Given the “full steam ahead” on tariffs signaling from the White House markets surprisingly ended yesterday higher. Pre-market futures pointed to a rough open but aside from Small Caps falling 0.56% and some mild Mag 7 weakness which helped the Nasdaq Composite shed a mere 0.14%, the S&P 500 gained 0.55% and the Dow closed 1.00% higher. Sectors were up across the board, led by Consumer Staples (1.57%) and Financials (1.22%). We saw relative weakness in Technology (0.05%) which was held back by continued reduced sentiment in the AI and data center trade as evidenced by a down day from Microsoft (MSFT), Nvidia (NVDA), Palantir Technologies (PLTR), and Broadcom (AVGO), to name a few.

Also surprising, given yesterday’s equity price action was the Cboe Market Volatility (VIX) index edging higher to close at 22.28 and gold picking up almost $30 to hit $3.123.20/oz. Similarly, despite a recent rating agency warning on U.S. credit quality from Moody’s, the 10-year treasury index saw slightly stronger bids, pushing the yield lower to 4.21%.

Oil price action has been interesting lately, which yesterday included a report showing that US crude oil production hit a 15-month low in January. This, coupled with expectations of Trump's controls on Russian Oil and his recent threats against Iran saw West Texas Crude (WTI) rise 3.00% and Brent Light Sweet (BRENT) gain 1.51%.

The Tematica Select Model Suite saw leadership from Cash Strapped Consumer, Guilty Pleasure, and Core Holdings strategies. While not falling out of bed per se, Nuclear Energy & Uranium, and Space Economy lagged to close out the quarter.

Tariff Clarity? More Earnings Pre-Announcements? Powell?

With one day to go before President Trump unveils his reciprocal tariffs, futures point to a mixed start for Q2 2025. While Trump claims to have settled on his tariff plan, reports as to what the president could announce, reportedly at 3 PM ET in the White House Rose Garden continue to vacillate between 20% global tariffs on virtually all imports to more targeted tariffs.

Our take is the situation is fluid, and the outcome will likely hinge on last-minute deal-making attempts that would allow Trump to claim some victory on the trade front. How all of this comes together and what it means for the market is very much TBD, but in our mind, what is just as important will be the response from those getting slapped with these tariffs. Then it becomes a question of whether Trump opts to escalate tariffs further. If you’re a public company that has just closed its books and is getting ready to issue June quarter guidance and possibly update your outlook for 2025, what’s to come has the potential to determine if your guidance meets, beats, or falls short of market expectations.

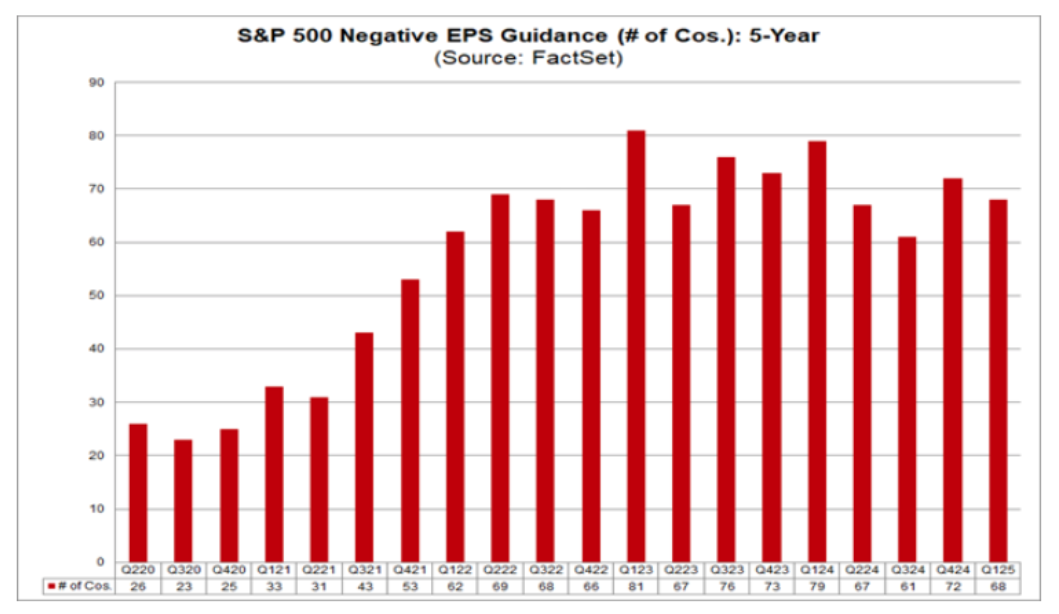

Data from FactSet shows that overall, 107 S&P 500 companies have issued quarterly EPS guidance for the first quarter. Of those companies, 68 have issued negative EPS guidance and 39 have issued positive EPS guidance. While a tad higher compared to the 5-year average, what is announced in the next few days could lead to even more negative earnings pre-announcements and fuel more questions about S&P 500 EPS growth prospects. Typically, when that happens, folks also question the market multiple, and for reference, the S&P 500 closed last night at 20.8x expected 2025 EPS of $269.92. For inquiring minds, that’s a 7% premium to the average peak P/E multiple for the S&P 500 over the 2000-2024 period sans the pandemic and matches the average peak P/E multiple for the 2015-2024 period also sans 2020.

Because we are in the often cited “quiet period” ahead of the March quarter earnings deluge and only one Fed official poised to speak today, it’s a good bet all eyes will be on the day’s economic releases. Those include S&P Global’s (SPGI) Final US March Manufacturing PMI, the more closely followed ISM March Manufacturing PMI, and the February JOLTs and Construction Spending Reports.

For our money, the focus will be on the March Manufacturing PMI reports and how they compare to the data found in the February reports. When reviewing the February data, the concern was a pull forward in demand given the expected Trump tariffs at the time on Canada, Mexico, and China. With Trump touting April 2 as “Liberation Day” during March, it’s quite possible the March data doesn’t fall as much as some might expect and it could surprise to the upside, likely due to more sales pulling forward ahead of unknown tariffs.

The big reveal to us will be in the new order dynamics as well as those for employment and inflation. On the one hand, because the US manufacturing economy is responsible for ~15% of GDP, what we see in the March Services PMI reports for those figures will be even more revealing. However, what we see in the data will influence GDP expectations for the March quarter. Given the Atlanta Fed’s GDPNow model at -2.8% for Q1 2025 and the New York Fed’s Nowcast model at 2.86%, it’s safe to say expectations are currently all over the map. It will start the process of refining expectations for what we could see in ADP’s March Employment Report tomorrow, Friday’s March Employment Report, and what Fed Chair Powell could say late Friday morning.

We’ll have more to share on Thursday as some of these puzzle pieces start to come together.

Related: Trump's 'Liberation Day': Markets Brace for Economic Chaos on April 2nd"