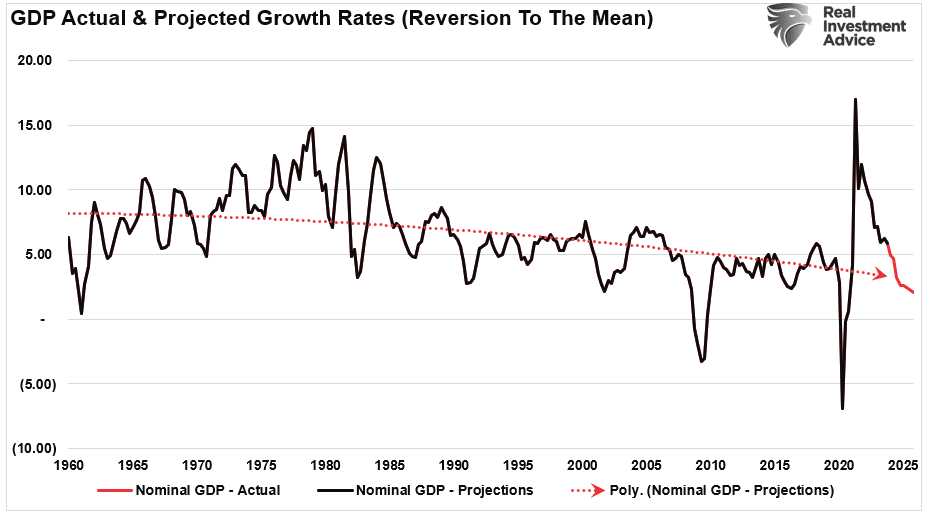

As far as the “reflation trade” is concerned, as that monetary impulse recedes, so will economic growth, as shown. Even if the economy continues to grow at 2-2.5% annualized each quarter, the annual rate of change in growth will continue to slow.

Importantly, this assumes that the Government will keep “spending like drunken sailors” over that same period. However, if they don’t, the economic growth rate will slow even more quickly without increasing monetary spending.

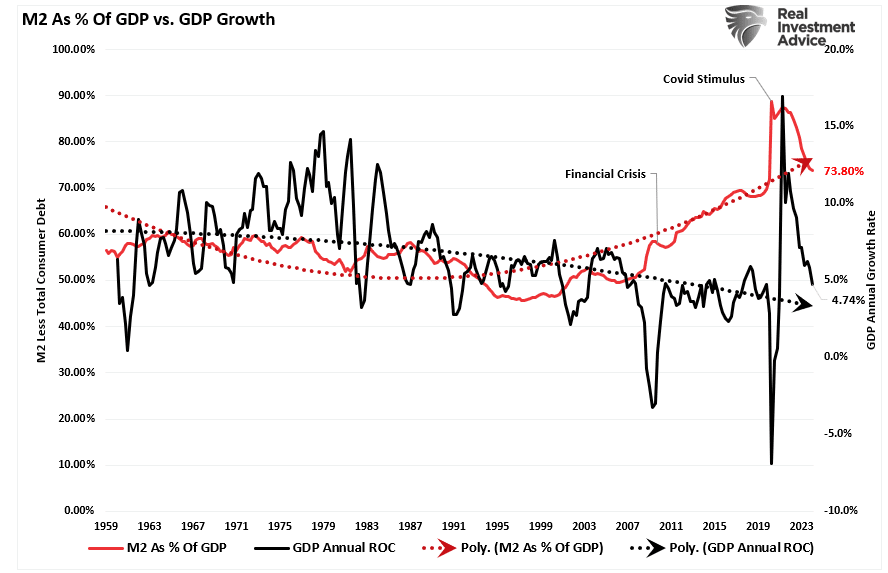

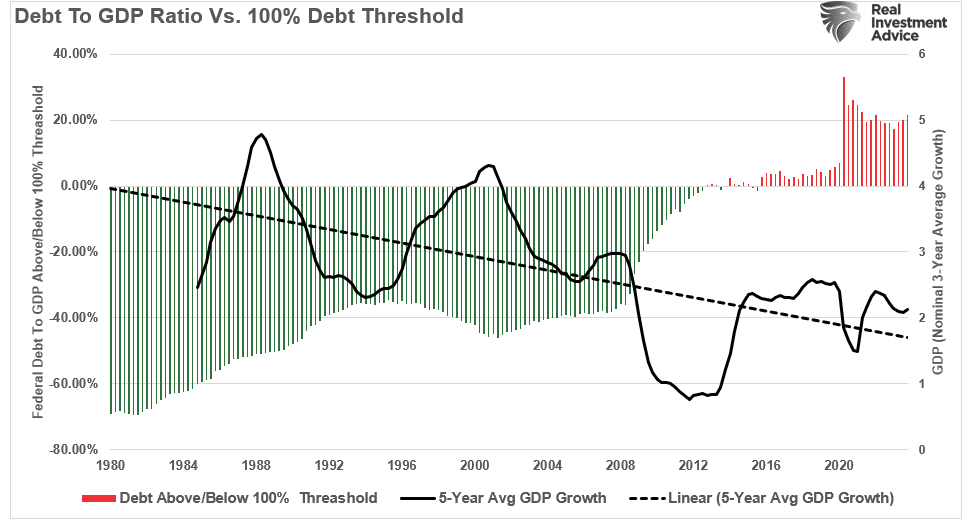

It is important to remember that increasing debts and deficits do not elicit stronger long-term economic growth. As debt levels rise, economic growth rates will slow as money diverts from productive investment into debt service.

That reality should be unsurprising, as this is not the first time the Government has gone “all in” on a reflation trade. As noted above, following the Financial Crisis, the Government intervened with HAMP, HARP, TARP, and a host of other spending programs to “reflate” the economy.

Let’s review what happened with interest rates, inflation, and gold and commodity trade.

Past May Be Prologue

As noted in 2009, following the “Financial Crisis” and recession, the Government and the Federal Reserve engaged in various monetary and fiscal supports to repair the economy. While the economy initially recovered from the recessionary lows, inflation, economic growth, and interest rates remained subdued despite ongoing interventions.

That is because debt and artificially low interest rates lead to malinvestment, which acts as a wealth transfer mechanism from the middle class to the wealthy. However, that activity erodes economic activity, leading to suppressed inflation and a surging wealth gap.

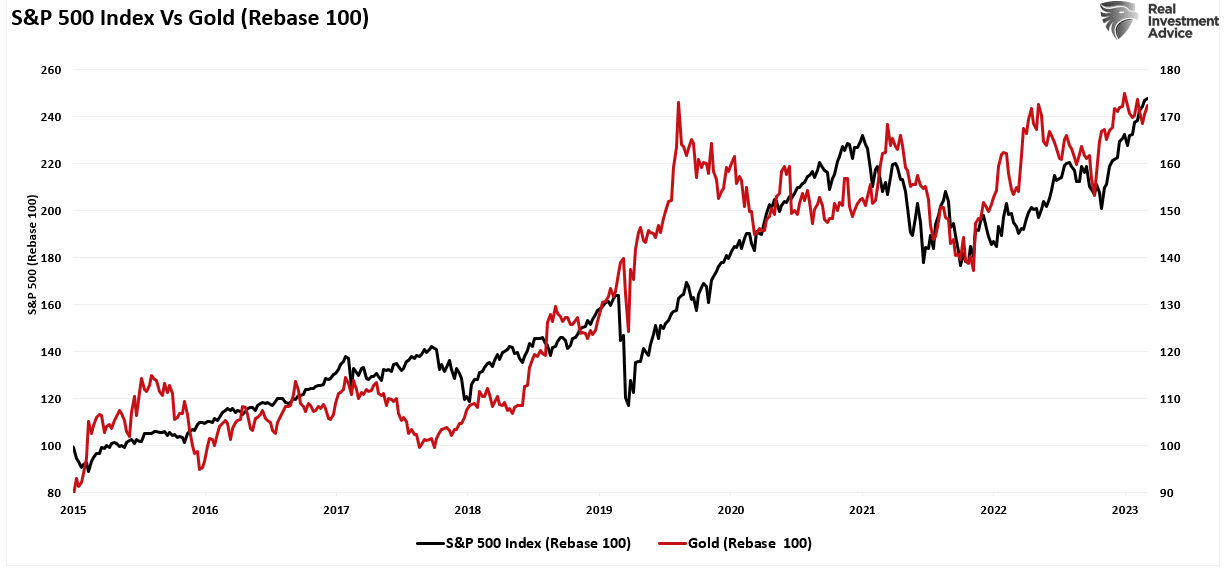

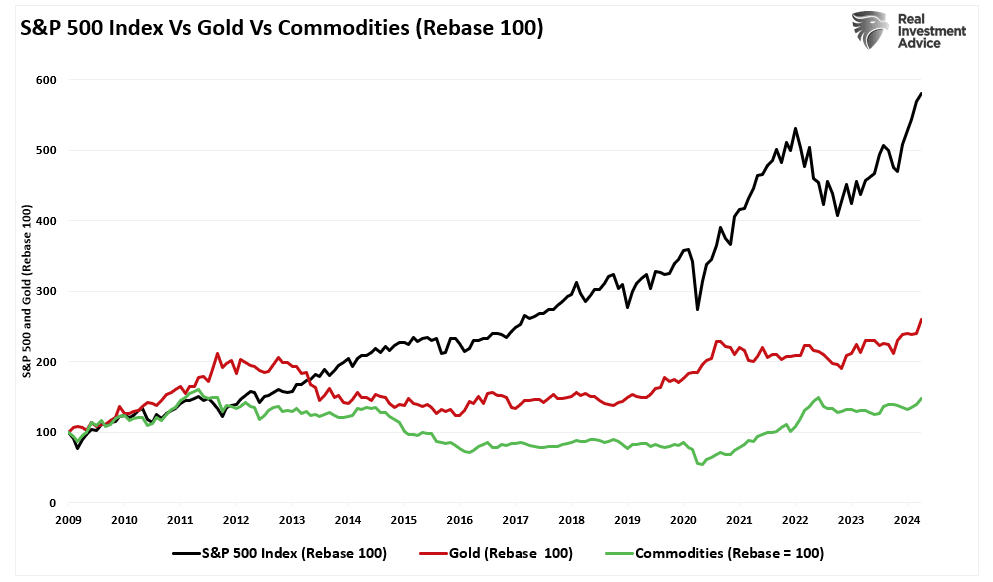

During that same period, commodities and precious metals rose initially as the “reflation expectation” was widespread. However, debt-driven realities quickly undermined that assessment and those investments languished relative to equities, as the flood of liquidity and low rates made equities far more attractive to investment.

While the relative performance of precious metals and commodities has picked up in recent months, this is more likely a function of “irrational exuberance” in the financial markets. As discussed previously, the surge in speculative investment activity is not uncommon to markets, and currently, many asset classes are becoming highly correlated.

However, while there is a compelling narrative around gold and precious metals from an investment perspective, those chasing that trade have had many years of terrible underperformance. While this time could be different, the “reflation narrative” will most likely fall prey to the realities of excessive debt, which will pressure Governments to cut rates once again.

If the past is potentially prologue, likely, the bullish narrative of “reflation” may once again find future disappointment. Such is particularly the case as the economics of debt and poor policy choices continue to erode the middle class further.